Contents

- 1 Why Most Indians Struggle to Save Money Every Month in 2026

- 2 The 50-30-20 Rule — The Best Framework for How to Save Money Every Month in India 2026

- 3 How to Save Money Every Month in India 2026 — Salary-Wise Examples

- 4 The Indian Reality — When 50-30-20 Does Not Work Perfectly

- 5 The Single Most Powerful Habit for Saving Money Every Month in India 2026

- 6 Where to Put Your Savings — The Right Instruments for Each Goal

- 7 20 Practical Tips to Save More Money Every Month in India in 2026

- 7.1 1. Track Expenses for 30 Days First

- 7.2 2. Audit and Cut Subscriptions Quarterly

- 7.3 3. Set a Weekly Food Delivery Budget

- 7.4 4. Use the 24-Hour Rule for Non-Essential Purchases

- 7.5 5. Switch to a Zero Balance High-Interest Savings Account

- 7.6 6. Increase SIP Amount Every April

- 7.7 7. Pack Lunch 3 Days Per Week

- 7.8 8. Never Pay Full Price for Electronics or Appliances

- 7.9 9. Refinance High-Interest Loans

- 7.10 10. Use UPI Cashback Cards Instead of Debit Cards

- 8 Common Money-Saving Mistakes Indians Make in 2026

- 9 Conclusion — The System Is More Important Than the Willpower

- 10 Frequently Asked Questions

- 10.1 How much of my salary should I save every month in India in 2026?

- 10.2 How to save money every month in India 2026 when rent takes most of my salary?

- 10.3 What is the 50-30-20 rule and does it work for Indians?

- 10.4 What is the best way to automatically save money every month in India?

- 10.5 How to save money fast in India 2026 when starting from zero?

- 10.6 Should I pay off debt first or save money every month in India?

Learning how to save money every month in India 2026 is one of the most searched and least acted-upon personal finance topics. The Reserve Bank of India‘s Annual Report for 2024-25 puts India’s net household financial savings rate at just 5.1% — one of the lowest in recent history. At the same time, consumer spending on food delivery, streaming subscriptions, EMIs, and lifestyle purchases has never been higher. Most Indians know they should save more. Very few have a system that makes it happen automatically every month without willpower or spreadsheet complexity.

I have had this conversation with dozens of people who earn good salaries and still find themselves with nothing left by the 28th of every month. A friend earning ₹85,000 per month in Bengaluru had exactly ₹3,200 in his savings account after four years of working. His money went to rent, Swiggy, Netflix, Amazon, weekend outings, and random impulse purchases — none of it tracked, none of it controlled. The problem was not the salary — it was the complete absence of a system. Once he adopted a simple 50-30-20 framework and automated his savings on salary day, he had ₹2.1 lakh saved within 12 months without feeling any significant lifestyle sacrifice.

This complete guide on how to save money every month in India 2026 gives you that system. It covers the 50-30-20 rule adapted for Indian realities, practical salary-wise budget examples, the specific habits that make saving automatic, and where to put the money you save so it actually grows. Follow this framework and saving money every month in India 2026 will stop being a resolution and start being a habit.

Why Most Indians Struggle to Save Money Every Month in 2026

Before looking at how to save money every month in India 2026, understanding the specific reasons Indians struggle is important because the solutions are different from generic global financial advice:

- No mandatory savings system for many earners: Salaried employees at companies above 20 employees have EPF deducted automatically — a forced savings habit. But contractual workers, freelancers, gig workers, and small business employees often have no automatic savings mechanism at all.

- Rising fixed costs consuming salary growth: Rent in metro cities has grown faster than salaries for most income brackets. A 2BHK in Bengaluru that cost ₹20,000 per month in 2018 now costs ₹35,000 to ₹45,000 in many areas — consuming a growing share of the monthly take-home for the same lifestyle.

- Lifestyle inflation matching income growth: When salary increases, spending typically increases by the same or more — phone upgrade, better restaurant, streaming service addition, premium gym. Savings rate stays flat even as absolute income grows.

- No system — only intention: Most Indians plan to save “whatever is left at the end of the month.” There is almost never anything left at the end of the month. The only system that works for how to save money every month in India 2026 is saving first, spending second — not the other way around.

- Family financial obligations: Sending money to parents, funding siblings’ education, contributing to family expenses — all legitimate and culturally important but must be explicitly budgeted rather than treated as irregular variable expenses.

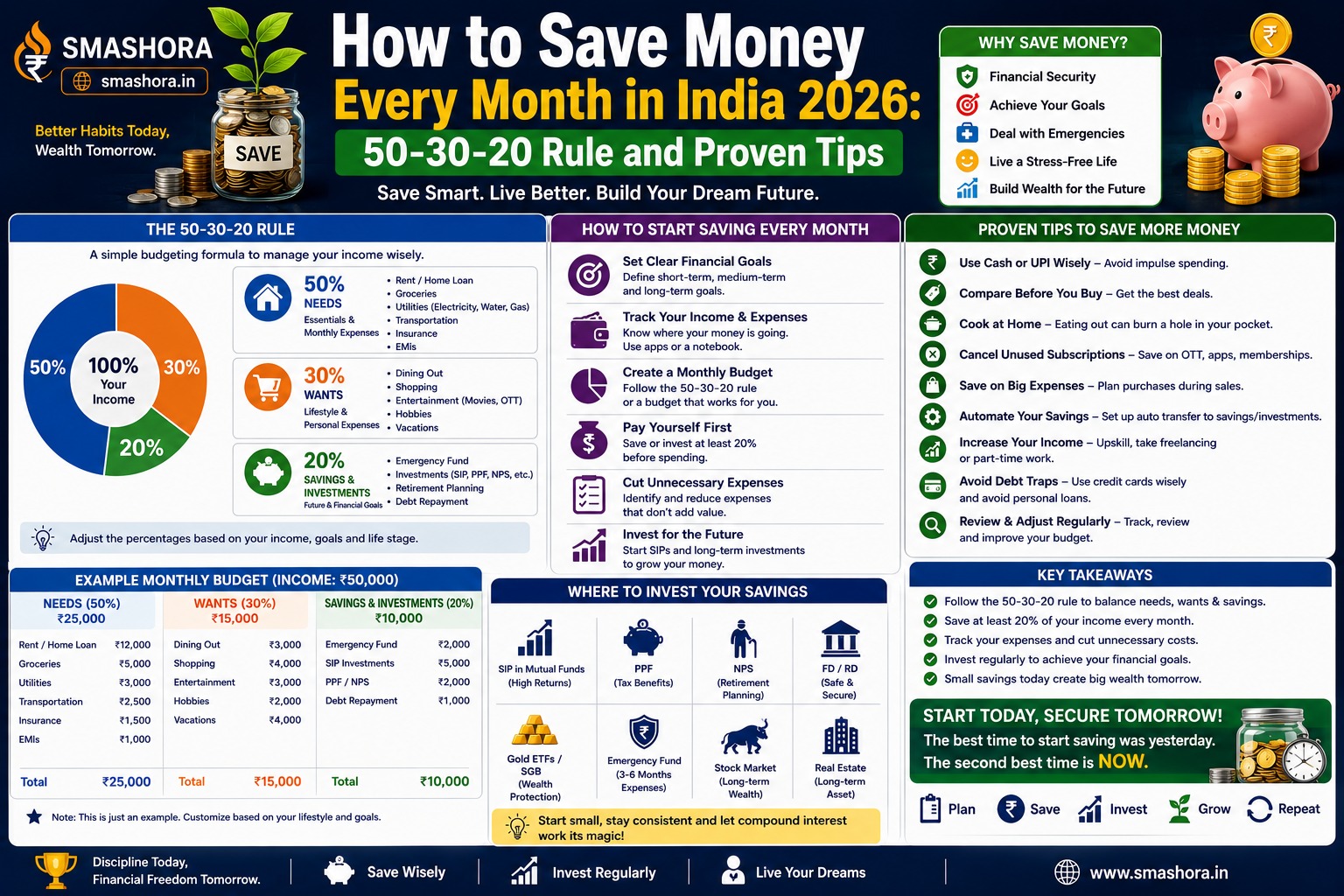

The 50-30-20 Rule — The Best Framework for How to Save Money Every Month in India 2026

The 50-30-20 rule is the most practical and widely proven budgeting framework for how to save money every month in India 2026. It divides your monthly take-home salary (not gross CTC — the actual amount credited to your bank account) into three buckets:

- 50% for Needs: All essential, non-negotiable monthly expenses

- 30% for Wants: Lifestyle and discretionary spending

- 20% for Savings and Investments: Money that builds your future wealth

The power of the 50-30-20 rule for how to save money every month in India 2026 is its simplicity. You do not track every single expense. You just ensure your three buckets stay roughly in proportion — and automate the savings bucket so it moves out on salary day before you have a chance to spend it.

What Goes in Each Bucket for Indians in 2026

| Bucket | Percentage | What to Include |

|---|---|---|

| Needs (50%) | 50% of take-home | Rent or home loan EMI, groceries, utility bills (electricity, water, gas), transport or petrol, health insurance premium, children’s school fees, mobile recharge, domestic help salary, family support sent home, any other non-negotiable monthly obligation |

| Wants (30%) | 30% of take-home | Dining out and food delivery (Swiggy, Zomato), streaming subscriptions (Netflix, Hotstar, Spotify), gym or fitness membership, shopping (clothing, gadgets, home decor), weekend outings and entertainment, personal care and grooming, vacations and travel |

| Savings and Investments (20%) | 20% of take-home | SIP in mutual funds, PPF contribution, additional EPF VPF (Voluntary Provident Fund), Recurring Deposit, FD, NPS contribution, any other long-term investment or savings goal |

How to Save Money Every Month in India 2026 — Salary-Wise Examples

Here is how the 50-30-20 rule for saving money every month in India 2026 looks across different salary levels:

Example 1 — ₹35,000 Take-Home Per Month (Early Career, Tier-2 City)

| Bucket | Amount | What It Covers |

|---|---|---|

| Needs (50%) | ₹17,500 | Rent ₹8,000, groceries ₹4,000, transport ₹2,500, mobile ₹500, insurance ₹800, miscellaneous ₹1,700 |

| Wants (30%) | ₹10,500 | Dining out ₹3,500, subscriptions ₹1,500, shopping ₹3,000, entertainment ₹2,500 |

| Savings (20%) | ₹7,000 | SIP ₹4,000, PPF ₹2,000, emergency fund ₹1,000 |

Example 2 — ₹60,000 Take-Home Per Month (Mid-Career, Metro City)

| Bucket | Amount | What It Covers |

|---|---|---|

| Needs (50%) | ₹30,000 | Rent ₹18,000, groceries ₹6,000, transport ₹3,000, mobile and internet ₹1,000, insurance ₹2,000 |

| Wants (30%) | ₹18,000 | Dining out ₹6,000, subscriptions ₹2,000, shopping ₹5,000, gym ₹2,000, entertainment ₹3,000 |

| Savings (20%) | ₹12,000 | SIP ₹7,000, PPF ₹3,000, emergency fund top-up ₹2,000 |

Example 3 — ₹1,00,000 Take-Home Per Month (Senior Professional, Metro City)

| Bucket | Amount | What It Covers |

|---|---|---|

| Needs (50%) | ₹50,000 | Home loan EMI ₹28,000, groceries ₹8,000, transport ₹5,000, insurance ₹4,000, domestic help ₹3,000, utilities ₹2,000 |

| Wants (30%) | ₹30,000 | Dining and food delivery ₹10,000, travel and weekend ₹8,000, shopping ₹7,000, subscriptions ₹3,000, gym and wellness ₹2,000 |

| Savings (20%) | ₹20,000 | SIP ₹12,000, PPF ₹4,000, NPS ₹3,000, FD or liquid fund ₹1,000 |

The Indian Reality — When 50-30-20 Does Not Work Perfectly

For many Indians learning how to save money every month in India 2026, the pure 50-30-20 split does not fit their situation cleanly — particularly in expensive metro cities where rent alone can consume 40% to 50% of take-home salary. Here is how to adapt:

When Rent Eats More Than 30% of Take-Home

If your rent is above 30% of take-home (common in Mumbai and Delhi for lower income brackets), start with a modified 60-20-20 rule: 60% for needs, 20% for wants, 20% for savings. The savings percentage stays protected even when needs are higher. Over time, work toward reducing needs below 60% through a longer commute for lower rent, a roommate arrangement, or a salary increase — but never sacrifice the savings bucket to fund lifestyle spending.

When Family Support Is a Large Obligation

For Indians sending ₹5,000 to ₹20,000 per month to parents or family, count this as part of your Needs bucket — it is not optional. Adjust the remaining Needs categories to fit within what is left. Family support is a real financial obligation that deserves honest budgeting, not classification as a Wants expense that gets cut when money is tight.

When EMIs Are High

If home loan EMI, car loan, and personal loan EMIs together exceed 30% to 35% of your take-home, your budget is in a danger zone. Never allow total EMI obligations to exceed 50% of take-home. If they do, the priority should be paying off the personal loan first (highest interest), reducing the car loan, and then aggressively prepaying the home loan over time as income grows.

The Single Most Powerful Habit for Saving Money Every Month in India 2026

Among all the tactics for how to save money every month in India 2026, one action has more impact than everything else combined: automate your savings transfer on salary day before you spend anything.

Set up an automatic transfer from your salary account to a separate savings or investment account on the 2nd or 3rd of every month — one or two days after your salary is credited. Transfer exactly 20% (or your chosen savings percentage) automatically. Treat this transfer like an EMI that cannot be missed. What remains in your salary account is all you have to spend for the month — and your spending naturally adjusts to what is available.

This pay-yourself-first approach is the most psychologically effective saving habit because it removes the need for willpower at the end of the month. You do not have to resist spending because the money is already moved to a separate account before the temptation arises.

Where to Put Your Savings — The Right Instruments for Each Goal

Knowing how to save money every month in India 2026 includes knowing where to put what you save so it earns the best possible return:

| Savings Purpose | Best Instrument | Why |

|---|---|---|

| Emergency Fund (3 to 6 months expenses) | High-interest savings account or liquid mutual fund | Instant access, earns 4% to 7.5% — better than regular savings account |

| Short-term goal (1 to 3 years) | Bank FD or debt mutual fund | Guaranteed returns, safe capital, no market risk |

| Tax saving (80C) | PPF or ELSS SIP | PPF for guaranteed tax-free returns, ELSS for higher returns with 3-year lock-in |

| Long-term wealth building (7 years plus) | Equity mutual fund SIP (Nifty 50 index fund) | Highest historical returns among all asset classes in India |

| Retirement corpus | NPS, PPF, and equity SIP combined | Mix of government-backed safety and equity growth |

| Child education fund | ELSS SIP or Sukanya Samriddhi Yojana (for daughters) | Long horizon for compounding, SSY at 8.2% tax-free for girl child |

For guidance on building an emergency fund first before moving money into investments, read our complete guide on how to build an emergency fund in India. For growing your savings in the right mutual fund SIP, our guide on the best SIP to start in India 2026 covers every category and fund recommendation. For the best FD options for safe short-term savings, read our article on the best FD rates in India 2026.

20 Practical Tips to Save More Money Every Month in India in 2026

1. Track Expenses for 30 Days First

Before building any budget, track where every rupee actually goes for one full month. Use an app like Walnut, Fi Money, or a simple Google Sheets template. Most Indians are surprised by how much they spend on food delivery, subscriptions, and small impulse purchases that individually feel trivial but collectively add up to ₹5,000 to ₹15,000 per month.

2. Audit and Cut Subscriptions Quarterly

List every recurring subscription charged to your credit card or bank account — Netflix, Hotstar, Spotify, Amazon Prime, news apps, gym, meditation apps, cloud storage. Cancel everything you have not actively used in the past 30 days. Most people have 4 to 8 active subscriptions they have forgotten about or no longer use, totalling ₹1,500 to ₹4,000 per month in silent drains.

3. Set a Weekly Food Delivery Budget

Food delivery is the single biggest discretionary expense category for working Indians in metro and tier-1 cities. Set a fixed weekly Swiggy or Zomato budget — say ₹800 per week — and stick to it. Cooking even 3 to 4 meals at home per week instead of ordering saves ₹2,000 to ₹5,000 per month for most people without meaningful lifestyle sacrifice.

4. Use the 24-Hour Rule for Non-Essential Purchases

For any non-essential purchase above ₹1,000 — clothing, gadget, home item, app subscription — wait 24 hours before buying. If you still want it the next day and it fits your Wants budget, buy it without guilt. If the urge passes, you have saved that money automatically. This single rule eliminates the majority of impulse purchases that derail monthly savings for most Indians.

5. Switch to a Zero Balance High-Interest Savings Account

Move your emergency fund and short-term savings to a small finance bank savings account earning 6% to 7.5% per year instead of leaving it at SBI or HDFC earning 2.7% to 3.5%. The extra 3% to 4% on even ₹2 lakh adds ₹6,000 to ₹8,000 per year in additional interest — essentially free money for switching banks.

6. Increase SIP Amount Every April

Every April when your salary increment comes in, increase your monthly SIP by at least 50% of the increment amount. If your take-home increases by ₹5,000, increase your SIP by ₹2,500. This step-up SIP approach ensures your investment rate grows with your income while still allowing lifestyle improvement from the remaining increment.

7. Pack Lunch 3 Days Per Week

Office canteen or restaurant lunch costs ₹150 to ₹350 per meal. Packing lunch from home 3 days per week saves ₹1,200 to ₹2,800 per month — approximately ₹14,000 to ₹33,000 per year. It is also healthier. This is genuinely one of the highest-return money-saving habits available to working Indians.

8. Never Pay Full Price for Electronics or Appliances

Amazon and Flipkart run sales events 6 to 8 times per year — Big Billion Days, Great Indian Sale, Republic Day, Independence Day sales. Buying electronics during these sales gives 10% to 40% off. Set a wish list, wait for a sale, buy then. Never pay full price for any planned electronics purchase.

9. Refinance High-Interest Loans

If you are paying above 12% per year on a personal loan or above 9.5% on a home loan, check whether you can transfer the balance to a lower-rate lender. Reducing your personal loan rate from 16% to 11% on a ₹3 lakh outstanding balance saves approximately ₹15,000 in total interest — money that goes directly to savings instead of interest payments.

10. Use UPI Cashback Cards Instead of Debit Cards

Replace your regular debit card with a RuPay credit card that earns cashback on UPI transactions. Cards like Kiwi RuPay or Axis Bank RuPay Credit Card earn 1% to 2% cashback on every UPI payment — including kirana stores, autos, and street vendors. On ₹25,000 in monthly UPI spends, that is ₹3,000 to ₹6,000 per year back in your pocket for zero additional effort.

Common Money-Saving Mistakes Indians Make in 2026

Saving What Is Left Instead of Spending What Remains

The most common savings failure in India is the “save whatever is left” approach. There is almost never anything left. Always save first — transfer your savings amount on salary day before spending. This single reversal transforms saving from an intention to a result.

Treating Savings as Emergency Backup for Wants

Savings accounts that are easily accessible become spending accounts within 3 to 4 months for most people. Keep your emergency fund and long-term investments in separate accounts that require deliberate action to access. The friction of having to log into a separate app or call a bank creates a natural pause that prevents impulsive savings withdrawal for non-emergencies.

Focusing on Cutting Expenses Instead of Increasing Income

There is a mathematical limit to how much you can cut expenses — but there is no limit to how much you can earn. Once basic discretionary waste is eliminated, the more powerful lever for how to save money every month in India 2026 is increasing income through skill development, career growth, freelancing, or a side project. An extra ₹10,000 per month from a side skill grows your savings rate far more than finding the next ₹500 cut in expenses.

Ignoring Small Regular Purchases

A ₹200 Swiggy delivery three times per week is ₹2,400 per month — ₹28,800 per year. A ₹1,500 streaming service you watch occasionally is ₹18,000 per year. Small recurring purchases are invisible individually but devastating collectively to your monthly savings goal. The only way to see them is to track them for one full month before budgeting.

Understanding how to save money every month in India 2026 also means understanding where to invest what you save for maximum growth. Our comprehensive guide on PPF vs FD vs mutual fund in India 2026 gives you the complete comparison of every safe and growth investment option available to Indian investors.

Conclusion — The System Is More Important Than the Willpower

The secret to how to save money every month in India 2026 is not discipline or motivation — it is a system that removes the need for both. Adopt the 50-30-20 framework, automate your savings transfer on salary day, track your expenses for one month to identify your biggest drains, and increase your savings rate by at least 1% to 2% every year. Done consistently over 10 to 20 years, these habits build wealth that changes your life.

Start today with one action — set up an automatic transfer of 20% of your next salary to a separate savings or investment account on the day it is credited. That one action, repeated every month, is the foundation of how to save money every month in India 2026 and every year after.

At Smashora, our mission is to help every Indian make every rupee count. If this guide on how to save money every month in India 2026 helped you think about your finances differently, leave a comment below and share which tip you are starting with today — or share it with a friend or family member whose salary seems to disappear every month.

Frequently Asked Questions

How much of my salary should I save every month in India in 2026?

Financial experts generally recommend saving at least 20% of your take-home salary every month as a baseline for building meaningful long-term wealth. The 50-30-20 rule — 50% for needs, 30% for wants, 20% for savings — is the most practical framework. If 20% feels too high to start, begin with 10% and increase by 1% every 3 months. The habit of saving consistently matters more than the exact percentage when you are starting out. As your income grows, aim to increase your savings rate toward 25% to 30% for faster wealth building.

How to save money every month in India 2026 when rent takes most of my salary?

High rent is the most common challenge for how to save money every month in India 2026, especially in metro cities. The practical solutions are: consider a roommate to split rent (saves ₹8,000 to ₹15,000 per month in most metros), move to a locality with a longer commute but significantly lower rent, or adopt a modified budget rule like 60-20-20 (60% needs, 20% wants, 20% savings) that acknowledges the higher fixed cost reality. The critical rule is never let your savings percentage drop below 10% even in expensive months — protect the savings bucket before adjusting anywhere else.

What is the 50-30-20 rule and does it work for Indians?

The 50-30-20 rule divides your monthly take-home salary into three buckets: 50% for essential needs (rent, groceries, EMIs, insurance), 30% for lifestyle wants (dining out, shopping, entertainment), and 20% for savings and investments. It works well for most Indians as a starting framework but needs adaptation for high-rent metro cities, large family obligations, or heavy EMI burdens. Many Indians find a modified 60-20-20 (higher needs, lower wants) or even 70-20-10 more realistic initially. The key principle — save at least 20% before spending on wants — is more important than the exact split between the other two buckets.

What is the best way to automatically save money every month in India?

The most effective automatic saving method for how to save money every month in India 2026 is setting up a monthly SIP in a mutual fund on the 1st or 2nd of the month — immediately after your salary is credited. The SIP debit happens automatically, and the remaining money in your account is what you spend for the month. Other automatic saving methods include standing instructions to transfer to a recurring deposit, EPF voluntary provident fund contributions through your employer, and sweep-in FD facilities that automatically convert idle savings account balances into higher-interest FDs.

How to save money fast in India 2026 when starting from zero?

To save money fast in India 2026 when starting from nothing: first audit all subscriptions and cancel unused ones (saves ₹1,000 to ₹4,000 immediately), reduce food delivery to twice per week (saves ₹2,000 to ₹5,000 per month), apply the 24-hour rule on all non-essential purchases above ₹1,000, move idle savings to a high-interest savings account at a small finance bank earning 6% to 7.5%, and start even a ₹500 per month SIP. These five steps together typically free up ₹5,000 to ₹10,000 per month for most Indians within 30 days without major lifestyle changes.

Should I pay off debt first or save money every month in India?

The right priority order for how to save money every month in India 2026 when you have debt is: first, build a 1-month emergency buffer (₹20,000 to ₹50,000 depending on expenses) to prevent taking on new debt for emergencies; second, pay off all high-interest debt above 15% per year (credit card outstanding, personal loans) aggressively; third, ensure your EPF and any employer-matched savings are active; fourth, start a small SIP even while paying off debt; and fifth, once high-interest debt is cleared, redirect that EMI amount entirely into savings and investments. Never stop all savings entirely to pay off debt unless the interest rate is above 18% to 20% and the outstanding is manageable in under 12 months.