Contents

- 1 What Is a Recurring Deposit and Who Should Use One

- 2 Best Recurring Deposit Interest Rates in India 2026 — Public Sector Banks

- 3 Best Recurring Deposit Interest Rates in India 2026 — Private Banks

- 4 Best Recurring Deposit Interest Rates in India 2026 — Small Finance Banks

- 5 How RD Interest Is Calculated

- 6 Recurring Deposit vs Fixed Deposit — Key Differences

- 7 Taxation on Recurring Deposits in India 2026

- 8 How to Choose Between Bank, Post Office, and Small Finance Bank RDs

- 9 RD as a Tool Within Your Broader Savings Strategy

- 10 Premature Withdrawal and Missed Instalment Rules

- 11 Conclusion — Match Your RD Choice to Your Monthly Savings Capacity

- 12 Frequently Asked Questions

- 12.1 Which bank offers the best recurring deposit interest rate in India in 2026?

- 12.2 What is the difference between RD and FD?

- 12.3 How is RD interest calculated in India?

- 12.4 Is RD interest taxable in India?

- 12.5 What happens if I miss a monthly RD instalment?

- 12.6 Can I withdraw my RD before maturity in India?

For anyone who wants to save a fixed amount every month with guaranteed, predictable returns, finding the best recurring deposit interest rates in India 2026 is the natural starting point. A Recurring Deposit (RD) lets you invest a small, consistent monthly amount — as little as ₹100 to ₹1,000 — over a chosen tenure, with the entire amount plus interest paid out at maturity. Unlike a Fixed Deposit which requires a lump sum upfront, an RD is built specifically for people who earn and save monthly, making it one of the most accessible disciplined savings tools in India.

The rate spread across lenders for RDs in 2026 is meaningfully wide. SBI offers RD rates ranging from 4.50% to 7.00% for general citizens, while small finance banks push as high as 9.60% per annum for the same guaranteed, government-regulated product. On a ₹5,000 monthly RD over 5 years, the difference between a 5% rate and a 9% rate compounds into a meaningfully larger maturity amount — money that adds up specifically because RDs reward consistent monthly discipline rather than one-time lump sum decisions.

This complete guide on the best recurring deposit interest rates in India 2026 covers current rates across public banks, private banks, and small finance banks, how RD interest is calculated and taxed, the key differences between RD and FD, and a practical framework for deciding when an RD is the right tool for your specific savings goal.

What Is a Recurring Deposit and Who Should Use One

A Recurring Deposit is a fixed-tenure savings instrument where you deposit a predetermined amount every month, and the bank pays a fixed interest rate on the cumulative balance, compounded quarterly in most cases. At the end of the chosen tenure — ranging from 6 months to 10 years depending on the bank — you receive the total principal deposited plus all accumulated interest as a lump sum.

RDs are particularly well suited for:

- Salaried individuals building toward a specific short to medium-term goal — a vacation, a gadget purchase, a wedding expense, or seed money for a larger investment

- Anyone without a lump sum to invest in a Fixed Deposit but who can commit to a smaller, consistent monthly outflow

- Building the habit of disciplined saving — the fixed monthly commitment functions similarly to a forced savings mechanism, much like a SIP does for mutual fund investing

- Risk-averse savers who want a completely guaranteed, government-regulated return with zero market exposure

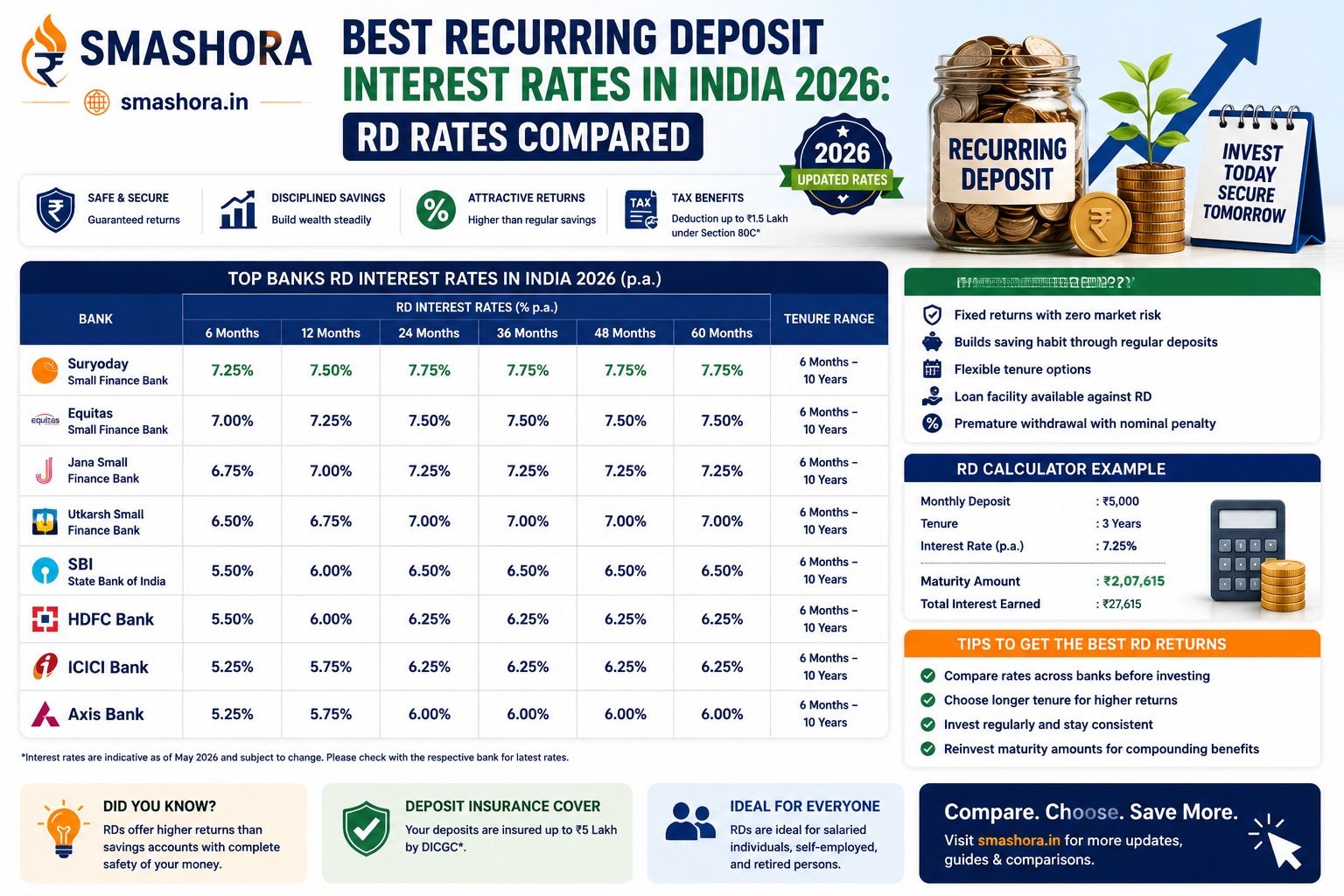

Best Recurring Deposit Interest Rates in India 2026 — Public Sector Banks

| Bank | General Citizen Rate | Senior Citizen Rate | Minimum Monthly Deposit |

|---|---|---|---|

| State Bank of India | 4.50% to 7.00% per year | 5.00% to 7.50% per year | ₹100 |

| Indian Bank | Up to 7.00% per year | Up to 7.50% per year | ₹100 to ₹500 |

| Indian Overseas Bank | Up to 7.00% per year | Up to 7.50% per year | ₹100 to ₹500 |

| UCO Bank | Up to 7.00% per year | Up to 7.50% per year | ₹100 to ₹500 |

Best Recurring Deposit Interest Rates in India 2026 — Private Banks

| Bank | General Citizen Rate | Senior Citizen Rate | Tenure Range |

|---|---|---|---|

| HDFC Bank | 5.50% to 7.00% per year | 5.00% to 7.75% per year | 6 months to 10 years |

| Axis Bank | Up to 7.00% per year | Up to 7.50% per year | 6 months to 10 years |

| ICICI Bank | Competitive with HDFC and Axis | 0.50% premium over general rate | 6 months to 10 years |

Best Recurring Deposit Interest Rates in India 2026 — Small Finance Banks

Small finance banks consistently offer the best recurring deposit interest rates in India 2026, often 2% to 3% higher than equivalent public or private bank rates for the same tenure — while remaining equally regulated and DICGC-insured up to ₹5 lakh per depositor per bank.

| Bank Category | Interest Rate Range | DICGC Insured |

|---|---|---|

| Small Finance Banks (general range) | 5.60% to 9.60% per year | Yes, up to ₹5 lakh per depositor |

| Select Small Finance Banks (top end) | Up to 9.60% per year | Yes, up to ₹5 lakh per depositor |

For a saver depositing ₹5,000 per month into a small finance bank RD at 9% instead of a public sector bank RD at 6.5% over a 5-year tenure, the difference in final maturity value runs into several thousand rupees — purely from choosing the higher-rate, equally regulated institution. Always confirm the specific small finance bank’s current published rate and DICGC coverage before opening an account, since rates are revised periodically without prior notice.

How RD Interest Is Calculated

RD interest is calculated on each individual monthly instalment from its date of deposit until maturity, and is typically compounded quarterly. This means the first month’s deposit earns interest for the entire tenure, while the last month’s deposit earns interest for only the final period before maturity. The bank’s RD calculator handles this automatically, but understanding the mechanism explains why the effective yield on an RD is slightly different from a simple multiplication of the rate by the total deposited amount.

Recurring Deposit vs Fixed Deposit — Key Differences

| Feature | Recurring Deposit | Fixed Deposit |

|---|---|---|

| Investment Style | Fixed monthly instalments | One-time lump sum |

| Interest Rate (typical range) | 5% to 9.6% depending on bank | Up to 8% to 9.1% at general banks, higher at small finance banks |

| Minimum Entry | As low as ₹100 per month | Typically ₹1,000 to ₹5,000 lump sum |

| Best For | Savers without a lump sum, building disciplined monthly habit | Savers with an existing lump sum seeking maximum guaranteed return |

| Premature Withdrawal | Allowed with penalty or reduced rate | Allowed with penalty, varies by bank |

| Tax Treatment | Fully taxable, TDS at 10% above ₹50,000 interest (₹1,00,000 for seniors) | Fully taxable, similar TDS thresholds apply |

Fixed Deposit interest rates in India in 2026 generally run slightly higher than RD rates at the same bank for comparable tenures — for instance, general bank FD rates can reach up to 8% to 9.1% at select institutions, compared to RDs typically capping around 7% to 7.75% at the same large banks, though small finance bank RDs can match or exceed many FD rates. The fundamental decision is less about which product has the marginally higher rate and more about whether you have a lump sum to deposit today (favouring FD) or a consistent monthly surplus to commit (favouring RD). For a complete breakdown of current FD rates across all bank categories, read our detailed guide on the best FD rates in India 2026.

Taxation on Recurring Deposits in India 2026

RD interest is fully taxable as income at your applicable income tax slab rate — there is no special tax exemption or 80C benefit for recurring deposits, unlike the 5-year Tax Saving FD which does qualify for Section 80C.

| Annual RD Interest Earned | TDS Applicability |

|---|---|

| Up to ₹50,000 (general citizens) | No TDS deducted |

| Above ₹50,000 (general citizens) | 10% TDS deducted by the bank |

| Up to ₹1,00,000 (senior citizens) | No TDS deducted |

| Above ₹1,00,000 (senior citizens) | 10% TDS deducted by the bank |

| PAN not submitted to bank | 20% TDS deducted instead of 10% |

These TDS thresholds were revised by the Finance Act 2025, effective April 2025, raising the limits from the previous ₹40,000 and ₹50,000 to the current ₹50,000 and ₹1,00,000 respectively. If your total annual income is below the taxable threshold, you can submit Form 15G (non-senior citizens) or Form 15H (senior citizens) to your bank at the start of the financial year to avoid TDS deduction altogether on your RD interest.

How to Choose Between Bank, Post Office, and Small Finance Bank RDs

| Institution Type | Typical Rate Range | Best For |

|---|---|---|

| Public Sector Banks (SBI, Indian Bank, UCO Bank) | 4.50% to 7.50% | Maximum safety perception, wide branch access |

| Private Banks (HDFC, Axis, ICICI) | 5.50% to 7.75% | Strong digital RD account management |

| Small Finance Banks | 5.60% to 9.60% | Highest rates while remaining DICGC insured up to ₹5 lakh |

For most disciplined monthly savers comfortable with online banking, opening an RD at a small finance bank offering 8% to 9.6% delivers a meaningfully higher maturity value than the same monthly commitment at a large public sector bank offering 6% to 7%, with no meaningful difference in safety as long as your total deposit (principal plus accrued interest) stays within the ₹5 lakh DICGC insurance limit at that institution.

RD as a Tool Within Your Broader Savings Strategy

A Recurring Deposit works particularly well as a structured complement to your monthly budgeting discipline. If you follow a 50-30-20 budgeting approach, an RD is a natural home for a portion of your monthly savings bucket — especially for goals with a fixed, known timeline of 1 to 3 years where capital safety matters more than growth potential. For a complete framework on structuring your monthly savings across different goals and instruments, read our guide on how to save money every month in India 2026.

RDs are also a practical building block for an emergency fund target, since the fixed monthly commitment ensures steady progress toward a 3 to 6 month expense buffer without requiring market exposure or large upfront capital. Our detailed guide on how to build an emergency fund in India covers how RDs fit alongside savings accounts and liquid funds in this specific use case.

For longer-term wealth building beyond 5 years, however, RDs are generally not the most efficient instrument — their fixed, fully taxable returns are typically outpaced over longer horizons by PPF’s tax-free compounding or equity mutual fund SIPs’ historically higher growth. Our comprehensive comparison in PPF vs FD vs mutual fund in India 2026 provides the complete picture for choosing the right instrument based on your specific time horizon and risk tolerance.

Premature Withdrawal and Missed Instalment Rules

- Missed monthly instalment: Most banks charge a small penalty fee for each missed instalment, and consistently missed payments can lead to account closure before maturity at some institutions

- Premature closure: Closing an RD before the agreed tenure typically results in a reduced interest rate — usually the rate applicable to the actual period the deposit was held, minus a penalty of 0.50% to 1%

- Additional instalments: Some banks allow you to deposit an extra instalment in a given month, though the additional amount typically does not earn interest beyond the standard monthly schedule

- Loan against RD: Many banks offer a loan or overdraft facility against your RD balance, typically up to 80% to 90% of the accumulated value, useful for short-term liquidity needs without breaking the deposit

Conclusion — Match Your RD Choice to Your Monthly Savings Capacity

The best recurring deposit interest rates in India 2026 are found at small finance banks, where rates of 8% to 9.60% significantly outpace the 4.50% to 7.75% range typical at large public and private banks for the same tenure — all while maintaining equal DICGC-backed safety up to ₹5 lakh per depositor. For savers who want maximum convenience and a long-standing banking relationship, SBI, HDFC, and Axis remain solid, lower-risk-perception choices, particularly for amounts above the DICGC insurance threshold where spreading across multiple small finance banks becomes impractical.

Whatever institution you choose, the genuine value of an RD lies less in chasing the absolute highest rate and more in the discipline it builds — committing to a fixed monthly amount toward a specific goal is one of the most reliable ways to convert income into savings without relying on willpower alone each month.

At Smashora, our mission is to help every Indian make every rupee count. If this guide on the best recurring deposit interest rates in India 2026 helped you choose the right RD for your monthly savings goal, leave a comment below or share it with a friend who is starting their first disciplined savings habit. For more information visit RBI Website

Frequently Asked Questions

Which bank offers the best recurring deposit interest rate in India in 2026?

Small finance banks consistently offer the best recurring deposit interest rates in India 2026, with rates ranging from 5.60% to as high as 9.60% per annum, significantly higher than the 4.50% to 7.75% range typically available at large public and private sector banks like SBI, HDFC, and Axis Bank for comparable tenures. Despite the higher rates, small finance bank RDs remain equally safe, since deposits up to ₹5 lakh per depositor per bank are covered by the same DICGC insurance that protects deposits at SBI and HDFC.

What is the difference between RD and FD?

A Recurring Deposit (RD) requires you to deposit a fixed amount every month over a chosen tenure, with the total principal and accumulated interest paid at maturity — making it ideal for savers without a lump sum but with a consistent monthly surplus. A Fixed Deposit (FD) requires a one-time lump sum deposit upfront, which then earns interest until maturity. FD rates at the same bank are often marginally higher than RD rates for comparable tenures, but the choice between the two is primarily determined by whether you have a lump sum available now (favouring FD) or prefer to build savings through consistent monthly contributions (favouring RD).

How is RD interest calculated in India?

RD interest is calculated separately on each monthly instalment from its specific date of deposit until the RD’s maturity date, and is typically compounded quarterly. This means earlier instalments earn interest for a longer period than later instalments. Banks provide RD calculators on their websites and apps that automatically compute the exact maturity value based on your monthly deposit amount, interest rate, and chosen tenure, removing the need for manual calculation.

Is RD interest taxable in India?

Yes. Recurring Deposit interest is fully taxable as income at your applicable income tax slab rate, with no special exemption like the EEE treatment available for instruments such as PPF. Banks deduct TDS at 10% if your annual RD interest exceeds ₹50,000 for general citizens or ₹1,00,000 for senior citizens, as per the Finance Act 2025 revisions effective from April 2025. If your total income is below the taxable threshold, you can submit Form 15G or Form 15H to your bank to avoid TDS deduction at source.

What happens if I miss a monthly RD instalment?

Most banks charge a small penalty fee for each missed RD instalment, and the exact penalty amount varies by bank and the specific monthly deposit value. If instalments are missed repeatedly beyond what the bank’s policy allows, the account may be closed before the original maturity date, at which point you typically receive the principal deposited plus interest calculated at a reduced rate reflecting the shorter actual holding period. It is advisable to set up an automatic standing instruction from your savings account to ensure RD instalments are never missed due to oversight.

Can I withdraw my RD before maturity in India?

Yes, premature withdrawal of an RD is generally allowed at most banks, but it comes with a penalty — typically the interest rate is reduced to the rate applicable for the actual period the deposit was held, often with an additional penalty of 0.50% to 1% deducted from that rate. Some banks also offer a loan or overdraft facility against your RD balance, allowing you to access funds for short-term needs without breaking the deposit and losing the benefit of the originally agreed interest rate.