Contents

- 1 What Is Gratuity and Who Must Pay It

- 2 Gratuity Eligibility Rules in India 2026

- 3 The Correct Gratuity Calculation Formula in India 2026

- 4 Gratuity Calculation — Worked Examples

- 5 New Labour Code Changes Affecting Gratuity Rules in India 2026

- 6 Gratuity Tax Rules in India 2026 — Section 10(10)

- 7 Gratuity When You Change Jobs — What Actually Happens

- 8 What Gratuity Does NOT Cover

- 9 Can Your Employer Forfeit Your Gratuity?

- 10 The 30-Day Payment Rule

- 11 For Employees in Establishments with Fewer Than 10 Workers

- 12 How to Verify Your Gratuity Calculation Is Correct

- 13 Conclusion — Know the Formula, Know Your Rights

- 14 Frequently Asked Questions

- 14.1 What is the correct gratuity calculation formula in India in 2026?

- 14.2 How many years of service are required for gratuity in India in 2026?

- 14.3 What is the maximum gratuity amount and tax exemption in India in 2026?

- 14.4 What does the new Labour Code change about gratuity in 2026?

- 14.5 Can my employer deduct gratuity from my Full and Final Settlement?

- 14.6 What happens to gratuity when an employee changes jobs?

Every salaried Indian employed in a company with 10 or more employees is entitled to gratuity — a statutory lump-sum payment from the employer recognising long service — yet most employees have only a vague idea of exactly how much they are owed or when they become eligible. Understanding gratuity rules and calculations in India 2026 has become particularly important following the Code on Social Security, 2020, notified on November 21, 2025, which introduced meaningful changes including eligibility for fixed-term employees after just one year of service and a tighter wage definition that can significantly increase gratuity payouts for employees with heavily structured CTC packages.

The difference between using the correct formula and a common shortcut calculation is real money. On a basic salary of ₹60,000 per month with 10 years of service, the correct formula — using 26 as the divisor — gives ₹3,46,154. Using 30 as the divisor, which many employees mistakenly use, gives only ₹3,00,000. That is a difference of ₹46,154 in gratuity the employee is legally entitled to. Knowing the formula correctly means knowing what you should receive when the time comes, and being able to identify immediately if your employer’s Full and Final Settlement is understating your rightful amount.

This complete guide on gratuity rules and calculation in India 2026 covers the eligibility criteria, the correct formula with worked examples, the new Labour Code changes, the ₹20 lakh tax exemption, what happens when you change jobs, and exactly what you should do if you believe you are being underpaid.

What Is Gratuity and Who Must Pay It

Gratuity is a statutory, one-time lump-sum payment that an employer is legally obligated to make to an employee upon the end of their employment, in recognition of continuous, long-term service. It is governed primarily by the Payment of Gratuity Act, 1972, which applies to every establishment employing 10 or more persons on any day in the preceding 12 months — including factories, mines, oilfields, plantations, ports, railway companies, shops, and any other establishment covered under the Act.

An important point many employers miss: once an establishment meets the 10-employee threshold, the Act applies permanently, even if the employee count later drops below 10. This means a company that grew to 12 employees in one year and later reduced to 7 is still fully covered under the Act and must pay gratuity to eligible departing employees. For the official text of the Act and its amendments, refer to the Ministry of Labour and Employment website.

Gratuity Eligibility Rules in India 2026

| Situation | Minimum Service Required |

|---|---|

| Resignation or voluntary retirement | 5 years of continuous service |

| Superannuation (reaching retirement age) | 5 years of continuous service |

| Retrenchment or layoff by employer | 5 years of continuous service |

| Death of the employee | No minimum service — payable regardless |

| Permanent disablement due to accident or disease | No minimum service — payable regardless |

| Fixed-term contract employees (new rule, November 2025) | 1 year of continuous service |

The 4 Years and 240 Days Rule — An Important Nuance

Multiple High Courts have consistently held that an employee who has completed exactly 4 years and 240 or more working days in the fifth year should be treated as having completed 5 continuous years of service for the purposes of gratuity eligibility. This is an important protection for employees who resign just before the technical five-year anniversary. If your joining date and resignation date are within 4 years and some months, carefully count your actual working days in that fifth year before concluding you are ineligible.

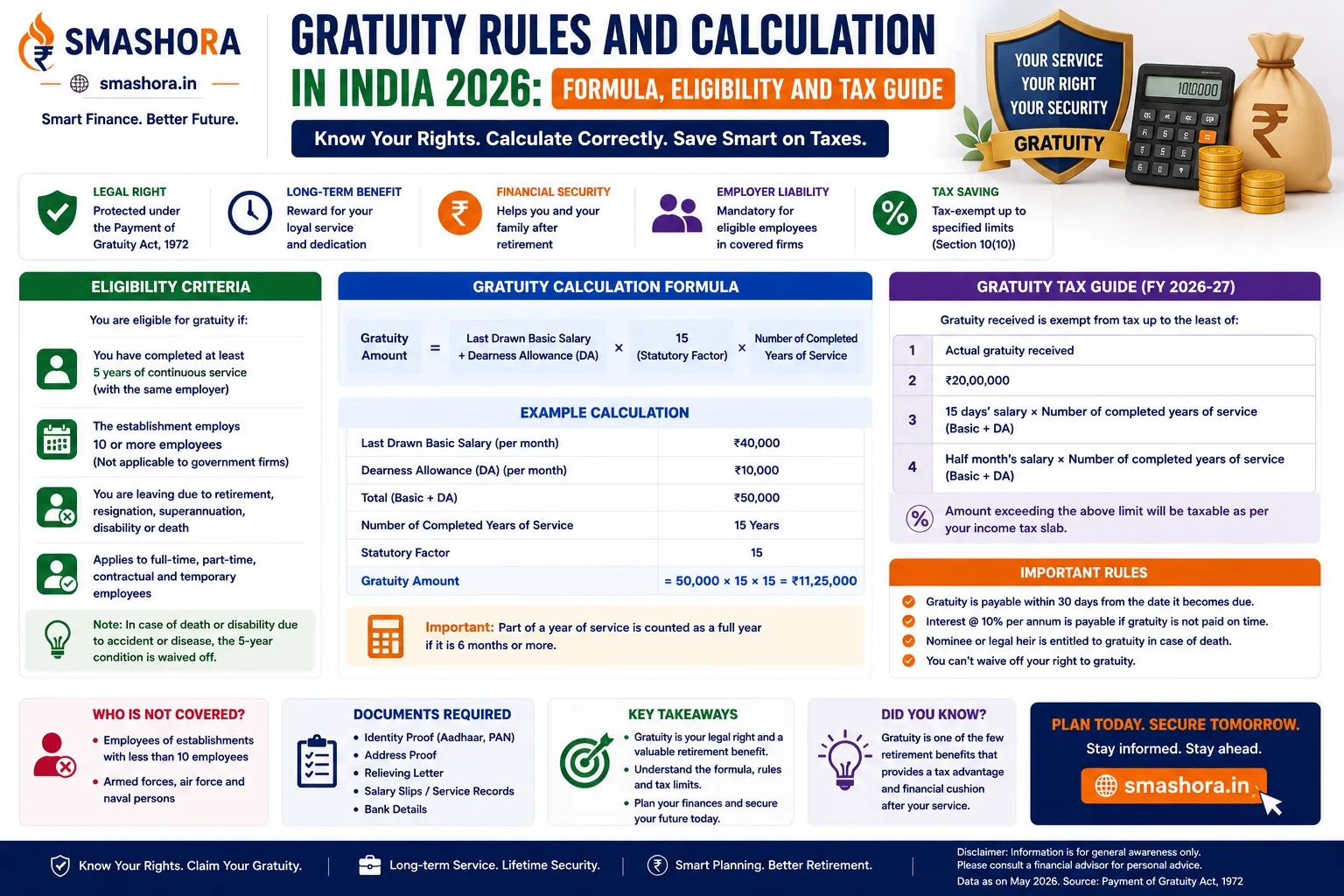

The Correct Gratuity Calculation Formula in India 2026

The formula for calculating gratuity under the Payment of Gratuity Act for employers covered by the Act is:

Gratuity = (Basic Salary + Dearness Allowance) × 15 × Completed Years of Service ÷ 26

The three most important things to understand about this formula:

- The divisor is 26, not 30: The 26 represents the average number of working days in a month under the Act, excluding Sundays and rest days. Using 30 systematically understates the gratuity by over 13%, since a higher daily wage value results when dividing the monthly salary by fewer working days. This single error costs many employees significant money in their Full and Final Settlement.

- Salary means Basic plus DA only: Gratuity is calculated on Basic Salary plus Dearness Allowance only — not on CTC, gross salary, HRA, performance bonus, commission, or any other allowances. In most private sector companies that pay zero DA, only the Basic figure from the last payslip is used.

- The 15 represents 15 days’ wages per year of service: The law awards half a month’s pay (15 out of 26 working days) for each completed year of long service.

How to Count Completed Years of Service

Completed years of service uses a rounding rule: if the service period includes more than 6 months beyond the last complete year, it rounds up to the next full year. If 6 months or fewer, it rounds down. For example, 9 years and 8 months counts as 10 years, while 9 years and 4 months counts as 9 years. This rounding difference can mean thousands of rupees in the final calculation — count your service period carefully from the exact joining date to the exact last working day.

Gratuity Calculation — Worked Examples

| Scenario | Basic + DA | Service Period | Counted Years | Calculated Gratuity |

|---|---|---|---|---|

| Mid-career professional | ₹45,000/month | 7 years 3 months | 7 years (3 months below 6) | ₹45,000 × 15 × 7 ÷ 26 = ₹1,82,692 |

| Senior professional | ₹60,000/month | 9 years 8 months | 10 years (8 months above 6) | ₹60,000 × 15 × 10 ÷ 26 = ₹3,46,154 |

| Long-serving employee | ₹1,20,000/month | 22 years | 22 years | ₹1,20,000 × 15 × 22 ÷ 26 = ₹15,23,077 |

| Very senior employee | ₹1,80,000/month | 22 years | 22 years | Formula gives ₹22,84,615 — but statutory and tax-exempt cap is ₹20 lakh |

The fourth example is important: when the formula produces a figure above ₹20 lakh, the statutory ceiling applies. The employer is legally required to pay only up to ₹20 lakh in gratuity. They may choose to pay the excess amount as an ex gratia discretionary payment, but any amount above ₹20 lakh becomes taxable in the employee’s hands regardless of its label.

New Labour Code Changes Affecting Gratuity Rules in India 2026

The Code on Social Security, 2020, was notified for commencement on November 21, 2025, introducing two changes that materially affect gratuity rules and calculation in India 2026. However, as of mid-2026, while the Code has been notified, the full implementation mechanism, including the commencement date for all establishments, remains subject to ongoing procedural notifications — the Payment of Gratuity Act, 1972 remains the operative law for existing covered establishments, with the Code’s provisions progressively applying:

Change 1 — Fixed-Term Employees: Gratuity After 1 Year

Under the Code on Social Security, fixed-term contract employees who have completed at least one year of continuous service with the same employer become eligible for proportionate gratuity — eliminating the 5-year service requirement that previously excluded most contract workers from this benefit. This is a significant expansion of gratuity coverage, particularly relevant in sectors like IT, media, hospitality, and healthcare where fixed-term contract employment is widespread.

Change 2 — 50% Wage Rule: Higher Gratuity for Many Employees

The new Code specifies that “wages” for the purpose of gratuity calculation must constitute at least 50% of an employee’s total remuneration or CTC. In practice, many employers structure CTC packages with a low basic salary and high allowances to minimise statutory deductions. The 50% wage rule means that if an employee’s basic salary is only 30% of their total CTC, allowances will be added back to meet the 50% threshold, which increases the gratuity calculation base and therefore the gratuity payout. This change benefits employees with heavily structured CTC packages and effectively penalises the practice of suppressing basic pay to reduce statutory liability.

Gratuity Tax Rules in India 2026 — Section 10(10)

Understanding the tax treatment is one of the most important aspects of gratuity rules and calculation in India 2026, since it determines your actual net take-home from this retirement benefit:

| Employee Category | Tax Exemption |

|---|---|

| Central and state government employees, defence personnel | Fully exempt — no upper limit under Section 10(10)(i) |

| Private sector employees covered under the Payment of Gratuity Act | Exempt up to ₹20 lakh (lifetime cumulative limit across all employers) under Section 10(10)(ii) |

| Private sector employees in establishments NOT covered under the Act | Exempt up to ₹20 lakh or as per Section 10(10)(iii) formula, whichever is lower |

| Any gratuity above the applicable exemption limit | Taxable as income from salary at the applicable income tax slab rate in the year of receipt |

The ₹20 Lakh Lifetime Cumulative Cap — A Critical Detail

The ₹20 lakh tax exemption ceiling is not per employer — it is a lifetime cumulative limit across your entire career. If you received ₹8 lakh in gratuity from a previous employer earlier in your career and claimed that as tax-exempt, only ₹12 lakh of gratuity from your next employer will be exempt, not another ₹20 lakh. Employees who have worked at multiple organisations over a long career should track their cumulative gratuity exemption claimed to avoid surprises in their Full and Final settlement tax calculation. For a complete guide on how to declare gratuity received correctly when filing your annual tax return, read our step-by-step article on how to file ITR online in India 2026.

Gratuity When You Change Jobs — What Actually Happens

Unlike EPF, gratuity is not transferable between employers and cannot be carried forward to accumulate with a new employer. When you resign from one company, you either receive your gratuity immediately (if you have completed the service requirement) or you do not receive any gratuity for that tenure. Each employer calculates and pays gratuity independently for the service period with that specific employer. This means if you changed jobs after 4 years and 11 months at a company, you receive zero gratuity for that tenure despite nearly meeting the requirement — there is no partial carry-forward mechanism for gratuity the way EPF account balance transfers work.

This is one of the structural reasons why long service with a single employer builds significantly more retirement wealth from gratuity than the same total years spent across multiple short stints, even if total working years are identical. Our comprehensive guide on retirement planning in India 2026 covers how to factor gratuity alongside EPF, NPS, and PPF into a complete retirement wealth strategy.

What Gratuity Does NOT Cover

- Performance bonuses and variable pay: Not included in the gratuity calculation base — only Basic and DA count

- HRA, conveyance, and other allowances: All excluded from the calculation base

- Commission-based earnings: Excluded unless specifically defined as wages under the relevant provisions

Can Your Employer Forfeit Your Gratuity?

Gratuity forfeiture is permitted only in two specific, legally defined situations under Section 4(6) of the Payment of Gratuity Act:

- Willful omission or negligence causing damage to employer property: Only partial forfeiture to the extent of the actual damage caused, not a blanket forfeiture

- Offence involving moral turpitude committed during service: Full forfeiture permitted only in this narrow category

Gratuity cannot be forfeited for poor performance, routine absenteeism, leaving without serving a notice period, or any general misconduct that does not meet the legal threshold above. Many employees are incorrectly told their gratuity is being withheld due to notice period non-compliance or performance issues — this is not legally enforceable and can be challenged under the Act.

The 30-Day Payment Rule

Under Section 7(3) of the Payment of Gratuity Act, the employer must pay gratuity within 30 days of it becoming due — meaning within 30 days of the employee’s last working day after the notice period ends. Delay attracts simple interest at a rate specified by the government for the period of delay, and willful non-payment can result in prosecution under Section 9, which carries fines up to ₹1 lakh and imprisonment up to 2 years for serious violations. If your employer is delaying your gratuity beyond 30 days without a valid legal reason, you can file a complaint with the Controlling Authority (typically the Labour Commissioner) under the Act.

For Employees in Establishments with Fewer Than 10 Workers

The Payment of Gratuity Act does not technically apply to establishments with fewer than 10 employees. However, such employers may choose to voluntarily pay gratuity, and many do so as a goodwill gesture. Where they do, the tax exemption for the employee follows Section 10(10)(iii) — exempt up to the least of the actual gratuity received, ₹20 lakh, or the amount calculated using a slightly different formula (half-month’s average salary from the last 10 months × completed years of service ÷ 30).

How to Verify Your Gratuity Calculation Is Correct

- Check your last drawn basic salary: Pull your most recent payslip and identify the Basic Salary line — only this figure (plus DA if any) goes into the formula

- Count your service years carefully: Calculate from your exact joining date to your exact last working day, applying the 6-month rounding rule

- Apply the formula: Basic × 15 × rounded years ÷ 26

- Cross-check with the ₹20 lakh statutory cap: If your formula result exceeds ₹20 lakh, the statutory payout is capped at ₹20 lakh

- Compare against your Full and Final Settlement: If your employer’s stated gratuity is lower than your calculated figure, flag the discrepancy in writing before signing the full and final release document

It is also worth ensuring your broader financial foundation is solid before your gratuity is received, so that this lump sum can be deployed effectively rather than absorbed by unplanned expenses. Our guide on how to build an emergency fund in India covers the right structure, and our article on how to save income tax on salary in India 2026 covers other retirement-related tax benefits available alongside gratuity.

Conclusion — Know the Formula, Know Your Rights

The gratuity rules and calculation in India 2026 are based on a clear, well-established formula that every salaried employee deserves to understand before their employment ends. The key facts to carry: 5 years of continuous service for eligibility (or 4 years and 240 days under court precedent), the 15/26 formula using basic plus DA only, the ₹20 lakh statutory and tax-exempt ceiling, and the employer’s legally binding 30-day payment deadline after your last working day. The November 2025 Labour Code changes additionally extend these gratuity rules and calculation standards in India 2026 to fixed-term contract workers after just 1 year, and introduce the 50% wage rule that should increase gratuity payouts for employees with low basic-to-CTC ratios.

If your employer’s Full and Final Settlement includes a gratuity figure lower than what your own calculation produces, you have the right to raise a formal dispute with the Labour Commissioner. Gratuity is not a discretionary bonus — it is a statutory benefit, and the law is clearly on the employee’s side when the payment rules are followed correctly.

At Smashora, our mission is to help every Indian make every rupee count — including the rupees that are legally yours in your Full and Final Settlement. If this guide on gratuity rules and calculation in India 2026 helped you understand what you are owed, leave a comment below or share it with a colleague who is planning to resign or is negotiating their exit from a current role.

Frequently Asked Questions

What is the correct gratuity calculation formula in India in 2026?

The correct gratuity formula for employees in establishments covered by the Payment of Gratuity Act, 1972 is: Gratuity = (Basic Salary + Dearness Allowance) × 15 × Completed Years of Service ÷ 26. The critical points are to use 26 as the divisor (not 30, which understates the amount by over 13%), to include only Basic and DA in the salary figure (not CTC, gross salary, or any other allowances), and to apply the rounding rule of counting the service period as a complete additional year if the excess beyond the last full year is more than 6 months.

How many years of service are required for gratuity in India in 2026?

The standard eligibility requirement for gratuity in India in 2026 is 5 years of continuous service with the same employer, applicable upon resignation, retirement, or retrenchment. Courts have consistently held that 4 years and 240 working days in the fifth year satisfies this requirement. The 5-year rule is waived entirely in cases of death or permanent disablement, where gratuity is payable regardless of how many years the employee has served. Under the Code on Social Security, 2020, notified in November 2025, fixed-term contract employees become eligible for proportionate gratuity after just 1 year of service.

What is the maximum gratuity amount and tax exemption in India in 2026?

The statutory maximum gratuity payable under the Payment of Gratuity Act and the maximum tax-exempt limit for private sector employees are both ₹20 lakh. Any formula calculation that produces a figure above ₹20 lakh is capped at ₹20 lakh for the statutory payment — though employers may pay the excess voluntarily as an ex-gratia amount. For income tax purposes, the ₹20 lakh exemption is a lifetime cumulative limit across all employers throughout the employee’s career, not a per-employer limit. Government employees have full gratuity exemption with no monetary ceiling.

What does the new Labour Code change about gratuity in 2026?

The Code on Social Security, 2020, notified on November 21, 2025, introduced two key gratuity changes: First, fixed-term contract employees working under a contract of at least one year become eligible for proportionate gratuity after just one year of service, removing the 5-year requirement for this employment category. Second, the revised definition of “wages” specifies that wages must constitute at least 50% of an employee’s total remuneration for gratuity calculation purposes, which increases the gratuity base for employees whose employers had structured packages with abnormally low basic salaries to minimise statutory obligations. As of mid-2026, the Payment of Gratuity Act, 1972 remains the operative law for existing covered establishments, with the Code’s provisions applying progressively.

Can my employer deduct gratuity from my Full and Final Settlement?

No, except in two very narrow legally defined circumstances: partial forfeiture to the extent of actual damage if the employee willfully caused damage to employer property through omission or negligence, or full forfeiture if the employee was terminated for an offence involving moral turpitude committed during service. Gratuity cannot be forfeited for non-completion of a notice period, poor performance, general absenteeism, or most routine disciplinary matters. If your employer is withholding gratuity for any other reason, you can file a formal complaint with the Controlling Authority (typically the District Labour Commissioner) under Section 8 of the Payment of Gratuity Act.

What happens to gratuity when an employee changes jobs?

Gratuity is not transferable between employers. When you resign from one company after meeting the service requirement, you receive your gratuity directly from that employer as part of your Full and Final Settlement. The accumulated amount cannot be carried forward to a new employer. Each employer independently calculates and pays gratuity based only on the service period with that specific employer and the last drawn salary there. The ₹20 lakh tax exemption is a lifetime cumulative limit across all employers, so you should track the total gratuity exemption already claimed from previous employers when computing the taxable portion from a subsequent employer.