Contents

- 1 Current FD Rate Landscape in India in 2026 — What Changed

- 2 Best FD Rates in India 2026 — Public Sector Banks

- 3 Best FD Rates in India 2026 — Private Sector Banks

- 4 Best FD Rates in India 2026 — Small Finance Banks (Highest Rates)

- 5 Best FD Rates in India 2026 — NBFCs

- 6 Special FD Schemes Worth Knowing in 2026

- 7 Tax-Saving FD — Best FD for Section 80C Benefit in 2026

- 8 Senior Citizen FD Rates in India 2026 — Best Options

- 9 FD vs Savings Account — Where Should Your Money Sit?

- 10 How FD Interest Is Taxed in India 2026

- 11 Effective Post-Tax Returns on FDs Across Tax Slabs

- 12 Smart Strategies to Maximise Your FD Returns in 2026

- 13 Conclusion — Find the Best FD Rates in India 2026 Before You Book

- 14 Frequently Asked Questions

- 14.1 Which bank offers the best FD rate in India in 2026?

- 14.2 Are small finance bank FDs safe in India in 2026?

- 14.3 What is TDS on FD and how can I avoid it in 2026?

- 14.4 Should I invest in FD or PPF in 2026?

- 14.5 What is FD laddering and how does it work in India?

- 14.6 Can NRIs invest in FDs in India in 2026?

Finding the best FD rates in India 2026 requires looking beyond the usual SBI and HDFC comparisons. The Reserve Bank of India’s multiple repo rate cuts in 2025 and 2026 have pushed large bank FD rates to 6.25% to 7.00% for most tenures — but small finance banks and NBFCs are still offering 7.50% to 9.10% per year on the same money, with the same DICGC insurance protection up to ₹5 lakh that your SBI account enjoys. That rate difference on ₹5 lakh over 3 years can add up to ₹30,000 to ₹70,000 in extra interest — simply by choosing the right institution.

I watched my parents renew a ₹10 lakh FD at SBI for 7.00% simply because it was convenient, at a time when AU Small Finance Bank was offering 8.00% for the same tenure. The difference over 3 years was over ₹30,000 in missed interest — more than enough to cover a year of health insurance premiums. That experience reinforced a simple principle: FD investing requires the same comparison discipline as buying any other financial product.

In 2026, with multiple banks cutting rates after RBI repo rate reductions, knowing the best FD rates in India 2026 across all bank categories — public sector, private sector, small finance banks, and NBFCs — is more important than ever for risk-averse investors, retirees, and anyone parking short to medium-term savings. This complete guide covers current rates from all major categories, the smartest tenures to lock in, special FD schemes worth knowing about, and exactly how to maximise your FD returns in the current interest rate environment.

Current FD Rate Landscape in India in 2026 — What Changed

Understanding the best FD rates in India 2026 requires understanding what has happened to rates over the past year. The RBI cut the repo rate multiple times in 2025, and banks have been gradually passing on these cuts through reduced FD rates on most standard tenures. This makes 2026 a very different FD environment from 2023 and 2024 when rates were at multi-year highs.

- Large public sector banks (SBI, PNB, Bank of Baroda): Standard 1-year FD rates have come down to 6.25% to 7.00% from the highs of 7.00% to 7.50% seen in 2023

- Large private banks (HDFC, ICICI, Axis, Kotak): 6.25% to 7.20% depending on tenure

- Small finance banks (Jana, Utkarsh, Suryoday, AU): Still holding rates at 7.25% to 8.25% — the most competitive options for the best FD rates in India 2026

- NBFCs (Bajaj Finance, Muthoot Capital): 7.00% to 9.10% — highest available rates but carry slightly higher credit risk than banks

Best FD Rates in India 2026 — Public Sector Banks

Public sector banks are the first choice for most conservative Indian investors due to the government ownership factor. Here are the current best FD rates in India 2026 from public sector banks:

| Bank | 1 Year FD Rate | 3 Year FD Rate | 5 Year FD Rate | Senior Citizen Extra |

|---|---|---|---|---|

| State Bank of India | 6.25% | 6.50% | 6.50% | 0.50% extra |

| Bank of Baroda | 6.85% | 7.00% | 6.50% | 0.50% extra |

| Punjab National Bank | 6.80% | 6.50% | 6.50% | 0.50% extra |

| Canara Bank | 6.85% | 6.70% | 6.70% | 0.50% extra |

| Union Bank of India | 6.50% | 6.50% | 6.50% | 0.50% extra |

| Bank of India | 6.80% | 6.50% | 6.25% | 0.50% extra |

Best FD Rates in India 2026 — Private Sector Banks

| Bank | 1 Year FD Rate | 3 Year FD Rate | 5 Year FD Rate | Senior Citizen Extra |

|---|---|---|---|---|

| Kotak Mahindra Bank | 7.10% | 7.00% | 6.20% | 0.50% extra |

| RBL Bank | 7.20% | 7.00% | 6.80% | 0.50% extra |

| ICICI Bank | 6.50% | 6.50% | 6.25% | 0.50% extra |

| HDFC Bank | 6.25% | 6.50% | 6.40% | 0.50% extra |

| Axis Bank | 6.70% | 7.00% | 6.75% | 0.50% extra |

| IndusInd Bank | 7.25% | 7.00% | 7.00% | 0.50% extra |

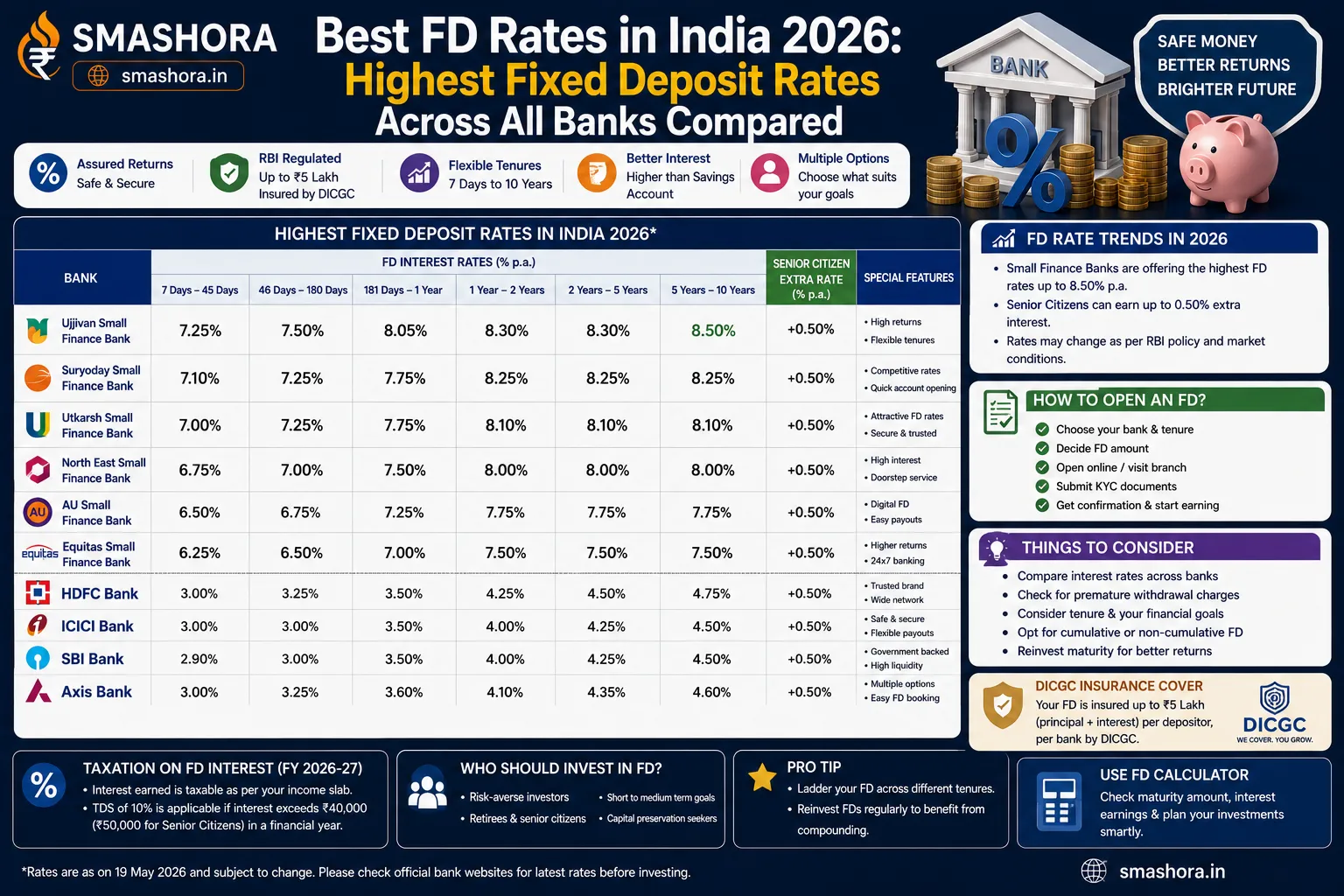

Best FD Rates in India 2026 — Small Finance Banks (Highest Rates)

Small finance banks offer the best FD rates in India 2026 among all bank categories — often 0.75% to 1.50% higher than equivalent large bank rates for the same tenure. All small finance banks are regulated by the RBI and deposits are DICGC insured up to ₹5 lakh per depositor per bank — the same protection as SBI or HDFC.

| Small Finance Bank | 1 Year FD Rate | 3 Year FD Rate | Senior Citizen Rate | Max Rate Available |

|---|---|---|---|---|

| Jana Small Finance Bank | 7.75% | 7.50% | 8.25% | 8.00% (general) |

| Utkarsh Small Finance Bank | 7.90% | 7.75% | 8.40% | 8.00% (general) |

| Suryoday Small Finance Bank | 8.25% | 8.25% | 8.75% | 8.25% (general) |

| AU Small Finance Bank | 7.25% | 7.50% | 7.75% | 7.50% (general) |

| ESAF Small Finance Bank | 7.50% | 7.50% | 8.00% | 7.75% (general) |

| Equitas Small Finance Bank | 7.25% | 7.25% | 7.75% | 7.50% (general) |

Best FD Rates in India 2026 — NBFCs

NBFCs (Non-Banking Financial Companies) offer the highest FD rates available in India 2026 — but they carry a higher risk profile than banks since NBFC deposits are not covered by DICGC insurance. Only invest in NBFC FDs from AAA-rated or AA-plus-rated companies and keep amounts within limits you can afford to have at risk.

| NBFC | General Citizen Rate | Senior Citizen Rate | Credit Rating | Max Tenure |

|---|---|---|---|---|

| Muthoot Capital | Up to 9.10% | Up to 9.35% | AA | 5 years |

| Bajaj Finance | Up to 8.35% | Up to 8.60% | AAA | 5 years |

| Shriram Finance | Up to 8.58% | Up to 8.83% | AA Plus | 5 years |

| Mahindra Finance | Up to 7.75% | Up to 8.00% | AAA | 5 years |

Important note on NBFC FDs: NBFC deposits are NOT covered by DICGC insurance. If an NBFC fails, your deposit is at risk. Only invest in AAA-rated NBFCs like Bajaj Finance and Mahindra Finance for maximum safety. Limit NBFC FD exposure to amounts you can manage even in a worst-case scenario.

Special FD Schemes Worth Knowing in 2026

Several banks offer special FD schemes at non-standard tenures (like 444 days or 555 days) with higher rates than their regular tenure rates. These are among the best FD rates in India 2026 for investors who want to lock in at peak rates before further cuts:

| Bank | Special Scheme | Tenure | Rate (General) | Rate (Senior) |

|---|---|---|---|---|

| SBI | Amrit Vrishti | 444 days | 7.05% | 7.55% |

| Bank of Baroda | Square Drive FD | 444 days | 7.00% | 7.50% |

| Bank of India | Harit Jama Yojana | Varied | Up to 7.30% | Up to 7.80% |

| IDBI Bank | Utsav FD | 375 days | 7.05% | 7.55% |

Special FD schemes are available for limited periods and the tenures are odd to prevent direct comparison with regular FDs. They typically offer 0.25% to 0.50% more than the bank’s standard 1-year FD rate. Always check if the scheme is still active on the bank’s website before going to book.

Tax-Saving FD — Best FD for Section 80C Benefit in 2026

A Tax-Saving Fixed Deposit is a special 5-year FD that qualifies for Section 80C deduction up to ₹1.5 lakh per year. It is one of the safest 80C investment options for conservative investors who do not want equity risk. Key things to know:

- Lock-in: 5 years — strictly no premature withdrawal allowed

- 80C benefit: Investment qualifies for deduction up to ₹1.5 lakh per year

- Interest: Fully taxable as income every year — TDS deducted at source if annual interest exceeds ₹40,000

- Current rates at major banks: 6.40% to 7.00% per year

- Joint holding: 80C benefit available only to the first account holder

| Bank | Tax Saving FD Rate (General) | Tax Saving FD Rate (Senior) |

|---|---|---|

| SBI 5-year Tax Saving FD | 6.50% | 7.00% |

| HDFC Bank 5-year Tax Saving FD | 6.40% | 6.90% |

| ICICI Bank 5-year Tax Saving FD | 6.25% | 6.75% |

| Axis Bank 5-year Tax Saving FD | 7.00% | 7.50% |

| IndusInd Bank 5-year Tax Saving FD | 7.00% | 7.50% |

For investors in the 30% tax bracket, the effective post-tax return on a 7% tax-saving FD is approximately 4.9% — significantly lower than PPF at a completely tax-free 7.1%. If you are choosing between a Tax Saving FD and PPF for your 80C investment, PPF almost always wins for higher tax bracket investors. Read our detailed comparison of PPF vs FD vs mutual fund in India 2026 to understand exactly how the numbers work.

Senior Citizen FD Rates in India 2026 — Best Options

Senior citizens (above 60 years) get an extra 0.25% to 0.50% on FD rates at most banks — making fixed deposits one of the most attractive safe income options for retirees. Here are the best FD rates in India 2026 specifically for senior citizens:

| Institution | Best Senior Citizen FD Rate | Tenure | Type |

|---|---|---|---|

| Suryoday Small Finance Bank | 8.75% | 5 years | Small Finance Bank |

| Utkarsh Small Finance Bank | 8.40% | 2 to 3 years | Small Finance Bank |

| Jana Small Finance Bank | 8.25% | 2 to 3 years | Small Finance Bank |

| Bajaj Finance | 8.60% | 44 months | NBFC (AAA rated) |

| Shriram Finance | 8.83% | 2 to 3 years | NBFC (AA Plus rated) |

| SBI (We-Care scheme) | 7.55% (super senior 80 plus) | 5 years | Public Sector Bank |

| Senior Citizen Savings Scheme | 8.2% (quarterly payout) | 5 years | Government scheme |

For senior citizens specifically, the Senior Citizen Savings Scheme (SCSS) at 8.2% with government backing and quarterly income payouts remains the strongest safe option — covered in full detail in our guide on the best government savings schemes in India 2026.

FD vs Savings Account — Where Should Your Money Sit?

Many Indians keep large amounts in savings accounts earning 3% to 4% when the best FD rates in India 2026 are offering 7% to 8.25%. Here is a simple rule of thumb:

- Keep in savings account: Your emergency fund (1 to 2 months expenses) for instant access, and your monthly operating expenses buffer

- Put in FD: Any money you will not need for 6 months or longer. Even a 6-month FD earning 6.5% is significantly better than a savings account at 3.5%

- Use sweep-in FD: For money in between — amounts you may need but not immediately. Sweep-in FDs earn FD rates automatically on idle savings account balances

For a complete guide on which savings account to use for different purposes, read our detailed article on the best zero balance savings account in India 2026.

How FD Interest Is Taxed in India 2026

One of the most overlooked aspects of finding the best FD rates in India 2026 is the tax impact. FD interest is fully taxable as income every year — regardless of whether you withdraw it or let it compound. Here is what you need to know:

| Annual FD Interest Earned | TDS Rate | When TDS Is Deducted |

|---|---|---|

| Below ₹40,000 (₹50,000 for seniors) | No TDS | No deduction |

| Above ₹40,000 (₹50,000 for seniors) | 10% TDS | Deducted at source by bank |

| If PAN not submitted to bank | 20% TDS | Always submit your PAN to avoid this |

TDS is only a withholding tax — not your final tax liability. If your total income falls below the basic exemption limit, you can claim a full refund of TDS by submitting Form 15G (non-senior citizens) or Form 15H (senior citizens) to your bank at the beginning of every financial year. This prevents TDS from being deducted altogether. For a step-by-step guide on declaring FD interest correctly in your ITR and claiming TDS refunds, read our article on how to file ITR online in India 2026.

Effective Post-Tax Returns on FDs Across Tax Slabs

| Gross FD Rate | Nil Tax Slab | 5% Slab | 20% Slab | 30% Slab |

|---|---|---|---|---|

| 6.50% | 6.50% | 6.17% | 5.20% | 4.55% |

| 7.00% | 7.00% | 6.65% | 5.60% | 4.90% |

| 7.50% | 7.50% | 7.12% | 6.00% | 5.25% |

| 8.00% | 8.00% | 7.60% | 6.40% | 5.60% |

| 8.25% | 8.25% | 7.84% | 6.60% | 5.78% |

For investors in the 30% tax bracket, even the best FD rates in India 2026 at 8.25% deliver only 5.78% effective post-tax returns — barely ahead of the 7.1% tax-free PPF rate. This is why for higher tax bracket investors, PPF and government savings schemes are often more attractive than FDs on an after-tax basis despite their lower stated rates.

Smart Strategies to Maximise Your FD Returns in 2026

FD Laddering

Instead of putting all your FD money in one tenure, split it across multiple tenures — for example, three separate FDs maturing in 1 year, 2 years, and 3 years respectively. This FD ladder gives you liquidity at regular intervals while capturing higher rates on the longer tenures. When each FD matures, reinvest it at the then-current rate. This strategy protects you from being fully locked in if rates rise, while still capturing current high rates on part of your corpus.

Use Small Finance Banks for Higher Rates

As shown in the tables above, small finance banks like Suryoday, Jana, and Utkarsh consistently offer 1% to 2% higher rates than large public sector banks for the same tenure. Deposits up to ₹5 lakh are equally safe due to DICGC insurance. Spreading your FD corpus across 2 to 3 small finance banks — staying within the ₹5 lakh insurance limit at each — lets you earn significantly higher returns without taking on meaningful additional risk.

Submit Form 15G or 15H to Avoid Unnecessary TDS

If your total annual income is below the taxable threshold, submit Form 15G (for non-seniors under 60) or Form 15H (for senior citizens) to your bank at the start of every financial year. This prevents the bank from deducting TDS on your FD interest and saves you the hassle of claiming a refund in your ITR.

Choose Cumulative FDs for Long-Term Goals

A cumulative FD reinvests the interest and pays everything at maturity — giving you the full benefit of compound interest. A non-cumulative FD pays out interest monthly or quarterly. For long-term savings goals like building a corpus for a down payment or retirement supplement, always choose cumulative FDs for maximum compounding.

Conclusion — Find the Best FD Rates in India 2026 Before You Book

The best FD rates in India 2026 are not at the banks most people automatically go to. Suryoday Small Finance Bank at 8.25% for general citizens, Jana and Utkarsh at 7.75% to 7.90%, and Bajaj Finance at 8.35% offer the highest rates — all significantly above SBI at 6.25% or HDFC at 6.25%. For senior citizens, rates go up to 8.75% at small finance banks and 8.83% at Shriram Finance.

The key decision framework for the best FD rates in India 2026 is: choose large banks for amounts above ₹5 lakh where safety matters most, and use small finance banks for up to ₹5 lakh per bank where DICGC insurance gives you equivalent protection at significantly higher rates. Ladder your FDs across tenures, submit Form 15G or 15H if your income is below the taxable threshold, and always calculate post-tax returns before comparing with PPF or debt mutual funds.

At Smashora, our mission is to help every Indian make every rupee count. If this guide on the best FD rates in India 2026 helped you find a better rate for your next FD booking, leave a comment below or share it with a family member who is about to renew their FD at the same old rate out of habit.

Frequently Asked Questions

Which bank offers the best FD rate in India in 2026?

Among banks, Suryoday Small Finance Bank offers the highest FD rate in India 2026 at up to 8.25% per year for general citizens and 8.75% for senior citizens. Among private sector banks, IndusInd Bank and RBL Bank offer competitive rates of 7.20% to 7.25% for general investors. Among public sector banks, Bank of Baroda leads with up to 7.00% for standard tenures. For NBFCs, Muthoot Capital offers the highest rate at up to 9.10% for general citizens but without DICGC insurance coverage. For most investors, small finance bank FDs up to the ₹5 lakh DICGC insurance limit offer the best risk-adjusted rates available in India in 2026.

Are small finance bank FDs safe in India in 2026?

Yes. All small finance banks in India are regulated by the RBI and deposits up to ₹5 lakh per depositor per bank are fully insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC) — the same protection that applies to SBI and HDFC Bank deposits. The term “small finance bank” refers to the licence category under RBI regulation, not the financial size or safety of the institution. Banks like AU Small Finance Bank, Equitas, Jana, and Utkarsh are well-capitalised regulated entities. To stay within the insurance coverage limit, keep no more than ₹5 lakh including principal and accrued interest at any single small finance bank.

What is TDS on FD and how can I avoid it in 2026?

TDS (Tax Deducted at Source) on FD interest is deducted at 10% by the bank when your total annual FD interest exceeds ₹40,000 (₹50,000 for senior citizens). If your total annual income including FD interest is below the basic exemption limit (₹2.5 lakh for general taxpayers, ₹3 lakh for senior citizens under New Regime), you can avoid TDS entirely by submitting Form 15G (non-senior citizens) or Form 15H (senior citizens) to your bank at the beginning of every financial year. This declaration tells the bank your income is below the taxable threshold and they will not deduct TDS on your interest payments.

Should I invest in FD or PPF in 2026?

For investors in the 20% or 30% income tax slab, PPF at 7.1% completely tax-free is almost always better than an FD at 6.50% to 7.00% with fully taxable returns. After tax, a 7% FD earns only 5.60% for 20% slab investors and 4.90% for 30% slab investors — both below PPF’s tax-free 7.1%. PPF also compounds over 15 years with EEE treatment. For investors in the nil or 5% tax slab, a high-rate small finance bank FD at 7.50% to 8.25% can beat PPF on net returns. For a complete detailed comparison including mutual funds, read our article on PPF vs FD vs mutual fund in India 2026.

What is FD laddering and how does it work in India?

FD laddering is a strategy where instead of placing all your money in a single FD, you split it across multiple FDs with different maturity dates — for example ₹1 lakh each maturing in 1 year, 2 years, and 3 years. When each FD matures, you reinvest it for the longest tenure in your ladder. This gives you regular liquidity access without breaking any FD prematurely, captures higher rates on longer tenures, and protects you from being entirely locked in if interest rates rise. FD laddering is particularly useful for investors who need periodic access to funds but want to earn higher than savings account rates on their idle money.

Can NRIs invest in FDs in India in 2026?

Yes. NRIs can invest in FDs in India through NRE (Non-Resident External) or NRO (Non-Resident Ordinary) accounts. NRE FD interest is completely exempt from Indian income tax and the principal and interest are freely repatriable. NRO FD interest is taxable in India and TDS is deducted at 30% for NRIs. Most major banks in India offer NRE and NRO FD facilities. NRE FD rates are typically slightly lower than regular domestic FD rates at the same bank, and NRIs should check the latest rates directly on the bank’s NRI banking portal before booking.