Contents

- 1 What is a Personal Loan and When Should You Take One?

- 2 Best Personal Loan in India 2026 — Current Interest Rates Comparison

- 3 Best Personal Loan in India 2026 — Top Lenders Reviewed

- 3.1 1. SBI Xpress Credit — Best for Government and PSU Employees

- 3.2 2. HDFC Bank Personal Loan — Best for Instant Disbursal

- 3.3 3. ICICI Bank Personal Loan — Best for High Loan Amounts

- 3.4 4. Bajaj Finserv Personal Loan — Best for Long Tenure and Flexibility

- 3.5 5. Axis Bank Personal Loan — Best for Salaried Professionals in Private Sector

- 4 Personal Loan EMI Table — Know Your Monthly Outgo

- 5 How Your CIBIL Score Affects Your Personal Loan Rate in 2026

- 6 Key Things to Check Before Taking the Best Personal Loan in India 2026

- 7 Personal Loan vs Credit Card EMI vs BNPL — Which Is Better in 2026?

- 8 How to Apply for the Best Personal Loan in India 2026 — Step by Step

- 9 How Your CIBIL Score Affects Your Personal Loan Rate in 2026

- 10 Key Things to Check Before Taking the Best Personal Loan in India 2026

- 11 Personal Loan vs Credit Card EMI vs BNPL — Which Is Better in 2026?

- 12 How to Apply for the Best Personal Loan in India 2026 — Step by Step

- 13 Conclusion — Compare Before You Borrow the Best Personal Loan in India 2026

- 14 Frequently Asked Questions

- 14.1 Which bank gives the best personal loan in India in 2026?

- 14.2 What CIBIL score do I need to get the best personal loan rate in India in 2026?

- 14.3 Can I get an instant personal loan in India in 2026?

- 14.4 What documents are needed for a personal loan in India in 2026?

- 14.5 What is the maximum personal loan amount I can get in India in 2026?

- 14.6 Should I take a personal loan or a credit card loan for a large expense in 2026?

Finding the best personal loan in India 2026 at the lowest possible interest rate is more important than most borrowers realise before they apply. Personal loan rates in India range from as low as 8.75% per year at public sector banks to as high as 24% to 36% per year from digital lenders and NBFCs — a gap that translates to tens of thousands of rupees in extra interest paid on the same loan amount. On a ₹5 lakh personal loan over 3 years, the difference between a 10% rate and a 20% rate is approximately ₹87,000 in total extra interest. That is not a small number for a loan meant to solve a short-term financial need.

Personal loans are the fastest-growing credit product in India in 2026 with over ₹2.73 lakh crore in personal loan applications processed in the past year alone. The sheer availability of instant personal loans from banks, NBFCs, and fintech apps has made borrowing easier than ever — but it has also made it easier to borrow at a poor rate without comparison shopping. I have seen colleagues take loans at 18% to 24% from fintech apps out of convenience when the same loan was available at 10% to 11% from their salary account bank with just a few extra steps.

This guide on the best personal loan in India 2026 covers the top lenders with current rates, exactly what determines the rate you are offered, how to calculate your EMI, and the smartest approach to getting the lowest possible rate on your personal loan application.

What is a Personal Loan and When Should You Take One?

A personal loan is an unsecured loan — meaning no collateral is required — given by banks and NBFCs based on your income, credit score, and employment profile. The money can be used for any purpose: medical emergency, home renovation, wedding expenses, education fees, travel, or debt consolidation.

Knowing when the best personal loan in India 2026 is the right tool is as important as knowing which lender to choose:

- Good reasons to take a personal loan: Medical emergency with no insurance cover, urgent home repair, one-time large expense you can repay within 1 to 3 years, consolidating multiple high-interest debts into one lower-rate loan

- Think twice before borrowing for: Discretionary spending like vacations or gadgets, funding regular monthly expenses (this signals a cash flow problem that a loan will worsen), investing in stocks or crypto (borrowing to invest is extremely high risk)

A personal loan at 12% to 15% for a genuine short-term need is a smart financial tool. A personal loan at 24% to fund lifestyle spending is an expensive debt trap. The best personal loan in India 2026 is one you genuinely need, at the lowest available rate, repaid as quickly as possible.

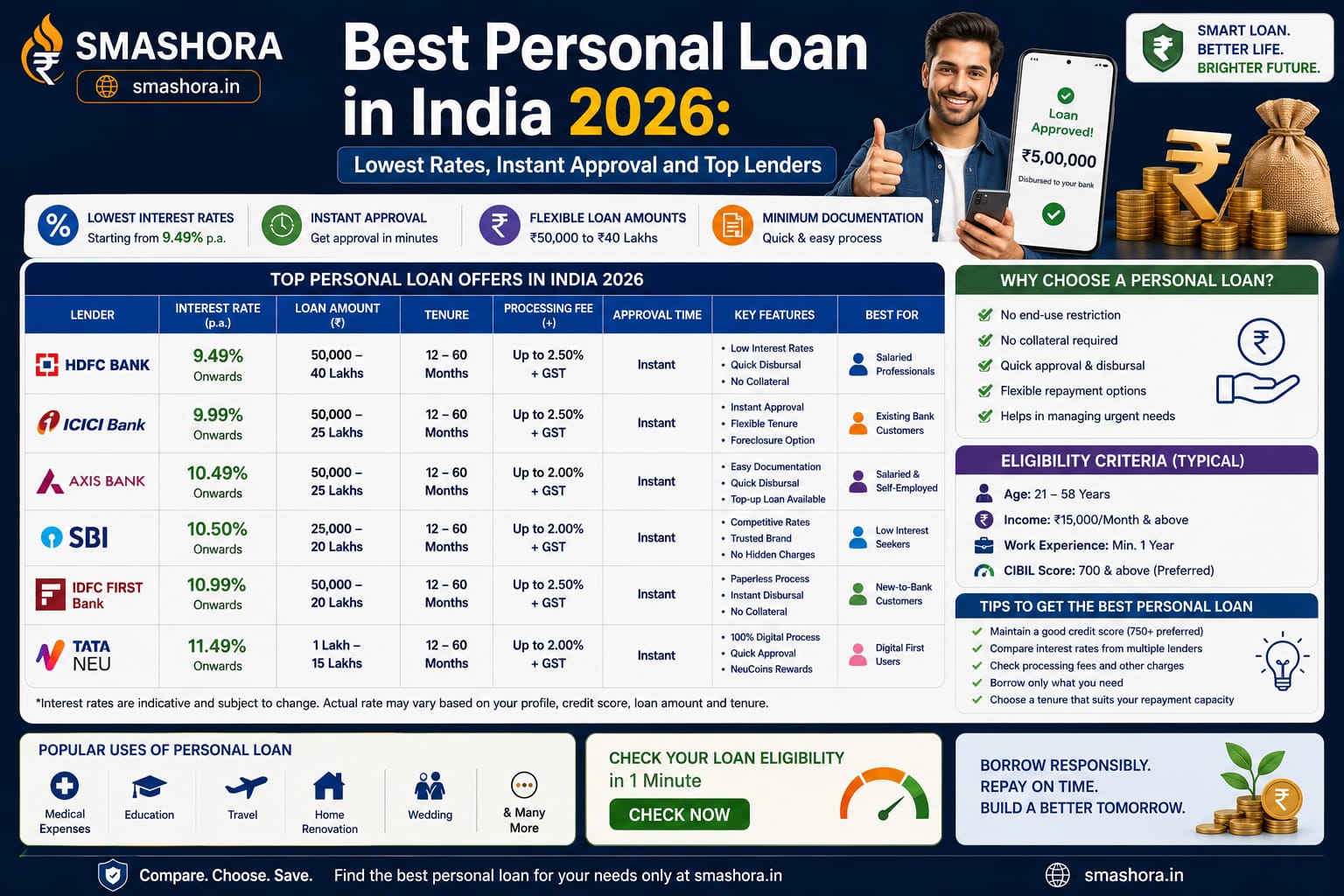

Best Personal Loan in India 2026 — Current Interest Rates Comparison

Here are the current personal loan rates from all major lenders as of June 2026:

| Lender | Interest Rate (per year) | Processing Fee | Max Loan Amount | Max Tenure |

|---|---|---|---|---|

| Union Bank of India | 8.75% to 13.15% | 0.50% | ₹15 lakh | 5 years |

| Bank of Maharashtra | 8.75% to 12.80% | 1.00% | ₹20 lakh | 5 years |

| SBI Xpress Credit | 9.60% to 15.65% | 1.50% (min ₹1,000) | ₹35 lakh | 6 years |

| HDFC Bank Personal Loan | 9.99% to 24.00% | Up to 2.50% | ₹40 lakh | 5 years |

| ICICI Bank Personal Loan | 10.50% to 19.00% | Up to 2.50% | ₹50 lakh | 6 years |

| Axis Bank Personal Loan | 10.49% to 22.00% | Up to 2.00% | ₹40 lakh | 5 years |

| Kotak Mahindra Bank | 10.99% to 24.00% | Up to 3.00% | ₹35 lakh | 5 years |

| Bajaj Finserv | 11.00% to 35.00% | Up to 3.93% | ₹40 lakh | 8 years |

| Tata Capital | 10.99% to 35.00% | Up to 3.00% | ₹35 lakh | 6 years |

| MoneyView | 15.96% to 39.99% | Up to 2.00% | ₹10 lakh | 5 years |

All rates above are indicative as of June 2026 for salaried borrowers. The actual rate you receive depends on your CIBIL score, income, employer profile, and existing banking relationship with the lender. For updated and official lending guidelines, you can refer to the Reserve Bank of India website.

Best Personal Loan in India 2026 — Top Lenders Reviewed

1. SBI Xpress Credit — Best for Government and PSU Employees

SBI Xpress Credit is consistently one of the best personal loan options in India 2026 for government employees, defence personnel, and PSU workers. SBI offers these borrowers significantly lower rates due to the job security their employment profile represents, and the loan process is simplified for salary account holders.

- Interest Rate: 9.60% to 15.65% per year

- Loan Amount: Up to ₹35 lakh

- Tenure: Up to 6 years

- Processing Fee: 1.50% (minimum ₹1,000)

- Special Rate: Government and PSU employees typically get 0.25% to 0.50% lower than private sector employees at the same credit score

- Key Feature: Pre-approved Xpress Credit loans for existing SBI salary account holders with instant disbursal via YONO app

Best for: Government employees, central or state government workers, defence personnel, and PSU employees who want the lowest possible rate from India’s most trusted public sector bank.

2. HDFC Bank Personal Loan — Best for Instant Disbursal

HDFC Bank is one of the top choices for the best personal loan in India 2026 for borrowers who need funds quickly. For pre-approved HDFC customers, loan disbursal happens within minutes directly into the bank account — no branch visit, no paperwork, no waiting period.

- Interest Rate: 9.99% to 24.00% per year

- Loan Amount: Up to ₹40 lakh

- Tenure: Up to 5 years

- Processing Fee: Up to 2.50%

- Key Feature: Instant pre-approved loan disbursal in under 10 seconds for eligible customers via HDFC mobile banking app

Best for: Existing HDFC Bank customers with a good credit profile who need funds urgently and want a fully digital process. HDFC’s pre-approved loan offers are usually at significantly better rates than their standard catalogue rates.

Honest consideration: HDFC’s processing fee of up to 2.50% is on the higher end. Always negotiate this down — HDFC is known to waive or reduce processing fees for high-value customers or during festive periods.

3. ICICI Bank Personal Loan — Best for High Loan Amounts

ICICI Bank offers one of the highest personal loan amounts in India — up to ₹50 lakh for well-qualified borrowers — making it the best personal loan in India 2026 for those who need a large amount for purposes like home renovation or wedding expenses. The fully digital process through iMobile Pay allows application to disbursal without any branch visit.

- Interest Rate: 10.50% to 19.00% per year

- Loan Amount: Up to ₹50 lakh

- Tenure: Up to 6 years

- Processing Fee: Up to 2.50% (minimum ₹999)

- Key Feature: Flexi loan option — borrow a credit line and pay interest only on the amount used, not the full sanctioned amount

Best for: Borrowers who need large personal loan amounts above ₹20 lakh, or those who want the flexibility of a credit line rather than a fixed loan with EMI from day one.

4. Bajaj Finserv Personal Loan — Best for Long Tenure and Flexibility

Bajaj Finserv is one of India’s largest NBFCs and a popular choice for the best personal loan in India 2026 due to its flexible repayment options, wide geographic reach, and high approval rates even for borrowers with slightly lower credit profiles. Its Flexi Hybrid loan option is one of the most unique personal loan products in India.

- Interest Rate: 11.00% to 35.00% per year

- Loan Amount: Up to ₹40 lakh

- Tenure: Up to 8 years (longest among major lenders)

- Processing Fee: Up to 3.93%

- Key Feature: Flexi Hybrid loan — pay only interest as EMI for the first part of the tenure, then switch to regular EMI — keeps initial monthly outflow low

Best for: Borrowers who need a longer repayment tenure to keep monthly EMIs manageable, or self-employed individuals who may not qualify easily at banks but have a reasonable credit history.

Honest consideration: Bajaj Finserv’s rates at the higher end go up to 35% per year. Always verify the exact rate being offered to you before signing — not the starting rate advertised. The processing fee is also among the highest. Negotiate both before accepting any offer.

5. Axis Bank Personal Loan — Best for Salaried Professionals in Private Sector

Axis Bank is a strong option for the best personal loan in India 2026 for salaried private sector professionals, with competitive starting rates and a fast digital process. Axis Bank customers with an existing relationship often receive pre-approved personal loan offers at rates well below the standard catalogue.

- Interest Rate: 10.49% to 22.00% per year

- Loan Amount: Up to ₹40 lakh

- Tenure: Up to 5 years

- Processing Fee: Up to 2.00%

- Key Feature: Same day disbursal for pre-approved customers, minimal documentation for salary account holders

Best for: Salaried professionals at reputable private sector companies with a clean credit history who bank with Axis and want competitive rates with quick processing.

Personal Loan EMI Table — Know Your Monthly Outgo

Before taking the best personal loan in India 2026, understanding your monthly EMI is critical. Here is a quick reference EMI table:

| Loan Amount | Rate 10% — 3 Years | Rate 12% — 3 Years | Rate 15% — 3 Years | Rate 18% — 3 Years |

|---|---|---|---|---|

| ₹1 lakh | ₹3,227 | ₹3,321 | ₹3,467 | ₹3,615 |

| ₹3 lakh | ₹9,681 | ₹9,963 | ₹10,401 | ₹10,845 |

| ₹5 lakh | ₹16,134 | ₹16,607 | ₹17,333 | ₹18,084 |

| ₹10 lakh | ₹32,267 | ₹33,214 | ₹34,665 | ₹36,152 |

| ₹20 lakh | ₹64,534 | ₹66,430 | ₹69,333 | ₹72,321 |

The difference in total interest between a 10% loan and an 18% loan on ₹5 lakh over 3 years is approximately ₹71,000. This is why spending an extra 30 minutes comparing the best personal loan options in India 2026 before applying is always worth it.

How Your CIBIL Score Affects Your Personal Loan Rate in 2026

Your CIBIL score is the single most important factor in determining what rate you get on the best personal loan in India 2026. Here is how score ranges map to typical rates:

| CIBIL Score | Typical Rate Range | Approval Likelihood |

|---|---|---|

| 800 and above | 9.99% to 11.00% | Very High — best rates available |

| 750 to 799 | 11.00% to 13.00% | High — competitive rates |

| 700 to 749 | 13.00% to 18.00% | Moderate — higher rates |

| 650 to 699 | 18.00% to 24.00% | Low — mostly NBFCs and digital lenders only |

| Below 650 | 24.00% to 36.00% or rejection | Very Low — consider improving score first |

If your CIBIL score is below 700 right now, you are better off spending 3 to 4 months improving it before applying for a personal loan. Even moving from 680 to 720 can reduce your personal loan rate by 4% to 6% — saving thousands in interest. Read our complete guide on how to improve your CIBIL score for step-by-step actions that work.

Key Things to Check Before Taking the Best Personal Loan in India 2026

Effective Annual Rate vs Stated Rate

The interest rate advertised by lenders is not always the true cost of your loan. Processing fees, GST on fees, insurance charges, and other upfront costs add to your effective borrowing cost. Always calculate the total amount you will repay — principal plus all charges — and divide by the loan amount and tenure to understand your true annualised cost before signing.

Prepayment and Foreclosure Charges

Unlike home loans, personal loans in India can have prepayment charges — typically 2% to 5% of the outstanding principal if you repay early. This matters because if you get a salary hike or a windfall and want to close the loan early, you may face a significant fee. Always check the prepayment terms before selecting a lender.

Part-Payment Facility

Some lenders allow part-payment — paying a lump sum toward the principal to reduce future EMIs or tenure — while others do not. If you expect to receive a bonus or tax refund during the loan period, choose a lender that allows part-payment without penalty.

Processing Fee Negotiation

Processing fees of 1% to 3% on a ₹5 lakh loan add up to ₹5,000 to ₹15,000 — often waivable or reducible through negotiation, especially if you are an existing customer or applying during a promotional period. Always ask for a processing fee waiver before accepting the loan offer.

Personal Loan vs Credit Card EMI vs BNPL — Which Is Better in 2026?

| Feature | Personal Loan | Credit Card EMI | Buy Now Pay Later |

|---|---|---|---|

| Interest Rate | 9.99% to 24% per year | 12% to 18% per year (0% for short tenures on offers) | 0% to 36% per year |

| Loan Amount | Up to ₹50 lakh | Up to your credit limit | Typically up to ₹1 to ₹2 lakh |

| Disbursal Time | Minutes to 2 days | Instant (on card swipe) | Instant at checkout |

| Tenure | 1 to 8 years | 3 to 24 months | 1 to 12 months typically |

| Impact on CIBIL | Hard inquiry on application | Reduces available credit limit | Varies by BNPL provider |

| Best For | Large amounts, multi-year repayment | Existing purchase on credit card, short tenure | Small purchases at 0% for 3 months |

For amounts above ₹2 lakh and tenures above 12 months, a personal loan from the best personal loan lender in India 2026 is almost always the most cost-effective option. For smaller purchases where your credit card offers 0% EMI, convert to credit card EMI instead. Read our guide on the best credit cards in India 2026 to find cards with the best 0% EMI offers and cashback on purchases.

How to Apply for the Best Personal Loan in India 2026 — Step by Step

- Check your CIBIL score: Know where you stand before applying. A score above 750 gets you the best rates. If below 700, delay and improve first.

- Calculate the exact amount you need: Borrow only what you need — not the maximum you qualify for. Every extra rupee borrowed costs you in interest.

- Compare at least 3 lenders: Use PaisaBazaar or BankBazaar to compare offers from multiple lenders without triggering multiple hard inquiries.

- Check your existing bank first: Your salary account bank almost always offers pre-approved loans at the best rates to existing customers. Check your banking app before going elsewhere.

- Negotiate processing fee: Always ask for a waiver or reduction before accepting any offer.

- Read the foreclosure terms: Confirm prepayment charges before signing — you may want to close the loan early if your finances improve.

- Apply and complete eKYC: Most lenders in 2026 offer fully digital applications with Aadhaar OTP-based eKYC and instant disbursal for eligible borrowers.

Before taking the best personal loan in India 2026, understanding your monthly EMI is critical. Here is a quick reference EMI table:

| Loan Amount | Rate 10% — 3 Years | Rate 12% — 3 Years | Rate 15% — 3 Years | Rate 18% — 3 Years |

|---|---|---|---|---|

| ₹1 lakh | ₹3,227 | ₹3,321 | ₹3,467 | ₹3,615 |

| ₹3 lakh | ₹9,681 | ₹9,963 | ₹10,401 | ₹10,845 |

| ₹5 lakh | ₹16,134 | ₹16,607 | ₹17,333 | ₹18,084 |

| ₹10 lakh | ₹32,267 | ₹33,214 | ₹34,665 | ₹36,152 |

| ₹20 lakh | ₹64,534 | ₹66,430 | ₹69,333 | ₹72,321 |

The difference in total interest between a 10% loan and an 18% loan on ₹5 lakh over 3 years is approximately ₹71,000. This is why spending an extra 30 minutes comparing the best personal loan options in India 2026 before applying is always worth it.

How Your CIBIL Score Affects Your Personal Loan Rate in 2026

Your CIBIL score is the single most important factor in determining what rate you get on the best personal loan in India 2026. Here is how score ranges map to typical rates:

| CIBIL Score | Typical Rate Range | Approval Likelihood |

|---|---|---|

| 800 and above | 9.99% to 11.00% | Very High — best rates available |

| 750 to 799 | 11.00% to 13.00% | High — competitive rates |

| 700 to 749 | 13.00% to 18.00% | Moderate — higher rates |

| 650 to 699 | 18.00% to 24.00% | Low — mostly NBFCs and digital lenders only |

| Below 650 | 24.00% to 36.00% or rejection | Very Low — consider improving score first |

If your CIBIL score is below 700 right now, you are better off spending 3 to 4 months improving it before applying for a personal loan. Even moving from 680 to 720 can reduce your personal loan rate by 4% to 6% — saving thousands in interest. Read our complete guide on how to improve your CIBIL score for step-by-step actions that work.

Key Things to Check Before Taking the Best Personal Loan in India 2026

Effective Annual Rate vs Stated Rate

The interest rate advertised by lenders is not always the true cost of your loan. Processing fees, GST on fees, insurance charges, and other upfront costs add to your effective borrowing cost. Always calculate the total amount you will repay — principal plus all charges — and divide by the loan amount and tenure to understand your true annualised cost before signing.

Prepayment and Foreclosure Charges

Unlike home loans, personal loans in India can have prepayment charges — typically 2% to 5% of the outstanding principal if you repay early. This matters because if you get a salary hike or a windfall and want to close the loan early, you may face a significant fee. Always check the prepayment terms before selecting a lender.

Part-Payment Facility

Some lenders allow part-payment — paying a lump sum toward the principal to reduce future EMIs or tenure — while others do not. If you expect to receive a bonus or tax refund during the loan period, choose a lender that allows part-payment without penalty.

Processing Fee Negotiation

Processing fees of 1% to 3% on a ₹5 lakh loan add up to ₹5,000 to ₹15,000 — often waivable or reducible through negotiation, especially if you are an existing customer or applying during a promotional period. Always ask for a processing fee waiver before accepting the loan offer.

Personal Loan vs Credit Card EMI vs BNPL — Which Is Better in 2026?

| Feature | Personal Loan | Credit Card EMI | Buy Now Pay Later |

|---|---|---|---|

| Interest Rate | 9.99% to 24% per year | 12% to 18% per year (0% for short tenures on offers) | 0% to 36% per year |

| Loan Amount | Up to ₹50 lakh | Up to your credit limit | Typically up to ₹1 to ₹2 lakh |

| Disbursal Time | Minutes to 2 days | Instant (on card swipe) | Instant at checkout |

| Tenure | 1 to 8 years | 3 to 24 months | 1 to 12 months typically |

| Impact on CIBIL | Hard inquiry on application | Reduces available credit limit | Varies by BNPL provider |

| Best For | Large amounts, multi-year repayment | Existing purchase on credit card, short tenure | Small purchases at 0% for 3 months |

For amounts above ₹2 lakh and tenures above 12 months, a personal loan from the best personal loan lender in India 2026 is almost always the most cost-effective option. For smaller purchases where your credit card offers 0% EMI, convert to credit card EMI instead. Read our guide on the best credit cards in India 2026 to find cards with the best 0% EMI offers and cashback on purchases.

How to Apply for the Best Personal Loan in India 2026 — Step by Step

- Check your CIBIL score: Know where you stand before applying. A score above 750 gets you the best rates. If below 700, delay and improve first.

- Calculate the exact amount you need: Borrow only what you need — not the maximum you qualify for. Every extra rupee borrowed costs you in interest.

- Compare at least 3 lenders: Use PaisaBazaar or BankBazaar to compare offers from multiple lenders without triggering multiple hard inquiries.

- Check your existing bank first: Your salary account bank almost always offers pre-approved loans at the best rates to existing customers. Check your banking app before going elsewhere.

- Negotiate processing fee: Always ask for a waiver or reduction before accepting any offer.

- Read the foreclosure terms: Confirm prepayment charges before signing — you may want to close the loan early if your finances improve.

- Apply and complete eKYC: Most lenders in 2026 offer fully digital applications with Aadhaar OTP-based eKYC and instant disbursal for eligible borrowers.

Before taking a personal loan, also consider whether your financial foundation is solid. If you are borrowing because of a genuine emergency and do not have adequate savings, read our guide on how to build an emergency fund in India after repaying this loan so you never need to borrow for emergencies again. And if you are thinking about a home loan alongside or after your personal loan, our comprehensive guide on best home loan interest rates in India 2026 will help you plan that next step.

Conclusion — Compare Before You Borrow the Best Personal Loan in India 2026

The best personal loan in India 2026 is not the one with the flashiest app or the fastest approval — it is the one with the lowest effective interest rate, reasonable processing fee, flexible prepayment terms, and a loan amount that matches what you genuinely need. For the lowest rates, public sector banks like Union Bank and SBI start from 8.75% to 9.60% per year. For the fastest disbursal, HDFC Bank and ICICI Bank offer pre-approved instant loans. For higher amounts up to ₹50 lakh, ICICI is the strongest option. For longer tenure up to 8 years, Bajaj Finserv gives the most flexibility.

Always check your CIBIL score before applying, compare at least 3 lenders, negotiate the processing fee, and borrow only what you genuinely need and can repay comfortably. The best personal loan in India 2026 is a tool — used wisely it solves a problem, used carelessly it creates a bigger one.

At Smashora, our mission is to help every Indian make every rupee count. If this guide on the best personal loan in India 2026 helped you understand your options, leave a comment below or share it with someone who is comparing personal loan offers right now.

Frequently Asked Questions

Which bank gives the best personal loan in India in 2026?

For the lowest interest rates, Union Bank of India and Bank of Maharashtra start from 8.75% per year making them the most affordable personal loan options in India in 2026. For instant disbursal, HDFC Bank and ICICI Bank are the strongest choices with pre-approved loans disbursed in minutes for eligible customers. For the highest loan amount up to ₹50 lakh, ICICI Bank is the top option. For government employees, SBI Xpress Credit offers special concession rates making it the best personal loan choice for that profile.

What CIBIL score do I need to get the best personal loan rate in India in 2026?

A CIBIL score of 750 and above qualifies you for the best personal loan interest rates in India 2026 — typically 9.99% to 11.00% per year at major banks. A score of 800 and above may get you additional rate concessions. Below 700, most banks will either decline or offer rates of 15% to 24% per year which significantly increases your total repayment cost. Spending 3 to 4 months improving your CIBIL score before applying is almost always worth the wait for the interest savings it delivers.

Can I get an instant personal loan in India in 2026?

Yes. Most major banks in India in 2026 offer instant pre-approved personal loans for eligible customers. HDFC Bank disburses pre-approved loans within seconds via the mobile banking app. ICICI Bank, SBI (via YONO), Axis Bank, and Kotak Bank all offer instant loan facilities for existing customers with a clean repayment history. For non-bank customers, digital lenders like MoneyView, Navi, and KreditBee offer loans with approvals in minutes — but typically at significantly higher rates of 15% to 36% per year. Always compare the instant loan rate against your bank’s offer before accepting a digital lender’s offer for convenience.

What documents are needed for a personal loan in India in 2026?

For salaried individuals applying for the best personal loan in India 2026, the standard documents needed are: PAN card, Aadhaar card for eKYC, last 3 months salary slips, last 6 months bank statement showing salary credits, and Form 16 or latest ITR for income verification. Many lenders in 2026 accept digital documents via DigiLocker and complete the full KYC process online without any physical submission. For self-employed applicants, additional documents including business registration proof and 2 years of ITR are typically required.

What is the maximum personal loan amount I can get in India in 2026?

The maximum personal loan amount in India in 2026 depends on your income, CIBIL score, and the lender. ICICI Bank offers up to ₹50 lakh, HDFC Bank and Axis Bank up to ₹40 lakh, and Bajaj Finserv up to ₹40 lakh. Most lenders cap the loan amount at 10 to 20 times your monthly net salary. So for a monthly net salary of ₹60,000, you may qualify for a maximum of ₹6 lakh to ₹12 lakh depending on your existing EMI obligations and CIBIL score. Your total EMI burden including the new loan should not exceed 50% to 60% of your monthly net income for most lenders.

Should I take a personal loan or a credit card loan for a large expense in 2026?

For amounts above ₹2 lakh and repayment periods longer than 12 months, a personal loan is almost always cheaper than converting a credit card bill into EMI. Credit card EMI conversion rates are typically 12% to 18% per year and may include upfront processing fees. A personal loan from a bank at 10% to 12% for the same amount and tenure saves meaningful interest. The exception is 0% EMI offers on specific purchases at specific retailers — for those short tenure zero-cost conversions, the credit card EMI is clearly better. For everything else, compare the personal loan rate from your bank against the credit card EMI rate before deciding.