Contents

- 1 What is Section 80C and How Much Tax Can You Save?

- 2 Complete List of Section 80C Eligible Investments and Expenses in 2026

- 3 How to Save Tax Under Section 80C in India 2026 — The Best Strategy

- 4 Best Section 80C Investment Options Compared — ELSS vs PPF vs LIC

- 5 ELSS — The Best 80C Option for Young Investors in 2026

- 6 How to Save Tax Under Section 80C in India 2026 — Recommended Portfolios by Profile

- 7 Section 80C vs Section 80CCC vs Section 80CCD — What Is the Difference?

- 8 Common Mistakes When Claiming Section 80C Deductions in 2026

- 9 How Much Tax Can You Save With Full 80C Plus NPS in 2026?

- 10 Conclusion — Start Saving Tax Under Section 80C in India 2026 From April Itself

- 11 Frequently Asked Questions

- 11.1 What is the maximum deduction under Section 80C in 2026?

- 11.2 Which is the best Section 80C investment option in India in 2026?

- 11.3 Does EPF contribution count toward the 80C limit?

- 11.4 Can I claim both Section 80C and Section 80D in the same year?

- 11.5 Is Section 80C available under the New Tax Regime in 2026?

- 11.6 Can I invest in both PPF and ELSS for Section 80C in the same year?

If you want to know how to save tax under Section 80C in India 2026, you are asking one of the most financially rewarding questions a salaried Indian can ask. Section 80C of the Income Tax Act allows you to reduce your taxable income by up to ₹1.5 lakh per year — which translates to a direct tax saving of ₹15,000 to ₹46,800 depending on your income tax slab. That is real money that stays in your pocket every year, year after year, simply by making the right investment choices.

The frustrating reality is that most salaried Indians use only one or two 80C options — typically a provident fund contribution through their employer and maybe a life insurance premium — and never fully utilise the entire ₹1.5 lakh limit. I have seen colleagues earning ₹12 lakh per year paying ₹20,000 to ₹30,000 more in tax than necessary simply because nobody explained that their home loan principal repayment, children’s school fees, and PPF contributions all count toward the same ₹1.5 lakh limit.

In 2026, with the July 31 ITR filing deadline approaching and the Old Tax Regime still offering significant advantages for investors with multiple deductions, understanding how to save tax under Section 80C in India 2026 is more important than ever. This complete guide covers every eligible investment and expense under Section 80C, their current returns and lock-in periods, and exactly how to build the most effective 80C portfolio for your income level and financial goals.

What is Section 80C and How Much Tax Can You Save?

Section 80C of the Income Tax Act allows individual taxpayers and Hindu Undivided Families (HUF) to claim a deduction of up to ₹1.5 lakh from their gross taxable income in a financial year. This deduction is available only under the Old Tax Regime — not the New Tax Regime which offers lower slab rates but no deductions.

Here is the exact tax saving you get by fully utilising the ₹1.5 lakh Section 80C deduction:

| Income Tax Slab | Tax Rate | Tax Saved on ₹1.5 Lakh 80C Investment | With 4% Cess |

|---|---|---|---|

| Up to ₹2.5 lakh | Nil | ₹0 | ₹0 |

| ₹2.5 lakh to ₹5 lakh | 5% | ₹7,500 | ₹7,800 |

| ₹5 lakh to ₹10 lakh | 20% | ₹30,000 | ₹31,200 |

| Above ₹10 lakh | 30% | ₹45,000 | ₹46,800 |

For a salaried individual in the 30% tax bracket, fully utilising the ₹1.5 lakh Section 80C limit saves ₹46,800 every single year. Over a 30-year career, that is over ₹14 lakh in cumulative tax savings — money that could have been invested and compounded into a significantly larger corpus.

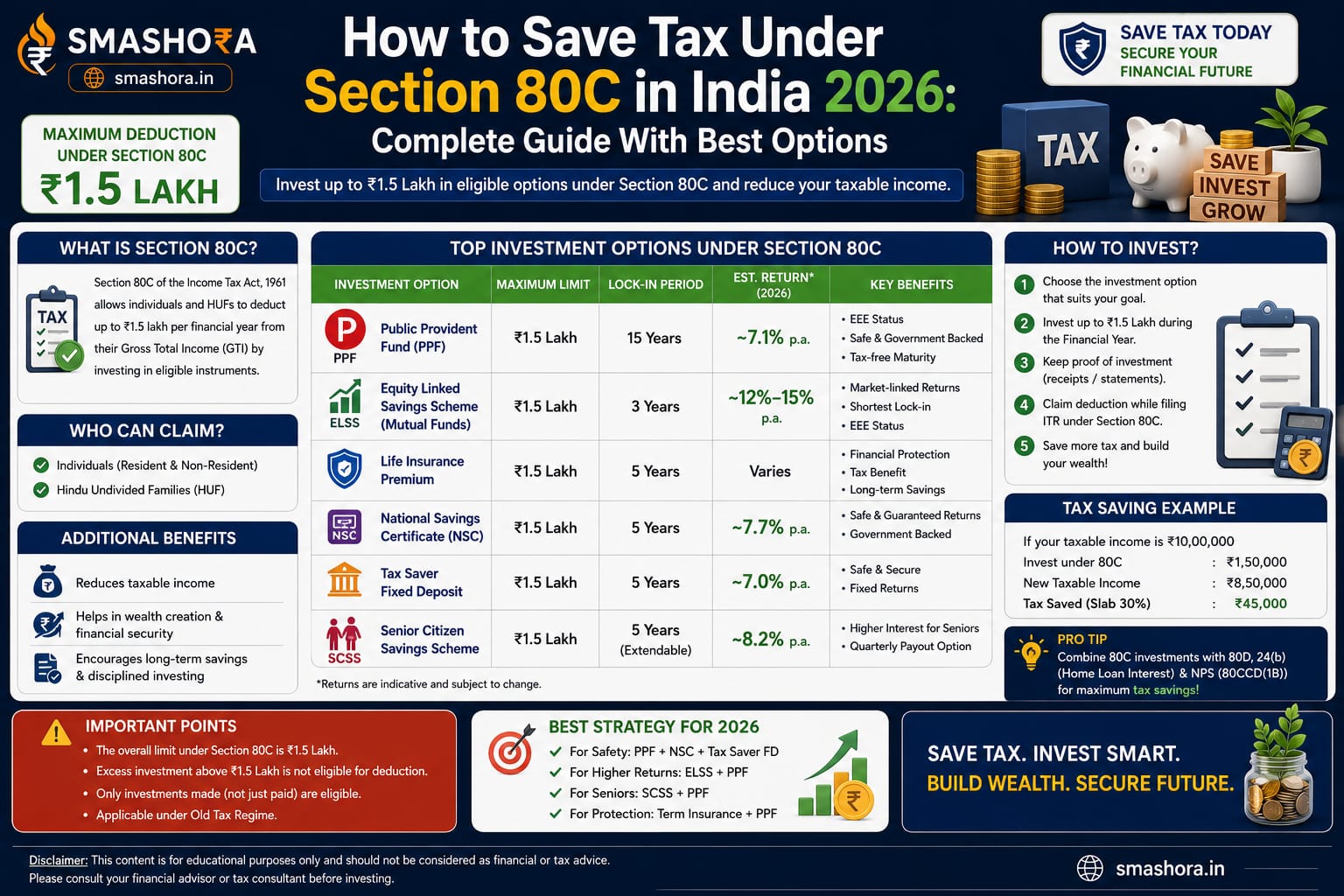

Complete List of Section 80C Eligible Investments and Expenses in 2026

Learning how to save tax under Section 80C in India 2026 starts with understanding everything that qualifies. The complete list is broader than most people realise:

Investment Options Under Section 80C

| Investment Option | Current Returns | Lock-in Period | Risk Level | Tax on Returns |

|---|---|---|---|---|

| ELSS Mutual Funds | 11% to 14% per year (historical) | 3 years | High (market-linked) | 10% LTCG above ₹1.25 lakh |

| Public Provident Fund (PPF) | 7.1% per year | 15 years | Zero (government backed) | Tax free (EEE) |

| Sukanya Samriddhi Yojana | 8.2% per year | 21 years | Zero (government backed) | Tax free (EEE) |

| National Savings Certificate | 7.7% per year | 5 years | Zero (government backed) | Taxable at maturity |

| 5-Year Post Office Time Deposit | 7.5% per year | 5 years | Zero (government backed) | Taxable as income |

| 5-Year Tax Saving Bank FD | 6.5% to 7.5% per year | 5 years | Very Low (DICGC insured) | Taxable as income |

| Senior Citizen Savings Scheme | 8.2% per year | 5 years | Zero (government backed) | Interest taxable quarterly |

| Employee Provident Fund (EPF) | 8.15% per year | Until retirement | Zero (government backed) | Tax free on withdrawal after 5 years |

| Life Insurance Premium (LIC or private) | 4% to 6% effective (traditional) | Policy term | Very Low | Death benefit tax free under 10(10D) |

| Unit Linked Insurance Plan (ULIP) | Market-linked | 5 years | Moderate to High | Complex — conditions apply |

Expenses That Also Qualify for Section 80C

Many salaried Indians do not realise that certain regular expenses — not just investments — also count toward the ₹1.5 lakh Section 80C limit:

- Home Loan Principal Repayment: The principal component of your home loan EMI qualifies for Section 80C deduction. If your annual EMI is ₹3.6 lakh and ₹1 lakh of that is principal, the full ₹1 lakh counts toward your 80C limit.

- Children’s Tuition Fees: Tuition fees paid to any school, college, university, or educational institution in India for up to 2 children qualify under Section 80C. Only tuition fees count — not development fees, transport fees, or other charges.

- Stamp Duty and Registration Charges: Stamp duty and registration charges paid for a residential property purchase qualify for 80C deduction in the year of payment.

How to Save Tax Under Section 80C in India 2026 — The Best Strategy

The smartest approach to how to save tax under Section 80C in India 2026 is not to invest the entire ₹1.5 lakh in one product. It is to build a layered 80C portfolio that combines guaranteed returns with growth potential based on your risk tolerance and goals.

Step 1 — First Count What Is Already Being Invested Automatically

Many salaried employees already have a portion of their 80C limit filled without realising it. Check these first before making any new investments:

- Employee Provident Fund (EPF): Your 12% salary contribution to EPF every month is automatically counted under Section 80C. If your monthly basic salary is ₹30,000, your annual EPF contribution is approximately ₹43,200 — already eating into your ₹1.5 lakh limit.

- Life Insurance Premium: Any LIC or private life insurance premium you are already paying counts toward 80C.

- Home Loan Principal: The principal repayment in your home loan EMI counts automatically once you declare it in your ITR.

- Children’s Tuition Fees: If you are paying school or college tuition for your children, this automatically qualifies.

Add up all of the above. The remaining gap between your total and ₹1.5 lakh is how much you need to invest additionally in 80C instruments to maximise your deduction.

Step 2 — Fill the Remaining Limit With the Best 80C Investments

For most salaried professionals in 2026, the best way to fill the remaining 80C limit after EPF is a combination of ELSS and PPF — one for maximum growth and one for guaranteed tax-free returns.

Best Section 80C Investment Options Compared — ELSS vs PPF vs LIC

When learning how to save tax under Section 80C in India 2026, the most important comparison is between the three most popular 80C instruments: ELSS funds, PPF, and life insurance premiums. Here is a clear head-to-head:

| Feature | ELSS Mutual Fund | PPF | LIC Traditional Policy |

|---|---|---|---|

| Expected Returns | 11% to 14% per year (historical) | 7.1% per year (guaranteed) | 4% to 6% per year (effective) |

| Lock-in Period | 3 years (shortest among 80C options) | 15 years | Full policy term (10 to 30 years) |

| Tax on Returns | 10% LTCG above ₹1.25 lakh per year | Completely tax free | Death benefit tax free, survival benefit conditions apply |

| Risk | Market risk — can fall in short term | Zero | Near zero |

| Recommended For | Young investors, long-term wealth | All investors for guaranteed tax-free base | Primarily not recommended for pure investment |

The honest financial advice for 2026 is clear: if you need life insurance, buy the best term insurance plan separately — not a traditional LIC endowment or money-back plan as an 80C investment. Term insurance gives you 100 times more life cover for the same premium. Use the 80C limit for actual investment — ELSS and PPF — not for bundled insurance-investment products that deliver poor returns on both counts.

Read our complete guide on the best term insurance plans in India 2026 to understand why pure term insurance at a fraction of the cost is far superior to traditional LIC policies for life protection.

ELSS — The Best 80C Option for Young Investors in 2026

If you are between 25 and 45 years old and want to know how to save tax under Section 80C in India 2026 while also building serious long-term wealth, ELSS (Equity Linked Savings Scheme) is the answer. ELSS is the only mutual fund category that qualifies for Section 80C deduction and it comes with the shortest lock-in period of just 3 years among all 80C instruments.

Why ELSS Stands Out

- Highest returns among 80C options: ELSS funds have historically delivered 11% to 14% annualised returns over 7 to 10 year periods — significantly better than PPF at 7.1% or NSC at 7.7%

- Shortest lock-in: 3-year lock-in is the minimum among all 80C instruments. After 3 years your money is fully accessible.

- SIP friendly: You can invest as little as ₹500 per month in ELSS via SIP — making it easy to build your 80C corpus gradually throughout the year rather than rushing a lump sum in March

- Tax-efficient returns: Long term capital gains on ELSS above ₹1.25 lakh per year are taxed at only 10% — significantly better than FD or NSC returns which are taxed at your full income slab rate

Top ELSS Funds for Section 80C in 2026

| ELSS Fund | 3-Year Returns | 5-Year Returns | Minimum SIP |

|---|---|---|---|

| Mirae Asset ELSS Tax Saver Fund | 18.2% per year | 16.8% per year | ₹500 per month |

| Quant ELSS Tax Saver Fund | 22.1% per year | 28.3% per year | ₹500 per month |

| SBI Long Term Equity Fund | 17.5% per year | 18.2% per year | ₹500 per month |

| Canara Robeco ELSS Tax Saver | 16.8% per year | 17.1% per year | ₹500 per month |

For a comprehensive guide on starting SIP investments including ELSS, read our detailed article on the best SIP to start in India 2026.

How to Save Tax Under Section 80C in India 2026 — Recommended Portfolios by Profile

Here are practical 80C portfolio recommendations based on your age and financial situation:

For Young Professionals (Age 22 to 35)

| Investment | Annual Amount | Reason |

|---|---|---|

| EPF contribution (auto-deducted) | As per salary | Already invested — count this first |

| ELSS SIP | Remaining 80C gap | Highest long-term returns, 3-year lock-in |

| PPF (if ELSS limit not reached) | Up to ₹1.5 lakh total | Guaranteed tax-free base |

For Mid-Career Professionals With Home Loan (Age 35 to 50)

| Investment | Annual Amount | Reason |

|---|---|---|

| EPF contribution (auto-deducted) | As per salary | Count first |

| Home loan principal repayment | Actual principal paid | Already being paid — declare in ITR |

| Children’s tuition fees | Actual fees paid | Count what you are already paying |

| ELSS or PPF for remaining gap | Balance to reach ₹1.5 lakh | Top up with best performing option |

For Conservative Investors and Those Near Retirement (Age 50 Plus)

| Investment | Annual Amount | Reason |

|---|---|---|

| EPF contribution | As per salary | Count first |

| PPF | Up to ₹1.5 lakh | Guaranteed tax-free returns close to retirement |

| NSC | Balance of 80C limit | 5-year guaranteed return with 80C benefit |

| 5-year tax saving FD | Any remaining gap | Capital safety over growth |

Section 80C vs Section 80CCC vs Section 80CCD — What Is the Difference?

Many taxpayers confuse the different subsections. Here is a clear breakdown:

| Section | What It Covers | Limit |

|---|---|---|

| Section 80C | EPF, PPF, ELSS, NSC, FD, LIC, SSY, home loan principal, tuition fees | ₹1.5 lakh per year |

| Section 80CCC | Pension plans from insurance companies (LIC Jeevan Suraksha etc.) | Within ₹1.5 lakh combined limit |

| Section 80CCD(1) | NPS contribution by employee (up to 10% of basic salary) | Within ₹1.5 lakh combined limit |

| Section 80CCD(1B) | Additional NPS contribution over and above ₹1.5 lakh | Additional ₹50,000 over the 80C limit |

| Section 80CCD(2) | Employer contribution to NPS on behalf of employee | Up to 10% of basic salary, no cap |

The important takeaway here: Section 80CCD(1B) gives you an additional ₹50,000 deduction for NPS investment over and above the ₹1.5 lakh 80C limit. If you are in the 30% tax bracket and invest ₹50,000 in NPS under 80CCD(1B), you save an additional ₹15,600 in taxes. This is one of the most underutilised tax saving opportunities among salaried Indians.

Common Mistakes When Claiming Section 80C Deductions in 2026

Investing at the Last Minute in March

Many Indians scramble to invest their entire ₹1.5 lakh in 80C instruments in February and March — right before the financial year ends. This approach misses out on 9 to 11 months of compounding and investment growth. Starting 80C SIPs in April at the beginning of the financial year and investing monthly is always better than a last-minute lump sum in March.

Not Declaring Existing Eligible Expenses

Many salaried employees do not realise that home loan principal repayment, school tuition fees, and EPF contributions already cover a large portion of their 80C limit. Always calculate your existing 80C coverage before making fresh investments — you may already be closer to ₹1.5 lakh than you think.

Investing in Traditional LIC Policies for 80C

Traditional endowment and money-back policies from LIC give 4% to 6% effective returns over 20 to 30 years — far below PPF at 7.1%, NSC at 7.7%, or ELSS at 11% to 14%. Paying LIC premiums purely for the 80C benefit while earning poor returns is one of the most common and expensive financial mistakes in India. If you already have such policies running, consider whether to continue or surrender after checking the surrender value.

Choosing the New Tax Regime and Losing All 80C Benefits

The New Tax Regime does not allow Section 80C deductions. For salaried individuals with significant 80C investments, home loan interest, and HRA, the Old Tax Regime almost always results in lower total tax. Calculate your tax under both regimes before selecting. For a step-by-step guide on making this comparison when filing your return, read our article on how to file ITR online in India 2026.

How Much Tax Can You Save With Full 80C Plus NPS in 2026?

| Deduction | Maximum Amount | Tax Saved (30% Slab) |

|---|---|---|

| Section 80C (EPF, PPF, ELSS, LIC etc.) | ₹1,50,000 | ₹46,800 |

| Section 80CCD(1B) — NPS additional contribution | ₹50,000 | ₹15,600 |

| Section 80D — Health insurance premium (self and family) | ₹25,000 | ₹7,800 |

| Section 80D — Senior citizen parents health insurance | ₹50,000 | ₹15,600 |

| Section 24(b) — Home loan interest | ₹2,00,000 | ₹62,400 |

| Standard Deduction (Old Regime) | ₹50,000 | ₹15,600 |

| Total Maximum Annual Tax Saving | ₹5,25,000 in deductions | Up to ₹1,63,800 per year |

A salaried individual in the 30% bracket who fully utilises all available deductions — 80C, NPS, health insurance, and home loan interest — can save up to ₹1.63 lakh in taxes every year. That is not a small number. It is money that should be invested in wealth-building instruments like SIPs rather than paid to the government unnecessarily.

To understand all your government-backed 80C investment options in detail, read our complete guide on the best government savings schemes in India 2026. And to understand how PPF compares to FD and mutual funds across all parameters, our article on PPF vs FD vs mutual fund in India 2026 gives you the full picture.

Conclusion — Start Saving Tax Under Section 80C in India 2026 From April Itself

The best time to start investing for how to save tax under Section 80C in India 2026 is the beginning of the financial year — April — not February or March. Start your ELSS SIP today, contribute to PPF monthly, and make sure your employer is accounting for your home loan principal and tuition fees in your salary TDS calculations. Every month of delay costs you both tax savings and compounding returns.

To summarise how to save tax under Section 80C in India 2026 effectively: first count your existing automatic 80C investments — EPF, home loan principal, tuition fees. Then fill the remaining gap to ₹1.5 lakh with ELSS for growth and PPF for guaranteed tax-free returns. Add NPS under 80CCD(1B) for an additional ₹50,000 deduction. File your return under the Old Tax Regime if your total deductions make it more beneficial than the New Regime.

At Smashora, our mission is to help every Indian make every rupee count — including the rupees saved from smart tax planning. If this guide on how to save tax under Section 80C in India 2026 helped you, leave a comment below or share it with a colleague who is still paying more tax than necessary.

Frequently Asked Questions

What is the maximum deduction under Section 80C in 2026?

The maximum deduction under Section 80C in 2026 is ₹1.5 lakh per financial year. This limit covers all eligible investments and expenses combined — EPF, PPF, ELSS, NSC, LIC premium, home loan principal, and tuition fees all count toward the same ₹1.5 lakh ceiling. Additionally, NPS contributions under Section 80CCD(1B) give you an extra ₹50,000 deduction over and above the ₹1.5 lakh 80C limit, effectively allowing up to ₹2 lakh in tax deductions from these two sections combined.

Which is the best Section 80C investment option in India in 2026?

For young investors aged 25 to 40 in the 20% or 30% tax slab, ELSS mutual funds are the best 80C investment in India in 2026 — they offer the highest historical returns of 11% to 14% per year with the shortest lock-in of 3 years. For guaranteed, completely tax-free returns, PPF at 7.1% with EEE treatment is the strongest risk-free 80C option. The ideal approach is to combine both — ELSS for growth and PPF for the guaranteed foundation — rather than putting all your 80C investment in one instrument.

Does EPF contribution count toward the 80C limit?

Yes. Your employee contribution to EPF — which is 12% of your basic salary deducted every month — counts fully toward the ₹1.5 lakh Section 80C limit. Many salaried Indians with a monthly basic of ₹25,000 or more find that their EPF alone contributes ₹36,000 to ₹60,000 toward 80C annually without any additional investment required. Always calculate your EPF contribution first before deciding how much additional 80C investment you need.

Can I claim both Section 80C and Section 80D in the same year?

Yes, absolutely. Section 80C (up to ₹1.5 lakh for EPF, PPF, ELSS etc.) and Section 80D (up to ₹25,000 for health insurance premium for self and family, plus up to ₹50,000 for senior citizen parents) are completely separate deductions with separate limits. You can claim both in the same year. Similarly, 80C and Section 24(b) for home loan interest (up to ₹2 lakh) can also be claimed simultaneously — they are independent of each other.

Is Section 80C available under the New Tax Regime in 2026?

No. Section 80C deductions are not available under the New Tax Regime. If you opt for the New Tax Regime when filing your ITR, you lose all 80C benefits including PPF, ELSS, NSC, and EPF deductions. The New Tax Regime offers lower slab rates as a trade-off for eliminating most deductions. For salaried individuals with significant 80C investments, home loan interest, and HRA, the Old Tax Regime almost always results in lower total tax. Always calculate your liability under both regimes before choosing. For a detailed step-by-step comparison, read our guide on income tax filing at the official portal.

Can I invest in both PPF and ELSS for Section 80C in the same year?

Yes, you can invest in both PPF and ELSS in the same financial year and both count toward the same ₹1.5 lakh Section 80C ceiling. For example, if your EPF contribution for the year is ₹54,000, you can invest ₹50,000 in PPF and ₹46,000 in ELSS SIPs to reach the full ₹1.5 lakh limit. Splitting your remaining 80C investment between PPF (guaranteed, tax-free) and ELSS (market-linked, higher returns) is the recommended strategy for most working-age Indians who want both safety and growth in their tax-saving portfolio.