Contents

- 1 NPS vs PPF in India 2026 — Quick Overview

- 2 What is NPS and How Does It Work?

- 3 The Most Important NPS Advantage Over PPF — Section 80CCD(1B)

- 4 NPS vs PPF Returns Comparison in India 2026

- 5 NPS vs PPF Tax Treatment — The Full Picture

- 6 NPS vs PPF Lock-in and Withdrawal Rules Compared

- 7 NPS vs PPF in India 2026 — Who Should Choose Which?

- 8 Can You Invest in Both NPS and PPF at the Same Time?

- 9 How to Open an NPS Account in India in 2026

- 10 NPS vs PPF — The Role of Employer Contribution in NPS

- 11 Conclusion — NPS vs PPF in India 2026 Is Not Either-Or

- 12 Frequently Asked Questions

- 12.1 Which is better — NPS or PPF in India in 2026?

- 12.2 What is the Section 80CCD(1B) benefit of NPS?

- 12.3 Can I withdraw from NPS before retirement?

- 12.4 What happens to NPS at retirement (age 60)?

- 12.5 Is NPS available under the New Tax Regime in 2026?

- 12.6 How do I open an NPS account online in India in 2026?

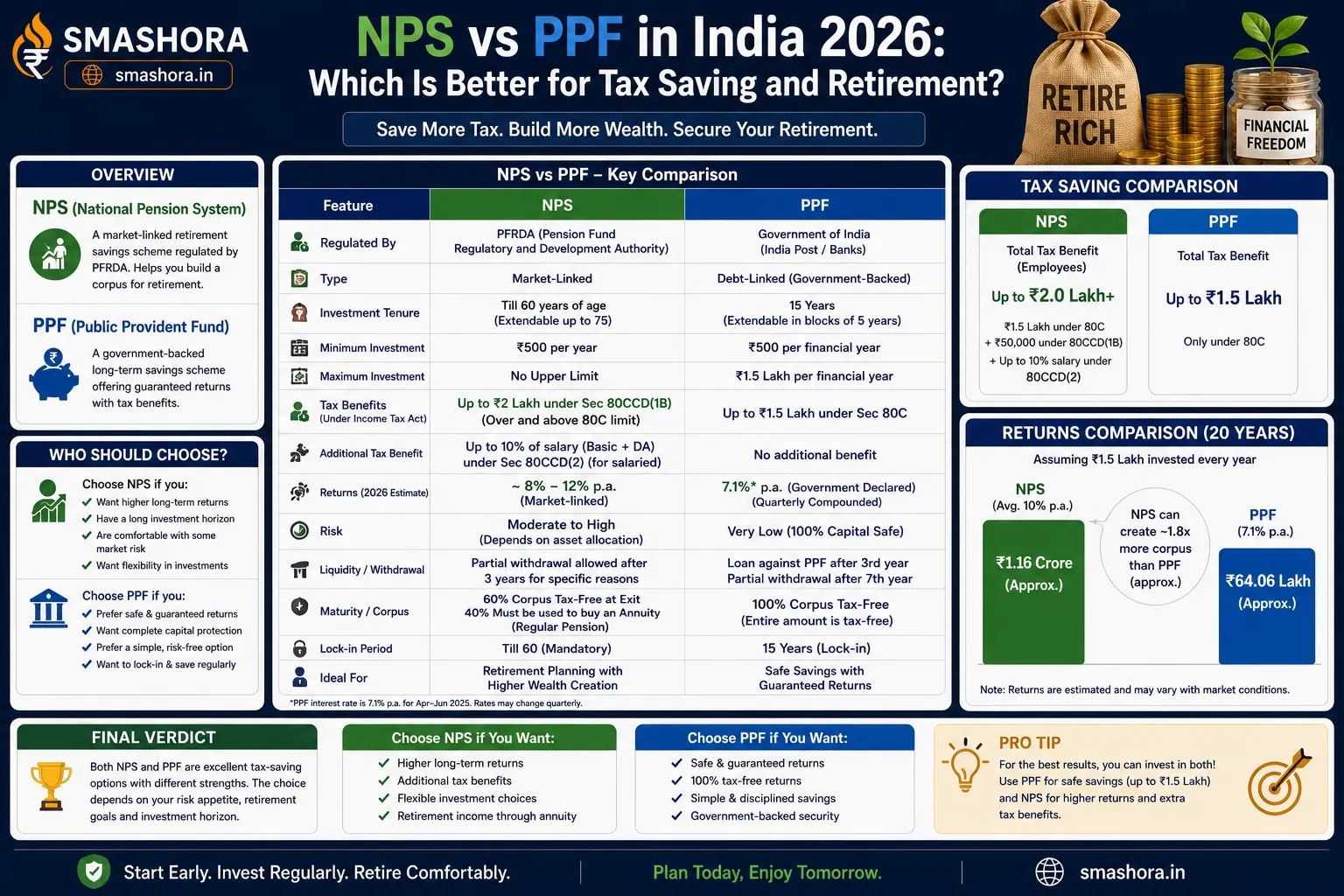

The NPS vs PPF in India 2026 debate has never been more relevant. With the July 31 ITR deadline approaching and millions of salaried Indians actively comparing their tax-saving options, NPS and PPF remain the two most discussed long-term government-backed investment choices. Both are safe. Both offer tax benefits. Both are designed for long-term wealth building. But they work very differently — and choosing the wrong one for your situation can cost you lakhs in either missed returns or missed tax savings over a 20 to 30 year career.

I have heard this question dozens of times from colleagues and friends. A software engineer earning ₹18 lakh per year recently asked me whether to open an NPS account or increase his PPF contribution. He had already maxed out his ₹1.5 lakh 80C limit through EPF and ELSS. The answer for him was clear: NPS under Section 80CCD(1B) gave him an additional ₹50,000 deduction beyond the 80C ceiling — saving him ₹15,600 per year in taxes that PPF simply could not offer him at that point. That is money that goes directly into building his retirement corpus instead of going to the government.

This complete guide on NPS vs PPF in India 2026 covers every dimension of the comparison — returns, tax treatment, lock-in, withdrawal rules, risk, and which type of investor should choose which option. By the end you will have a clear, specific answer for your own financial situation.

NPS vs PPF in India 2026 — Quick Overview

Before going deep, here is a side-by-side snapshot of NPS vs PPF in India 2026:

| Feature | NPS (National Pension System) | PPF (Public Provident Fund) |

|---|---|---|

| Type | Market-linked pension scheme | Government-backed savings scheme |

| Regulated By | PFRDA (Pension Fund Regulatory and Development Authority) | Government of India (Ministry of Finance) |

| Returns | 9% to 12% per year (historical, equity-heavy portfolios) | 7.1% per year (guaranteed, government-set) |

| Returns Type | Market-linked — not guaranteed | Government-guaranteed — fixed |

| Risk | Moderate — equity and debt mix | Zero — sovereign guarantee |

| Minimum Investment | ₹500 per year (Tier 1) | ₹500 per year |

| Maximum Investment | No upper limit | ₹1.5 lakh per year |

| Lock-in Period | Until age 60 (with limited withdrawals) | 15 years (extendable) |

| Tax Deduction — 80C | Up to ₹1.5 lakh under 80CCD(1) | Up to ₹1.5 lakh under 80C |

| Additional Tax Deduction | Extra ₹50,000 under 80CCD(1B) — exclusive to NPS | Not available |

| Tax on Returns | Partially taxable at exit (annuity income taxable) | Completely tax free (EEE) |

| Maturity Withdrawal | 60% tax-free lump sum, 40% mandatory annuity | 100% tax-free lump sum |

What is NPS and How Does It Work?

The National Pension System is a voluntary, market-linked retirement savings scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It was originally designed for government employees but is now open to all Indian citizens between ages 18 and 70.

In NPS, your contributions are invested across three asset classes based on the allocation you choose:

- Asset Class E (Equity): Invested in index funds and equity instruments — highest growth potential, highest volatility

- Asset Class C (Corporate Bonds): Invested in fixed income corporate bonds — moderate risk and returns

- Asset Class G (Government Securities): Invested in government bonds — lowest risk, lowest returns

NPS has two account types. Tier 1 is the mandatory retirement account with strict withdrawal restrictions but full tax benefits. Tier 2 is a voluntary savings account with no restrictions but no additional tax benefits.

Your NPS contributions are managed by empanelled Pension Fund Managers — SBI Pension Fund, HDFC Pension, ICICI Prudential Pension, UTI Retirement Solutions, and others. You choose both your fund manager and your asset allocation. For more information on NPS rules and fund performance, visit the NPS Trust official website.

The Most Important NPS Advantage Over PPF — Section 80CCD(1B)

When comparing NPS vs PPF in India 2026, the single biggest advantage NPS has over PPF is the Section 80CCD(1B) deduction — an additional ₹50,000 tax deduction that is available exclusively for NPS Tier 1 contributions and is completely separate from and over the ₹1.5 lakh Section 80C ceiling.

Here is why this matters enormously for higher-income salaried Indians:

| Scenario | PPF Only | PPF plus NPS 80CCD(1B) |

|---|---|---|

| 80C investment (PPF, EPF, ELSS etc.) | ₹1,50,000 | ₹1,50,000 |

| NPS 80CCD(1B) additional deduction | Not available | ₹50,000 |

| Total deduction from taxable income | ₹1,50,000 | ₹2,00,000 |

| Extra tax saved (30% slab plus cess) | Nil | ₹15,600 per year |

| Extra tax saved over 20 years | Nil | ₹3,12,000 in direct tax savings |

For anyone who has already exhausted the ₹1.5 lakh 80C limit through EPF, ELSS, and PPF, investing ₹50,000 per year in NPS Tier 1 saves an additional ₹15,600 in annual taxes — and builds a retirement corpus simultaneously. This is one of the most underutilised tax benefits available to salaried Indians in 2026.

NPS vs PPF Returns Comparison in India 2026

The NPS vs PPF in India 2026 comparison on returns is where the two instruments diverge most clearly:

PPF Returns

PPF currently offers 7.1% per year, compounded annually, with a complete government guarantee on both principal and returns. The rate is reviewed quarterly but has been remarkably stable — ranging between 7% and 8% over the past 5 years. PPF returns are 100% predictable, completely risk-free, and entirely tax free at all stages.

NPS Returns (Historical)

NPS returns depend entirely on your asset allocation — specifically how much of your portfolio is in Asset Class E (equity). Here are the historical returns delivered by NPS Tier 1 equity plans across fund managers:

| NPS Fund Manager | 1-Year Return | 5-Year Return | 10-Year Return |

|---|---|---|---|

| SBI Pension Fund (Scheme E) | 18.2% | 16.8% | 13.5% |

| HDFC Pension Fund (Scheme E) | 19.1% | 17.3% | 14.2% |

| ICICI Prudential Pension (Scheme E) | 17.8% | 16.5% | 13.8% |

| UTI Retirement Solutions (Scheme E) | 18.5% | 17.0% | 13.3% |

These equity returns are significantly higher than PPF’s 7.1% over long periods. However, they are not guaranteed — NPS equity returns fluctuate with the market and can be negative in down years. The comparison of NPS vs PPF in India 2026 on returns is therefore a comparison of potential higher return with risk against guaranteed modest return with certainty.

Projected Corpus Comparison — ₹50,000 Per Year Over 20 Years

| Investment | Annual Amount | Assumed Rate | Projected Corpus After 20 Years |

|---|---|---|---|

| PPF | ₹50,000 | 7.1% | Approximately ₹27 lakh |

| NPS (50% equity, 50% debt) | ₹50,000 | 10% (blended) | Approximately ₹32 lakh |

| NPS (75% equity, 25% debt) | ₹50,000 | 12% (blended) | Approximately ₹40 lakh |

The projections above show a potential ₹13 lakh difference in corpus between PPF and an equity-heavy NPS on the same ₹50,000 annual investment over 20 years — but the NPS figure is based on historical returns, not guaranteed.

NPS vs PPF Tax Treatment — The Full Picture

Tax treatment is the most nuanced part of the NPS vs PPF in India 2026 comparison and it is where PPF actually has a meaningful advantage over NPS at the withdrawal stage:

| Tax Stage | PPF | NPS Tier 1 |

|---|---|---|

| Tax on Investment (Entry) | 80C deduction up to ₹1.5 lakh | 80CCD(1) up to ₹1.5 lakh plus 80CCD(1B) extra ₹50,000 |

| Tax on Annual Returns (Accumulation) | Tax free every year | Tax free every year |

| Tax on Maturity Lump Sum (Exit) | 100% tax free | 60% tax free, 40% mandatory annuity purchase |

| Tax on Pension (Post-Exit) | Not applicable — full lump sum | Annuity income taxable as income from other sources at slab rate |

| Overall Tax Framework | EEE — Exempt, Exempt, Exempt | EET — Exempt, Exempt, Partially Taxed |

PPF follows a true EEE framework — everything is tax free. NPS follows an EET framework — the investment and accumulation are tax free, but the exit is partially taxable through the mandatory 40% annuity whose income is taxed at your retirement slab rate. However, NPS compensates for this with the exclusive 80CCD(1B) entry deduction that PPF cannot match.

NPS vs PPF Lock-in and Withdrawal Rules Compared

Liquidity is another important dimension of the NPS vs PPF in India 2026 comparison. Neither is a liquid instrument, but PPF gives slightly more flexibility:

PPF Withdrawal Rules

- Lock-in: 15 years from account opening date

- Partial withdrawal: Allowed from year 7 onwards — up to 50% of the balance at the end of year 4 or the preceding year, whichever is lower

- Loan: Available from year 3 to year 6 — up to 25% of the balance at the end of year 2 or preceding year

- Premature closure: Allowed after 5 years for specific reasons — medical treatment, higher education, change of residency

- Extension: Account can be extended in 5-year blocks indefinitely after the initial 15-year tenure with or without contributions

NPS Tier 1 Withdrawal Rules

- Lock-in: Until age 60 (or 3 years for partial withdrawals after that)

- Partial withdrawal: Allowed after 3 years of account opening — up to 25% of own contributions for specific purposes (child education, marriage, home purchase, medical treatment)

- Exit before 60: If corpus is below ₹5 lakh, 100% can be withdrawn — 80% must be converted to annuity if above ₹5 lakh

- Exit at 60: Up to 60% can be withdrawn as tax-free lump sum — at least 40% must be used to purchase an annuity

- Annuity: The 40% mandatory annuity generates monthly pension income for life — taxable at your income slab rate in retirement

NPS vs PPF in India 2026 — Who Should Choose Which?

The NPS vs PPF in India 2026 question does not have one universal answer — it depends on your specific situation. Here is a clear decision framework:

| Your Profile | Recommended Choice | Reason |

|---|---|---|

| 80C limit not yet maxed out | PPF first | Fill PPF up to ₹1.5 lakh first before considering NPS for 80C benefit |

| 80C limit already maxed, in 20% or 30% tax slab | NPS under 80CCD(1B) | Extra ₹50,000 deduction saves ₹10,400 to ₹15,600 per year |

| Risk-averse, wants guaranteed returns | PPF | Zero market risk, government-guaranteed returns, EEE tax treatment |

| Age 25 to 40, long retirement horizon | Both — PPF plus NPS equity-heavy | Long horizon absorbs NPS market volatility, equity allocation builds larger corpus |

| Needs liquidity before retirement | PPF preferred | PPF allows partial withdrawals from year 7, NPS locks until 60 |

| Self-employed or freelancer | PPF plus NPS | No EPF, so both PPF and NPS help build retirement corpus from scratch |

| Government employee with existing pension | PPF for additional savings | Already enrolled in government NPS (mandatory), PPF adds tax-free savings layer |

| Wants tax-free complete lump sum at maturity | PPF | 100% tax-free maturity vs NPS where 40% must be annuitised |

Can You Invest in Both NPS and PPF at the Same Time?

Yes — and for most working professionals in the 20% or 30% tax slab with a long career ahead, investing in both NPS and PPF simultaneously is the recommended approach in the NPS vs PPF in India 2026 context. Here is a simple framework:

- Invest up to ₹1.5 lakh per year in PPF for guaranteed, completely tax-free long-term savings under the 80C umbrella

- Invest an additional ₹50,000 per year in NPS Tier 1 under 80CCD(1B) for the exclusive extra deduction that PPF cannot provide

- Within your NPS allocation, choose a 75% equity (Asset Class E) and 25% government securities (Asset Class G) allocation if you are below age 50, for maximum long-term growth

This combined approach gives you the best of both — the guaranteed, completely tax-free safety of PPF for your core long-term savings, plus the higher growth potential and exclusive additional tax deduction of NPS. Over a 25-year career, this combination can build a significantly larger retirement corpus than either instrument alone.

For a detailed breakdown of how PPF compares against FDs and mutual funds across all parameters, read our complete article on PPF vs FD vs mutual fund in India 2026. And for the full picture of all government savings scheme options including PPF, SSY, SCSS, and NSC, our guide on the best government savings schemes in India 2026 covers every option with current rates.

How to Open an NPS Account in India in 2026

Opening an NPS Tier 1 account in 2026 is fully digital and takes under 30 minutes:

- Visit eNPS portal: Go to enps.nsdl.com or eNPS on the NSDL website

- Choose registration type: Select Aadhaar OTP-based registration for the fastest process

- Enter personal details: PAN, Aadhaar, bank account, and nominee details

- Choose pension fund manager: Select from SBI, HDFC, ICICI, UTI, Kotak, or Birla Sun Life Pension Fund

- Choose asset allocation: Active choice (you decide the equity-debt-government split) or Auto choice (age-based automatic allocation)

- Make first contribution: Minimum ₹500 for Tier 1 account activation

- Get PRAN: Your Permanent Retirement Account Number is generated immediately after successful registration

You can also open NPS through your bank’s internet banking portal if your bank is an authorised Point of Presence (POP) — HDFC, ICICI, SBI, Axis, and Kotak all support NPS account opening through their respective net banking portals.

NPS vs PPF — The Role of Employer Contribution in NPS

One often-overlooked advantage of NPS in the NPS vs PPF in India 2026 comparison is the employer contribution benefit under Section 80CCD(2). If your employer contributes to your NPS account, that employer contribution is deductible from your taxable income under Section 80CCD(2) — up to 10% of basic salary for private sector employees and 14% for government employees. Crucially, this employer contribution benefit is available even under the New Tax Regime.

This means if you are a private sector employee and your employer contributes 10% of your basic salary to NPS — say ₹5,000 per month on a ₹50,000 basic — that ₹60,000 annual employer contribution reduces your taxable income by ₹60,000 per year with zero additional investment from you. This is free money that PPF cannot replicate. Ask your HR team whether your company offers NPS as part of your CTC structure.

To understand how to correctly declare both PPF and NPS deductions when filing your income tax return, read our step-by-step guide on how to file ITR online in India 2026 and our comprehensive article on how to save tax under Section 80C in India 2026 for the full deduction picture.

Conclusion — NPS vs PPF in India 2026 Is Not Either-Or

The NPS vs PPF in India 2026 question has a clear answer for most working Indians: do not choose one over the other — use both for different purposes. PPF for the guaranteed, completely tax-free EEE savings foundation at ₹1.5 lakh per year. NPS for the exclusive additional ₹50,000 deduction under 80CCD(1B) that PPF cannot provide, plus higher long-term growth potential from equity exposure.

If you have not maxed your 80C limit yet, start with PPF. Once your 80C is fully utilised through EPF, ELSS, and PPF, add NPS Tier 1 contributions for the exclusive 80CCD(1B) benefit. And if your employer offers NPS as part of your CTC, ensure you are enrolled — the employer contribution under 80CCD(2) is one of the best tax-free benefits available in India in 2026 regardless of which tax regime you choose.

At Smashora, our mission is to help every Indian make every rupee count. If this guide on NPS vs PPF in India 2026 helped you understand which option fits your financial situation, leave a comment below or share it with a colleague who is still confused about where to invest their tax-saving money this year.

Frequently Asked Questions

Which is better — NPS or PPF in India in 2026?

NPS and PPF serve different purposes and the better choice depends on your situation. If your 80C limit is not fully utilised, PPF is better as a first priority — it gives guaranteed, completely tax-free (EEE) returns at 7.1% per year with no market risk. Once your 80C limit is fully used through EPF, ELSS, and PPF, NPS is better for the additional ₹50,000 tax deduction under 80CCD(1B) that PPF cannot provide. For most salaried professionals in the 20% to 30% tax bracket, investing in both simultaneously is the optimal approach.

What is the Section 80CCD(1B) benefit of NPS?

Section 80CCD(1B) allows you to claim an additional tax deduction of up to ₹50,000 per year for contributions to NPS Tier 1 — completely separate from and above the ₹1.5 lakh Section 80C ceiling. This means a taxpayer who has already maxed out 80C at ₹1.5 lakh can claim a further ₹50,000 deduction by investing in NPS Tier 1, for a total of ₹2 lakh in deductions from these two sections combined. At the 30% tax slab, this saves an additional ₹15,600 per year in taxes that PPF alone cannot provide. This benefit is available only under the Old Tax Regime.

Can I withdraw from NPS before retirement?

Yes, with restrictions. After completing 3 years in NPS Tier 1, you can make partial withdrawals of up to 25% of your own contributions for specific purposes — child education, marriage, home purchase, or treatment of specified critical illnesses. You can make a maximum of 3 partial withdrawals during the entire tenure. For premature exit before age 60 where the corpus exceeds ₹5 lakh, at least 80% must be used to buy an annuity and only 20% can be taken as a lump sum. If the corpus is below ₹5 lakh at exit, 100% can be withdrawn.

What happens to NPS at retirement (age 60)?

At age 60, you can withdraw up to 60% of your NPS Tier 1 corpus as a completely tax-free lump sum. The remaining 40% must be mandatorily used to purchase an annuity from a PFRDA-approved insurance company, which generates a regular monthly pension income for life. This annuity income is taxable at your applicable income slab rate in retirement. You can defer the withdrawal and continue contributing to NPS up to age 75 if you choose not to exit at 60.

Is NPS available under the New Tax Regime in 2026?

Partially. Under the New Tax Regime in 2026, the popular 80C deduction (including PPF contributions) and the 80CCD(1B) extra ₹50,000 NPS deduction are not available. However, one NPS benefit survives under the New Tax Regime: Section 80CCD(2) — the employer contribution to your NPS account — is deductible up to 10% of basic salary for private sector employees and 14% for government employees. If your employer contributes to your NPS as part of your CTC, this benefit is available regardless of whether you choose Old or New Tax Regime. For all other NPS and PPF deductions, the Old Tax Regime is required.

How do I open an NPS account online in India in 2026?

Visit the eNPS portal at enps.nsdl.com and complete the fully digital registration using your Aadhaar OTP for identity verification. You will need your PAN card, Aadhaar linked to an active mobile number, bank account details, and a nominee’s details. Choose your pension fund manager and asset allocation during registration. Make an initial contribution of at least ₹500 to activate your Tier 1 account. Your PRAN (Permanent Retirement Account Number) is generated immediately. The process takes under 30 minutes. You can also open NPS through the net banking portals of HDFC, ICICI, SBI, Axis, and Kotak banks if you hold accounts there.