Contents

- 1 Two Paths to Saving Tax on Salary in India 2026

- 2 How to Save Income Tax on Salary in India 2026 — Available Under BOTH Regimes

- 2.1 1. Standard Deduction — ₹75,000 Under New Regime, ₹50,000 Under Old Regime

- 2.2 2. Employer NPS Contribution — Section 80CCD(2)

- 2.3 3. Employer-Provided Meal Vouchers or Food Benefits

- 2.4 4. Employer Gifts and Festival Vouchers — Now ₹15,000 Tax-Free

- 2.5 5. Car Perquisite Structuring

- 2.6 6. Leave Encashment at Retirement or Resignation

- 2.7 7. Gratuity Exemption

- 3 How to Save Income Tax on Salary in India 2026 — Old Tax Regime Specific Strategies

- 3.1 8. House Rent Allowance (HRA) Exemption

- 3.2 9. Leave Travel Allowance (LTA)

- 3.3 10. Section 80C — Up to ₹1.5 Lakh Deduction

- 3.4 11. Section 80D — Health Insurance Premium

- 3.5 12. Additional NPS Contribution — Section 80CCD(1B)

- 3.6 13. Home Loan Interest — Section 24(b)

- 3.7 14. Education Allowance and Hostel Allowance

- 4 Complete Tax-Saving Checklist for Salaried Employees — FY 2026-27

- 5 Form 12BB — How to Declare Your Tax-Saving Investments to Your Employer

- 6 How to Save Income Tax on Salary in India 2026 — Salary-Wise Summary

- 7 Conclusion — Start Tax Planning in April, Not March

- 8 Frequently Asked Questions

- 8.1 How can I save the most income tax on my salary in India in 2026?

- 8.2 Is HRA tax-free in India in 2026?

- 8.3 Can I claim HRA and home loan interest deduction simultaneously in India?

- 8.4 What is Form 12BB and when should I submit it?

- 8.5 Can I save tax on salary under the New Tax Regime in India in 2026?

- 8.6 What is the new metro city list for HRA exemption in India 2026?

Every salaried Indian in 2026 has one question before the July 31 ITR deadline — exactly how to save income tax on salary in India 2026 without missing any legitimate deduction or exemption. The Indian tax system for salaried employees offers a surprisingly wide range of legal tax-saving tools — from the well-known House Rent Allowance exemption and Section 80C investments to several lesser-known salary components like meal vouchers, education allowances, and employer NPS contributions that work even under the New Tax Regime.

Most salaried employees leave significant tax money on the table every year — not through illegal means, but simply through ignorance of what they are legally entitled to claim. A colleague earning ₹15 lakh per year had been paying approximately ₹35,000 more in income tax than necessary for three consecutive years because he had not declared his rent payments to his employer for HRA exemption, had not asked HR to enrol him in the company NPS scheme, and had not realised his parents’ health insurance premium qualified for an additional 80D deduction. When he corrected all three for AY 2026-27, his tax liability dropped by ₹34,000 — entirely within the law.

This complete guide on how to save income tax on salary in India 2026 covers every legally available tax-saving tool for salaried employees under both the Old and New Tax Regimes — with updated FY 2026-27 figures, salary-wise examples, and a practical checklist so you do not miss a single rupee of legitimate tax saving before the ITR filing deadline.

Two Paths to Saving Tax on Salary in India 2026

Before listing specific strategies for how to save income tax on salary in India 2026, understanding which path applies to you sets the context:

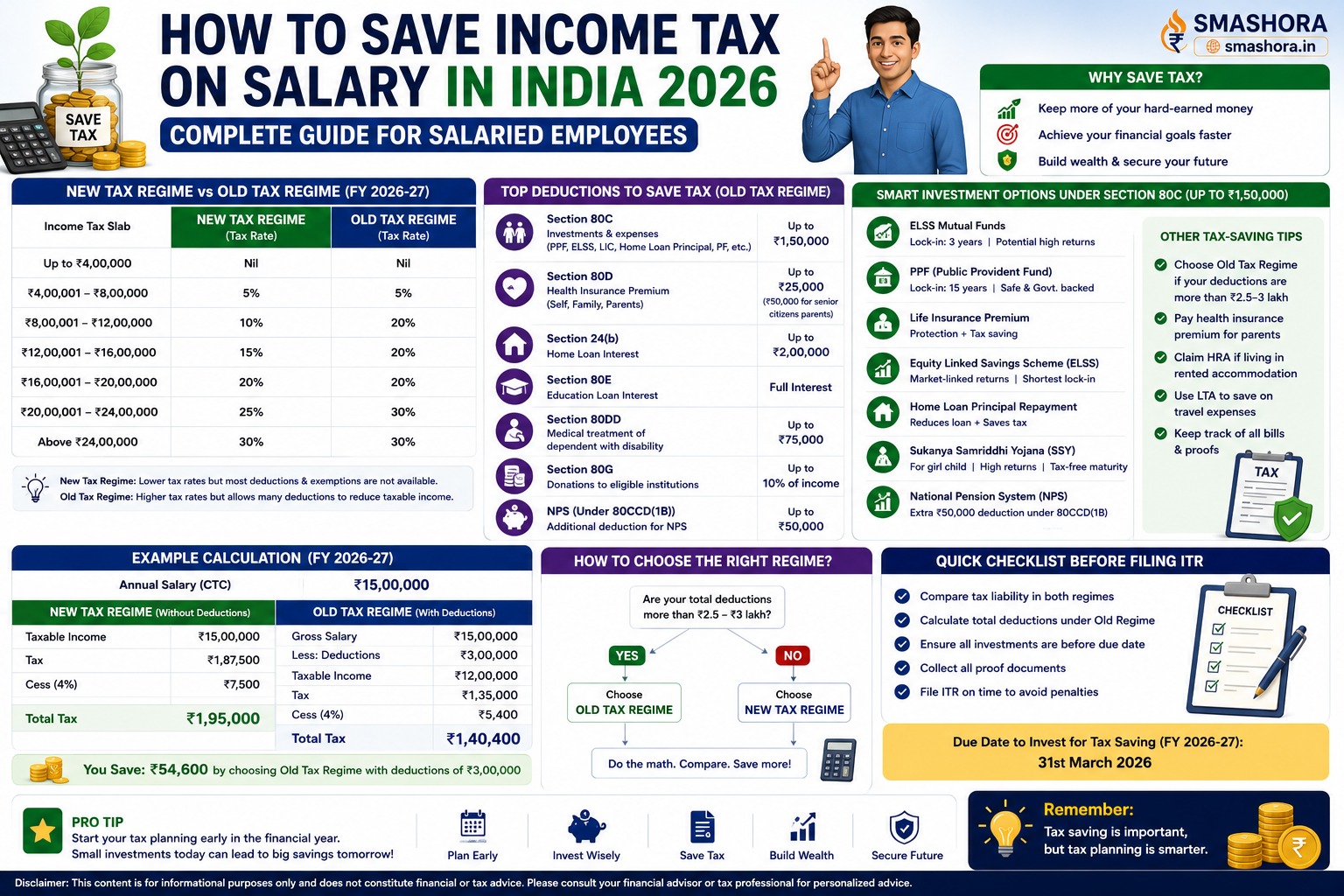

- New Tax Regime (Default for FY 2025-26): Lower slab rates, ₹75,000 standard deduction, zero tax up to ₹12 lakh with 87A rebate — but most exemptions and deductions are NOT available. A smaller but still meaningful set of tax-saving options survive under the new regime.

- Old Tax Regime: Higher slab rates, ₹50,000 standard deduction — but all major salary exemptions (HRA, LTA) and investment deductions (80C, 80D, home loan interest) ARE available. Better for salaried employees with significant deductions to claim.

The strategies below are clearly labelled by which regime they are available in. For the complete regime comparison with salary-wise worked examples, read our detailed guide on the new tax regime vs old tax regime in India 2026.

How to Save Income Tax on Salary in India 2026 — Available Under BOTH Regimes

These strategies reduce your tax liability regardless of which regime you choose:

1. Standard Deduction — ₹75,000 Under New Regime, ₹50,000 Under Old Regime

The standard deduction is automatically available to all salaried employees and pensioners — no declaration, no proof, no documentation required. You do not need to do anything to claim it. Your employer deducts it automatically when computing TDS.

- New Tax Regime: ₹75,000 standard deduction

- Old Tax Regime: ₹50,000 standard deduction

On a gross salary of ₹12.75 lakh under the new regime, the ₹75,000 standard deduction brings the taxable income to ₹12 lakh — which then attracts zero tax under the Section 87A rebate. This makes income up to ₹12.75 lakh completely tax-free under the new regime in 2026.

2. Employer NPS Contribution — Section 80CCD(2)

This is the single most powerful salary-based tax-saving strategy available under both regimes and is significantly underutilised. When your employer contributes to your NPS (National Pension System) Tier 1 account as part of your CTC structure, that contribution is fully deductible from your taxable income under Section 80CCD(2) — up to 10% of basic salary for private sector employees and 14% for government employees.

This benefit applies even under the New Tax Regime — making it the only major deduction that survives the new regime alongside the standard deduction.

| Basic Salary Per Month | Annual Basic Salary | 10% Employer NPS Contribution | Tax Saving (30% Slab) |

|---|---|---|---|

| ₹30,000 | ₹3.6 lakh | ₹36,000 | ₹11,232 |

| ₹50,000 | ₹6 lakh | ₹60,000 | ₹18,720 |

| ₹75,000 | ₹9 lakh | ₹90,000 | ₹28,080 |

| ₹1,00,000 | ₹12 lakh | ₹1,20,000 | ₹37,440 |

If your employer does not currently offer NPS as part of your CTC, ask your HR team proactively — many companies will restructure the CTC to include NPS contributions if an employee requests it. The employer saves on their tax liability too, making it a win-win CTC restructuring. For the complete NPS guide, read our article on NPS vs PPF in India 2026.

3. Employer-Provided Meal Vouchers or Food Benefits

Meal vouchers and food benefits provided by your employer are exempt from income tax up to ₹50 per meal, effectively ₹26,400 per year (assuming 22 working days per month, 2 meals per day). Many companies offer Sodexo or similar digital meal cards as part of CTC that fall under this exemption.

- Available: Both Old and New Tax Regime

- Annual tax-free limit: Approximately ₹26,400 per year

- Tax saving at 30% slab: Approximately ₹8,237 per year

4. Employer Gifts and Festival Vouchers — Now ₹15,000 Tax-Free

From FY 2026-27, employer-provided gifts, festival vouchers, or occasion-based perquisites are tax-free up to ₹15,000 per year — increased from the previous ₹5,000 limit. If your employer gives festival bonuses in the form of gift vouchers rather than cash, the first ₹15,000 is completely tax-free.

- Available: Both Old and New Tax Regime

- Annual tax-free limit: ₹15,000 per year

- Tax saving at 30% slab: ₹4,680 per year on maximum benefit

5. Car Perquisite Structuring

If your employer provides a company car for official and personal use, the perquisite value is taxed at a prescribed rate far below the actual car operating cost — typically ₹1,800 to ₹2,400 per month for cars up to 1600cc and ₹2,400 to ₹3,000 per month for larger cars. For employees who use a company-owned car extensively for personal use, this is a far more tax-efficient arrangement than receiving the equivalent car allowance in cash salary.

- Available: Both Old and New Tax Regime

- Benefit: Actual car operating cost far exceeds the taxable perquisite value

6. Leave Encashment at Retirement or Resignation

Leave encashment at the time of retirement is tax-free up to ₹25 lakh for private sector employees (increased in recent budgets) and fully exempt for government employees. Leave encashment during service (not at retirement) is taxable, but the lump sum received at retirement or separation benefits significantly from this exemption.

7. Gratuity Exemption

Gratuity received on retirement, death, or resignation after 5 or more years of continuous service is tax-free up to ₹20 lakh for private sector employees. Government employees receive full gratuity exemption without any monetary cap. This is a significant retirement benefit that requires no action from the employee during their working years — it applies automatically.

How to Save Income Tax on Salary in India 2026 — Old Tax Regime Specific Strategies

These strategies apply only if you have opted for the Old Tax Regime for AY 2026-27:

8. House Rent Allowance (HRA) Exemption

HRA is the most significant salary component for tax saving in the old tax regime for employees who live in rented accommodation. The HRA exemption is the minimum of:

- Actual HRA received from employer

- Actual rent paid minus 10% of basic salary

- 50% of basic salary for metro cities (Mumbai, Delhi, Kolkata, Chennai, Bengaluru, Hyderabad, Pune, Ahmedabad) OR 40% of basic salary for other cities

Important 2026 update: Bengaluru, Hyderabad, Pune, and Ahmedabad have now been officially included in the expanded metro city list for 50% HRA calculation — up from the traditional four metros. This benefits employees in these cities significantly, as the 50% rate gives a higher exemption than the 40% that previously applied.

| Parameter | Example (Bengaluru, ₹60,000 Basic) |

|---|---|

| Monthly Basic Salary | ₹60,000 |

| Monthly HRA from Employer | ₹25,000 |

| Monthly Rent Paid | ₹22,000 |

| Actual HRA received | ₹25,000 |

| Rent paid minus 10% of basic | ₹22,000 minus ₹6,000 = ₹16,000 |

| 50% of basic (metro) | ₹30,000 |

| HRA Exemption (minimum of above three) | ₹16,000 per month = ₹1,92,000 per year |

| Tax Saving at 30% Slab | ₹59,904 per year |

Paying rent to parents: You can pay rent to your parents and claim HRA exemption — even if you live in a house owned by your parents. Your parents must include the rent received in their own income tax return. If your parents are in a lower tax slab than you (or below the taxable limit), this is a legitimate and highly effective tax-saving strategy used by millions of Indian salaried professionals.

Documentation required: Submit rent receipts to your employer for months where rent exceeds ₹3,000 per month. If annual rent exceeds ₹1 lakh, you must also submit the landlord’s PAN card number to your employer.

9. Leave Travel Allowance (LTA)

LTA allows you to claim exemption on actual travel expenses for domestic travel in India — covering you, your spouse, children, and dependent parents — for up to 2 journeys in a 4-year block period. The current LTA block period is 2026 to 2029.

- Available: Old Tax Regime only

- Coverage: Economy air travel, AC rail travel, or AC bus travel — actual fare for the shortest route to the destination

- Documentation: Travel tickets and boarding passes must be submitted to your employer

- Block period: 2026 to 2029 — you can claim 2 LTA exemptions in these 4 years

- Important: Only the travel fare is covered — hotel accommodation, food, and local transport are not part of the LTA exemption

10. Section 80C — Up to ₹1.5 Lakh Deduction

The foundation of how to save income tax on salary in India 2026 under the old regime is maximising the ₹1.5 lakh Section 80C deduction. First count what you already contribute automatically — EPF contributions from your salary, children’s tuition fees, home loan principal repayment — then fill the remaining gap with ELSS SIPs or PPF contributions.

For a complete guide on every 80C option with current returns, lock-in periods, and a strategy for different income levels, read our detailed article on how to save tax under Section 80C in India 2026.

11. Section 80D — Health Insurance Premium

- Self, spouse and children health insurance: Up to ₹25,000 deduction per year

- Parents below 60 years: Additional ₹25,000 per year

- Senior citizen parents (60 plus): Additional ₹50,000 per year

- Maximum combined deduction: Up to ₹75,000 per year for an individual with senior citizen parents

- Available: Old Tax Regime only

12. Additional NPS Contribution — Section 80CCD(1B)

Over and above the 80C limit, you can invest an additional ₹50,000 per year in NPS Tier 1 under Section 80CCD(1B) and claim it as a separate deduction — completely independent of and above the ₹1.5 lakh 80C ceiling.

- Available: Old Tax Regime only (the personal contribution 80CCD(1B) — not the employer contribution 80CCD(2) which works in both regimes)

- Additional deduction: ₹50,000 per year

- Tax saving at 30% slab: ₹15,600 per year

13. Home Loan Interest — Section 24(b)

- Deduction: Up to ₹2 lakh per year on interest paid on home loan for self-occupied residential property

- Available: Old Tax Regime only for self-occupied property (available in new regime only for let-out property)

- Tax saving at 30% slab: Up to ₹62,400 per year on the full ₹2 lakh deduction

14. Education Allowance and Hostel Allowance

For salaried parents with school-going children, education and hostel allowances in your salary structure give significant tax-free amounts from FY 2026-27 — significantly revised upward:

- Education allowance: ₹3,000 per month per child (maximum 2 children) — increased from ₹100 per month

- Hostel allowance: ₹9,000 per month per child (maximum 2 children) — increased from ₹300 per month

- Combined maximum for 2 children: ₹72,000 per year tax-free

- Available: Old Tax Regime only

If your salary structure does not currently include these allowances, ask your HR team to restructure your CTC to include them — these are employer-declared allowances that your company can include in your salary package without affecting your net take-home, while reducing your tax liability significantly.

Complete Tax-Saving Checklist for Salaried Employees — FY 2026-27

| Tax-Saving Option | Max Benefit | Regime | Action Required |

|---|---|---|---|

| Standard Deduction | ₹75,000 (new), ₹50,000 (old) | Both | Automatic — no action needed |

| Employer NPS 80CCD(2) | 10% of basic salary | Both | Ask HR to include in CTC |

| Meal vouchers | ₹26,400 per year | Both | Ask HR to include in CTC |

| Festival gift vouchers | ₹15,000 per year | Both | Ask HR to give as vouchers, not cash |

| HRA Exemption | Calculated (rent based) | Old only | Submit rent receipts to employer (Form 12BB) |

| LTA | Actual travel fare | Old only | Submit travel tickets to employer |

| Section 80C | Up to ₹1.5 lakh | Old only | Declare investments in Form 12BB |

| Section 80D (Health Insurance) | Up to ₹75,000 | Old only | Submit premium receipts to employer |

| NPS 80CCD(1B) | ₹50,000 | Old only | Invest in NPS Tier 1, declare to employer |

| Home Loan Interest 24(b) | Up to ₹2 lakh | Old only | Submit bank interest certificate to employer |

| Education and Hostel Allowance | Up to ₹72,000 per year | Old only | Ask HR to restructure CTC to include |

Form 12BB — How to Declare Your Tax-Saving Investments to Your Employer

Form 12BB is the declaration form you submit to your employer at the beginning of the financial year (April) to inform them of all tax-saving investments and exemptions you plan to claim for the year. This tells your employer exactly how much TDS to deduct from your salary each month.

Form 12BB includes four sections:

- Section 1: HRA — details of rent paid, landlord’s name, address, and PAN (if annual rent exceeds ₹1 lakh)

- Section 2: LTA — details of travel undertaken and expense amount

- Section 3: Home loan interest — annual interest certificate from lender, name and PAN of lender

- Section 4: All other deductions — Section 80C investments, 80D health insurance, 80CCD(1B) NPS, and any other deductions

If you miss submitting Form 12BB to your employer, your employer deducts higher TDS assuming no deductions. You can still claim all your deductions when filing your ITR before the July 31 deadline and receive any excess TDS as a refund. However, submitting Form 12BB at the start of the year prevents unnecessary TDS deductions throughout the year, giving you better monthly cash flow. For a step-by-step guide on the complete ITR filing process, read our article on how to file ITR online in India 2026.

How to Save Income Tax on Salary in India 2026 — Salary-Wise Summary

| Gross Annual Salary | Best Strategy | Approximate Maximum Tax Saving |

|---|---|---|

| Up to ₹12.75 lakh | New regime — zero tax with standard deduction and 87A rebate | Zero tax payable — no further action needed |

| ₹13 lakh to ₹15 lakh | New regime with employer NPS 80CCD(2), meal vouchers, gift vouchers | ₹30,000 to ₹50,000 via employer restructuring |

| ₹15 lakh to ₹20 lakh | Old regime if HRA, full 80C, 80D, and NPS exceed ₹3.75 lakh combined | ₹50,000 to ₹1.1 lakh total tax saving vs new regime |

| ₹20 lakh to ₹30 lakh | Old regime with maximum deductions including home loan interest, 80D, NPS, HRA | ₹1 lakh to ₹1.6 lakh total tax saving vs new regime |

| Above ₹30 lakh | Old regime for maximum deductions, or new regime if deductions below ₹5.43 lakh | Calculate individual basis with tax calculator |

Conclusion — Start Tax Planning in April, Not March

The single most powerful insight about how to save income tax on salary in India 2026 is that tax planning done in April — at the start of the financial year — saves far more than tax planning done in January or February when most people scramble to invest before the year-end deadline. Starting in April means your SIPs earn returns for the full year, your HRA declarations result in lower TDS all 12 months giving better monthly cash flow, and your NPS contributions compound for longer.

Use this practical action list: submit Form 12BB to your employer with HRA rent details by April 15, ask HR to include employer NPS and meal vouchers in your CTC if not already there, start your ELSS SIP in April rather than waiting for a March lump sum, and calculate whether old or new regime saves you more using the official income tax calculator at incometax.gov.in. These steps together ensure you pay the minimum legally required income tax on your salary in India in 2026 — and keep every remaining rupee working for your future.

At Smashora, our mission is to help every Indian make every rupee count — including the rupees you can save by planning your salary taxes correctly. If this guide on how to save income tax on salary in India 2026 helped you identify a deduction you were missing, leave a comment below or share it with a colleague before the July 31 ITR filing deadline.

Frequently Asked Questions

How can I save the most income tax on my salary in India in 2026?

To save the maximum income tax on salary in India in 2026 under the Old Tax Regime, maximise all available deductions simultaneously: HRA exemption (submit rent receipts to employer), full ₹1.5 lakh Section 80C (EPF plus ELSS plus PPF), additional ₹50,000 under NPS 80CCD(1B), up to ₹75,000 under Section 80D for self and senior parent health insurance, up to ₹2 lakh under Section 24(b) for home loan interest, LTA claim for the 2026 to 2029 block, and employer NPS 80CCD(2) contribution under both regimes. Combined, these deductions can reduce a ₹25 lakh salary’s taxable income by ₹5 lakh to ₹7 lakh, saving ₹1.5 lakh to ₹2 lakh in total annual tax.

Is HRA tax-free in India in 2026?

HRA (House Rent Allowance) is partially tax-exempt under the Old Tax Regime for salaried employees who live in rented accommodation. The exempt amount is the minimum of: actual HRA received, rent paid minus 10% of basic salary, or 50% of basic salary for employees in metro cities (now expanded to include Mumbai, Delhi, Kolkata, Chennai, Bengaluru, Hyderabad, Pune, and Ahmedabad) or 40% of basic salary for other cities. HRA is NOT exempt under the New Tax Regime — employees who switch to the new regime lose this exemption entirely.

Can I claim HRA and home loan interest deduction simultaneously in India?

Yes, you can claim both HRA exemption and home loan interest deduction under Section 24(b) in the same year under the Old Tax Regime, provided you have a genuine reason for both — for example, if you have bought a house in one city but work and live on rent in another city, or if your purchased home is under construction and you live on rent in the interim. Simply owning a house in the same city where you live on rent is typically scrutinised by the income tax department, and genuine justification should be documented.

What is Form 12BB and when should I submit it?

Form 12BB is the investment declaration form you submit to your employer at the beginning of the financial year — ideally by April 15 — to inform them of all tax-saving investments and exemptions you plan to claim. It covers HRA rent details, LTA travel claims, home loan interest, and all Section 80C and other investment declarations. Submitting Form 12BB ensures your employer deducts the correct (lower) TDS from your salary each month throughout the year. If you miss submitting it, your employer deducts higher TDS assuming no deductions — you can reclaim the excess through an ITR filing before the July 31 deadline, but your monthly cash flow suffers throughout the year from over-deducted TDS.

Can I save tax on salary under the New Tax Regime in India in 2026?

Yes, though the options are more limited than the Old Tax Regime. Under the New Tax Regime in India in 2026, the tax-saving options available are: ₹75,000 standard deduction (automatic), employer NPS contribution under Section 80CCD(2) (up to 10% of basic salary), meal vouchers up to approximately ₹26,400 per year, employer gift vouchers up to ₹15,000 per year, and retirement benefits like gratuity and EPF maturity that remain tax-free under both regimes. HRA, LTA, 80C, 80D, 80CCD(1B) personal NPS, and home loan interest for self-occupied property are NOT available under the new regime.

What is the new metro city list for HRA exemption in India 2026?

From FY 2026-27, the expanded metro city list eligible for the 50% of basic salary HRA calculation now includes Mumbai, Delhi, Kolkata, Chennai, Bengaluru, Hyderabad, Pune, and Ahmedabad. Previously, only the traditional four metros — Mumbai, Delhi, Kolkata, and Chennai — qualified for the 50% rate, while all other cities including Bengaluru, Hyderabad, Pune, and Ahmedabad were limited to 40% of basic salary. This expansion significantly benefits employees in these four newly added cities, as the 50% rate generates a meaningfully higher HRA exemption than the previous 40% that applied to them.