Contents

- 1 How Education Loans Work in India — The Basics

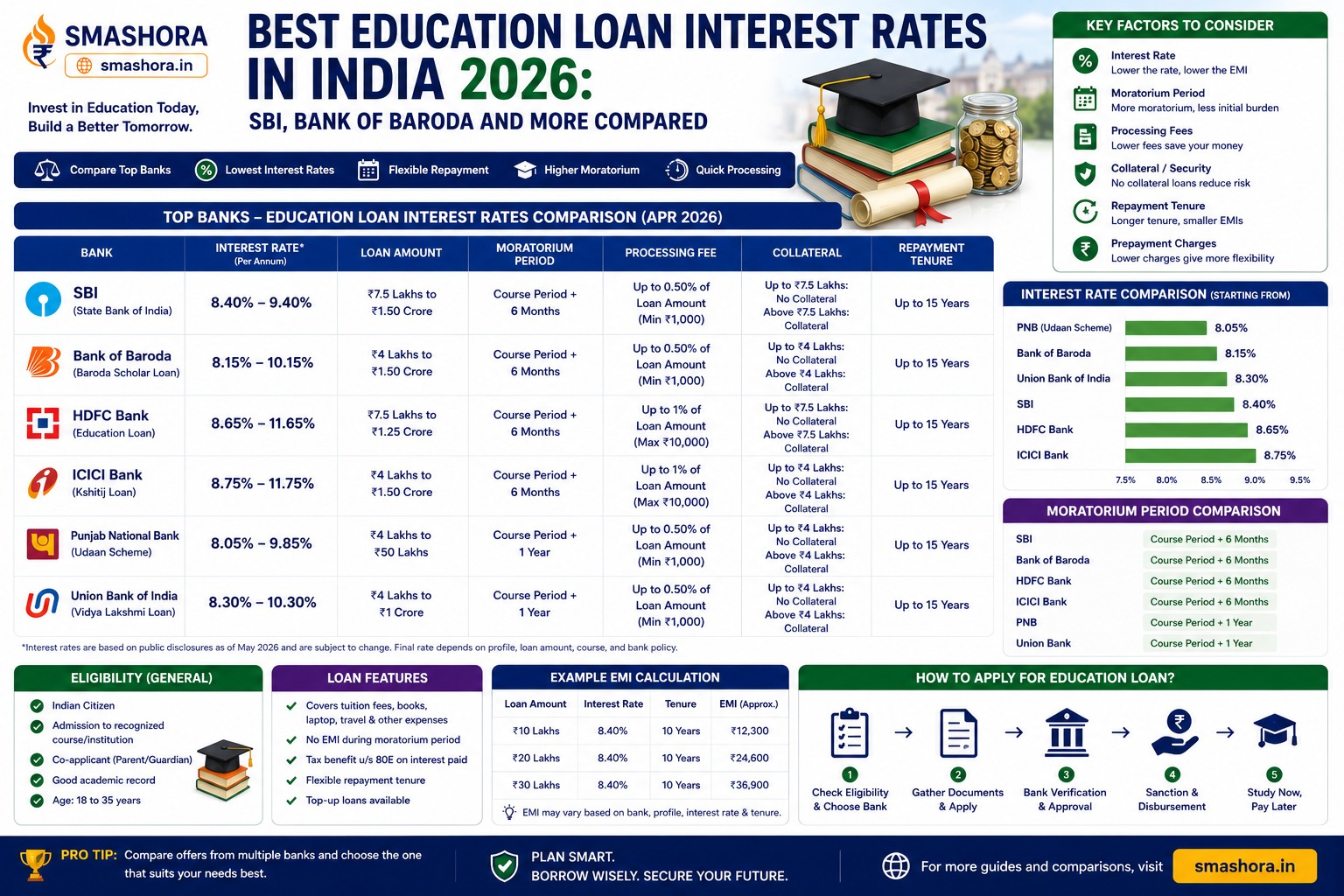

- 2 Best Education Loan Interest Rates in India 2026 — Bank Comparison

- 3 SBI Education Loan 2026 — The Most Detailed Look

- 4 Other Major Banks — Best Education Loan Interest Rates in India 2026

- 5 Education Loan Without Collateral — What You Need to Know

- 6 Best Education Loan Interest Rates in India 2026 — For Studying in India vs Abroad

- 7 Education Loan EMI Calculator — What Will You Pay After Graduation?

- 8 Paying Simple Interest During the Course — A Powerful Strategy

- 9 Section 80E — Tax Benefit on Education Loan Interest

- 10 How to Get the Best Education Loan Interest Rate in India 2026 — Step by Step

- 11 NBFC Education Loans — When to Consider Them

- 12 What Happens If EMIs Are Missed

- 13 Conclusion — Compare the Best Education Loan Interest Rates in India 2026 Before Signing

- 14 Frequently Asked Questions

- 14.1 Which bank offers the best education loan interest rate in India in 2026?

- 14.2 Can I get an education loan without collateral in India in 2026?

- 14.3 What is the moratorium period in an education loan?

- 14.4 What is Section 80E and how much can I save on education loan interest?

- 14.5 Is there an interest rate concession for female students on education loans?

- 14.6 Can I prepay or foreclose an education loan early without penalty?

With admission season for both Indian and overseas universities in full swing, finding the best education loan interest rates in India 2026 can be the difference between a manageable monthly EMI after graduation and a debt burden that follows a young professional for over a decade. Education loan rates in India in 2026 range from as low as 6.90% at SBI’s Scholar Loan Scheme for top-ranked institutions to over 11% at NBFCs for collateral-free loans to lesser-known colleges. On a ₹40 lakh loan over 10 years, that range translates to a difference of well over ₹10 lakh in total interest — money that could instead go toward a young graduate’s first home down payment or emergency fund.

The education loan landscape in India in 2026 has become significantly more sophisticated than it was even five years ago. Public sector banks now offer dedicated schemes for premier institutions with rates that rival personal loan rates for top borrowers, processing has moved largely online through digital partners, and gender-based and insurance-linked interest concessions have become standard across most major lenders. At the same time, families navigating this for the first time often default to whichever bank a relative mentions, missing out on schemes that could save lakhs over the loan tenure.

This complete guide on the best education loan interest rates in India 2026 covers current rates from all major public sector lenders for both domestic and international study, the difference between collateral and non-collateral loans, the moratorium period and how repayment works, Section 80E tax benefits, and exactly how to choose the right loan for your specific admission.

How Education Loans Work in India — The Basics

Before comparing the best education loan interest rates in India 2026, understanding the structure of an education loan helps you evaluate offers correctly:

- Moratorium period: Education loans do not require EMI payments during the course duration plus an additional grace period — typically 6 months to 1 year after course completion. This is called the moratorium period, giving the student time to find employment before repayment begins.

- Simple interest during moratorium: Most lenders charge simple interest (not compounded) during the moratorium period. Some lenders allow students to pay only this simple interest during the course — significantly reducing the total interest burden over the loan tenure.

- Repayment tenure: Typically 10 to 15 years after the moratorium period ends, giving manageable monthly EMIs once the student is employed.

- What is covered: Tuition fees, hostel and accommodation charges, books and study materials, laptop or equipment required for the course, travel expenses for studying abroad, and examination or library fees.

Best Education Loan Interest Rates in India 2026 — Bank Comparison

Here are the current best education loan interest rates in India 2026 from major public sector banks:

| Bank | Interest Rate Range | Max Loan Amount | Collateral-Free Limit |

|---|---|---|---|

| Union Bank of India | 7.10% to 10.50% per year | Up to ₹2 crore (abroad) | Up to ₹7.5 lakh |

| SBI (Scholar Loan Scheme) | 6.90% to 7.65% per year | Up to ₹50 lakh (premier institutions) | Up to ₹7.5 lakh |

| SBI (Global Ed-Vantage) | 8.40% to 10.45% per year | Up to ₹3 crore (28 countries) | Up to ₹7.5 lakh |

| Bank of Baroda | 8.50% to 10.85% per year | Up to ₹1.5 crore (abroad) | Up to ₹7.5 lakh |

| Canara Bank | 8.85% to 10.85% per year | Up to ₹1.5 crore (abroad) | Up to ₹7.5 lakh |

| Punjab National Bank | 8.65% to 11.00% per year | Up to ₹1.5 crore (abroad) | Up to ₹7.5 lakh |

| South Indian Bank | 9.50% to 12.00% per year | Up to ₹50 lakh | Up to ₹7.5 lakh |

| NBFCs (Avanse, Auxilo, Credila) | 10.50% to 14.00% per year | Up to ₹1.5 crore (case basis) | Variable, often collateral-free up to higher limits |

All rates above are floating and indicative as of June 2026 for salaried co-applicants with good credit profiles. For official lending guidelines and current monetary policy context affecting these rates, refer to the Reserve Bank of India website.

SBI Education Loan 2026 — The Most Detailed Look

SBI remains the most popular choice among the best education loan interest rates in India 2026 due to its combination of competitive rates, the widest branch network for processing, and dedicated schemes tailored to different student profiles.

SBI Scholar Loan Scheme — Best for Premier Institutions

The SBI Scholar Loan Scheme offers among the lowest education loan interest rates in India 2026 — ranging from 6.90% to 7.65% — but is exclusively available to students admitted to a specified list of premier institutions including IITs, IIMs, NITs, AIIMS, and other top-ranked Indian and international universities.

- Interest Rate: 6.90% to 7.65% per year

- Eligibility: Admission to a listed premier institution (check the current SBI list as institutions are periodically updated)

- Loan Amount: Up to ₹50 lakh

- Collateral: Not required up to ₹7.5 lakh; above this, parental guarantee or collateral required depending on amount

- Processing Fee: Nil for loans up to ₹4 lakh, nominal for higher amounts

SBI Global Ed-Vantage — Best for Studying Abroad

For students heading abroad to the USA, UK, Canada, Australia, and 24 other countries, SBI Global Ed-Vantage is one of the best education loan interest rates in India 2026 for international education, offering loan amounts up to ₹3 crore.

- Interest Rate: 8.40% to 10.45% per year (8.40% for female students with collateral)

- Loan Amount: ₹7.5 lakh to ₹3 crore for 28 countries

- Tenure: Up to 15 years

- Margin: Nil up to ₹4 lakh, 5% above ₹4 lakh

- Collateral: Required above ₹7.5 lakh — parent or guardian co-borrower with liquid assets or property collateral valued at 100% to 110% of the loan amount

- Processing Fee: Fixed at ₹10,000 plus GST regardless of loan amount — a significant advantage on larger loans where percentage-based fees at other lenders would be much higher

- Approval Time: Typically 14 to 16 working days

- Foreclosure Charges: Zero — you can prepay and close the loan early without any penalty

SBI Interest Rate Concessions

| Concession Type | Rate Reduction | Eligibility |

|---|---|---|

| Female Student Concession | 0.50% | All female applicants across schemes |

| SBI Life Insurance Concession | 0.50% | Student purchases SBI Rinn Raksha or other eligible life insurance policy |

| Combined Concession | Up to 1.00% | Female students who also purchase the eligible insurance policy |

A female student applying under SBI Global Ed-Vantage who also purchases the SBI Rinn Raksha policy could see her effective rate reduced from 9.40% to as low as 8.40% — a combination worth actively pursuing if eligible.

Other Major Banks — Best Education Loan Interest Rates in India 2026

Union Bank of India — Lowest Starting Rate

Union Bank of India offers among the lowest starting education loan rates at 7.10% per year — even lower than SBI’s general schemes — making it one of the best education loan interest rates in India 2026 for students who do not qualify for SBI’s Scholar Loan Scheme but still want a competitive public sector rate.

- Interest Rate: 7.10% to 10.50% per year

- Loan Amount: Up to ₹2 crore for abroad studies

- Collateral-free: Up to ₹7.5 lakh

Bank of Baroda — Strong for Both Domestic and Abroad

- Interest Rate: 8.50% to 10.85% per year

- Loan Amount: Up to ₹1.5 crore for abroad studies

- Multiple schemes: Bank of Baroda offers separate education loan schemes for domestic study, abroad study, and specific premier institution categories — each with its own rate structure

Canara Bank and Punjab National Bank

Both offer competitive rates in the 8.65% to 11% range, with similar collateral-free limits of ₹7.5 lakh and loan amounts up to ₹1.5 crore for studying abroad. These banks are particularly accessible for students in tier-2 and tier-3 cities where branch density is higher than some other public sector banks.

Education Loan Without Collateral — What You Need to Know

One of the most important factors when comparing the best education loan interest rates in India 2026 is the collateral-free limit, which is largely standardised across public sector banks at ₹7.5 lakh:

| Loan Amount | Collateral Requirement | Margin Money |

|---|---|---|

| Up to ₹4 lakh | None — only parent or guardian as co-borrower | Nil |

| ₹4 lakh to ₹7.5 lakh | None — third-party guarantee may be required by some banks | 5% of loan amount (for studies in India), nil for some abroad schemes |

| Above ₹7.5 lakh | Collateral required — property, FD, or other liquid assets typically valued at 100% to 110% of loan amount | 5% (varies by scheme) |

For loans up to ₹50 lakh without collateral, some lenders including SBI under specific schemes for select institutions and certain NBFCs offer collateral-free options, though typically at higher interest rates than collateral-backed loans — often 11% to 11.50% versus 8.90% to 9% for fully secured loans of the same amount.

Best Education Loan Interest Rates in India 2026 — For Studying in India vs Abroad

| Feature | Education Loan for India | Education Loan for Abroad |

|---|---|---|

| Interest Rate Range | 7.10% to 10.50% | 8.40% to 11.50% |

| Maximum Loan Amount | Typically up to ₹50 lakh to ₹75 lakh | Up to ₹3 crore at SBI for select countries |

| Coverage | Tuition, hostel, books, equipment | Tuition, accommodation, travel, insurance, living expenses |

| Documentation Complexity | Simpler — domestic admission letter sufficient | More complex — visa documents, I-20 or equivalent, forex considerations |

| Currency Risk | None | None for the loan itself (rupee-denominated), but actual expenses abroad are subject to forex rates |

Education Loan EMI Calculator — What Will You Pay After Graduation?

Here is a reference table showing approximate EMIs after the moratorium period for common education loan amounts at different interest rates over a 10-year repayment tenure:

| Loan Amount | EMI at 8% — 10 Years | EMI at 9.5% — 10 Years | EMI at 11% — 10 Years |

|---|---|---|---|

| ₹10 lakh | ₹12,133 | ₹12,950 | ₹13,793 |

| ₹25 lakh | ₹30,332 | ₹32,376 | ₹34,481 |

| ₹40 lakh | ₹48,531 | ₹51,801 | ₹55,170 |

| ₹60 lakh | ₹72,797 | ₹77,702 | ₹82,755 |

| ₹1 crore | ₹1,21,328 | ₹1,29,503 | ₹1,37,925 |

On a ₹40 lakh loan over 10 years, the difference between 8% and 11% is approximately ₹6,639 per month — or nearly ₹8 lakh in total additional interest over the loan tenure. This is precisely why comparing the best education loan interest rates in India 2026 across multiple lenders before signing matters so much for large education loans.

Paying Simple Interest During the Course — A Powerful Strategy

Most lenders allow students or their parents to pay simple interest on the disbursed loan amount during the course period (the moratorium), rather than letting it accumulate and compound into the principal at the start of repayment. This single decision can save lakhs over the loan tenure:

| Approach During Moratorium (4-year course, ₹40 lakh loan at 9%) | Principal at Repayment Start | Approximate Total Interest Over 10-Year Repayment |

|---|---|---|

| Pay simple interest during course (approx ₹3.6 lakh per year) | ₹40 lakh | Approximately ₹21 lakh |

| No payment during course — interest compounds into principal | Approximately ₹56.5 lakh | Approximately ₹29.7 lakh |

If the family can manage the modest simple interest payments during the course — often ₹2,000 to ₹4,000 per month on a ₹10 lakh loan tranche — the savings over the full repayment tenure are substantial. This is one of the most underutilised strategies for reducing the effective cost of even the best education loan interest rates in India 2026.

Section 80E — Tax Benefit on Education Loan Interest

One of the most valuable but underused tax benefits in India is Section 80E — a deduction for interest paid on education loans, available under the Old Tax Regime:

- What it covers: Interest paid on an education loan taken for the higher education of self, spouse, children, or a student for whom the taxpayer is a legal guardian

- Deduction amount: No upper limit — the entire interest amount paid during the financial year can be claimed as a deduction

- Eligible courses: Any course of study pursued after passing senior secondary examination — including vocational courses, both in India and abroad

- Duration: Available for 8 consecutive years starting from the year repayment begins, or until the interest is fully repaid, whichever is earlier

- Important: Only the interest component is deductible — principal repayment does not qualify for any deduction under Section 80E

For a parent in the 30% tax bracket paying ₹3 lakh in education loan interest in a year, Section 80E saves approximately ₹93,600 in taxes for that year alone — with no upper limit on this deduction, unlike most other Income Tax Act deductions. For a complete guide on claiming Section 80E along with other deductions when filing your ITR, read our article on how to save tax under Section 80C in India 2026, and for the filing process itself, our guide on filing your return covers the complete e-filing steps.

How to Get the Best Education Loan Interest Rate in India 2026 — Step by Step

- Check institution-specific schemes first: If the admission is to an IIT, IIM, NIT, AIIMS, or another premier institution, check SBI’s Scholar Loan Scheme and similar schemes at other banks first — these offer rates significantly below standard education loan rates

- Compare at least 3 to 4 public sector banks: Rates vary by 1% to 2% across SBI, Union Bank, Bank of Baroda, Canara Bank, and PNB for the same profile — get quotes from multiple lenders

- Apply for the female student concession if applicable: The 0.50% concession applies across most public sector banks, not just SBI

- Consider the linked insurance concession: If a 0.50% rate reduction is available by purchasing an associated life insurance policy, calculate whether the premium cost is lower than the interest saved over the loan tenure — in most cases it is

- Decide on collateral strategically: If the loan amount is close to the ₹7.5 lakh collateral-free threshold, consider whether providing modest collateral (an FD, for instance) to access a collateral-backed rate (often 2% to 3% lower) makes financial sense versus staying collateral-free at a higher rate

- Pay simple interest during the moratorium if possible: Even small monthly payments during the course significantly reduce the principal at repayment start

- Check for zero or fixed processing fees: SBI’s flat ₹10,000 plus GST processing fee on Global Ed-Vantage is significantly better than percentage-based fees at other lenders for large loan amounts — always compare the actual fee in rupees, not just the percentage

NBFC Education Loans — When to Consider Them

NBFCs like Avanse, Auxilo, and Credila specialise in education loans and can be useful in specific situations even though their rates (10.5% to 14%) are generally higher than public sector banks:

- Faster processing: NBFCs often process and disburse loans faster than public sector banks — useful when admission deadlines or visa timelines are tight

- Higher collateral-free limits: Some NBFCs offer collateral-free loans up to ₹40 lakh to ₹50 lakh, well above the ₹7.5 lakh standard at public banks — useful for families without property or FD collateral to pledge

- Coverage for non-listed institutions: NBFCs may finance admissions to institutions not on a public bank’s approved list

- Refinancing strategy: Many students take an NBFC loan initially for speed, then refinance to a public sector bank at a lower rate once employed and credit profile improves — read our guide on how to improve your CIBIL score to build the credit profile needed for a successful refinance

What Happens If EMIs Are Missed

Missing education loan EMIs does not change the original interest rate, but it does carry consequences: penalty interest charges accrue on the missed amount, your CIBIL score is negatively affected — impacting future loan applications including home loans and the best personal loan in India 2026 you might need later — and it can reduce your chances of successfully refinancing or restructuring the loan to a lower rate. If repayment becomes difficult after graduation due to delayed employment, proactively contact the bank to discuss a moratorium extension or restructuring rather than simply missing payments.

Before the repayment period begins, families should also ensure their broader financial foundation is solid. Our guide on how to build an emergency fund in India is particularly relevant for families managing an education loan alongside other obligations — having a buffer prevents a single income disruption from cascading into missed EMIs and credit score damage.

Conclusion — Compare the Best Education Loan Interest Rates in India 2026 Before Signing

The best education loan interest rates in India 2026 start as low as 6.90% for students admitted to premier institutions under SBI’s Scholar Loan Scheme, and 7.10% at Union Bank for general education loans — both significantly below the 9% to 11% range that families often accept by default at the first bank they approach. For studying abroad, SBI Global Ed-Vantage’s combination of competitive rates, fixed processing fee, zero foreclosure charges, and up to ₹3 crore loan amount across 28 countries makes it one of the strongest options in the market for 2026.

The key actions that make the biggest difference: check institution-specific schemes first, compare at least 3 to 4 public sector banks, claim every applicable concession including the female student and insurance-linked rate reductions, pay simple interest during the moratorium if affordable, and claim the unlimited Section 80E deduction on interest paid once repayment begins. Together, these steps can mean the difference between an education loan that becomes a manageable stepping stone and one that becomes a long-term financial burden.

At Smashora, our mission is to help every Indian make every rupee count — including the rupees that fund the next generation’s education. If this guide on the best education loan interest rates in India 2026 helped you or your family plan an upcoming admission, leave a comment below or share it with a parent or student currently comparing education loan offers this admission season.

Frequently Asked Questions

Which bank offers the best education loan interest rate in India in 2026?

For students admitted to premier institutions like IITs, IIMs, NITs, and AIIMS, SBI’s Scholar Loan Scheme offers the best education loan interest rates in India 2026 at 6.90% to 7.65% per year. For general education loans without premier institution admission, Union Bank of India offers the lowest starting rate at 7.10% per year. For studying abroad, SBI Global Ed-Vantage at 8.40% to 10.45% with up to ₹3 crore loan amount across 28 countries, zero foreclosure charges, and a fixed ₹10,000 plus GST processing fee is one of the strongest overall packages available.

Can I get an education loan without collateral in India in 2026?

Yes, education loans up to ₹7.5 lakh are collateral-free at virtually all public sector banks in India in 2026, requiring only a parent or guardian as co-borrower. For loans above ₹7.5 lakh, collateral — typically property, fixed deposits, or other liquid assets valued at 100% to 110% of the loan amount — is generally required at public sector banks. Some NBFCs offer collateral-free loans up to ₹40 lakh to ₹50 lakh for strong profiles and well-ranked institutions, though at higher interest rates of 10.5% to 14% compared to public sector bank rates.

What is the moratorium period in an education loan?

The moratorium period is the duration during which the student is not required to pay EMIs on an education loan — it covers the entire course duration plus an additional grace period, typically 6 months to 1 year after course completion, to allow time for finding employment. During this period, interest typically still accrues on the disbursed amount. Many lenders allow borrowers to pay just this simple interest during the moratorium, which significantly reduces the principal amount when full EMI repayment begins, leading to substantial total interest savings over the loan tenure.

What is Section 80E and how much can I save on education loan interest?

Section 80E of the Income Tax Act allows a deduction for the entire interest amount paid on an education loan during a financial year, with no upper limit — unlike most other tax deductions which are capped. This deduction is available for 8 consecutive years starting from the year loan repayment begins, or until the interest is fully repaid, whichever comes first. It covers education loans taken for self, spouse, children, or a student under legal guardianship, for any course after senior secondary, in India or abroad. For someone in the 30% tax bracket paying ₹3 lakh in education loan interest in a year, this deduction saves approximately ₹93,600 in that year’s taxes. Only the interest is deductible — principal repayment does not qualify.

Is there an interest rate concession for female students on education loans?

Yes. Most major public sector banks in India, including SBI, offer a 0.50% interest rate concession for female students on education loans across multiple schemes. Some banks also offer an additional 0.50% concession if the student purchases an associated life insurance policy — for example, SBI’s Rinn Raksha policy. Combined, female students who also opt for the eligible insurance policy can reduce their effective education loan interest rate by up to 1.00% compared to the standard rate, making a meaningful difference on large education loans over a 10 to 15 year repayment tenure.

Can I prepay or foreclose an education loan early without penalty?

This depends on the lender and scheme. SBI’s Global Ed-Vantage scheme for studying abroad explicitly has zero foreclosure charges, meaning you can prepay and close the loan early at any time without any penalty — a significant advantage if your income grows faster than expected after graduation and you want to clear the debt ahead of schedule. Always check the specific foreclosure terms of your chosen scheme before signing, as policies vary across lenders and even across different schemes at the same bank.