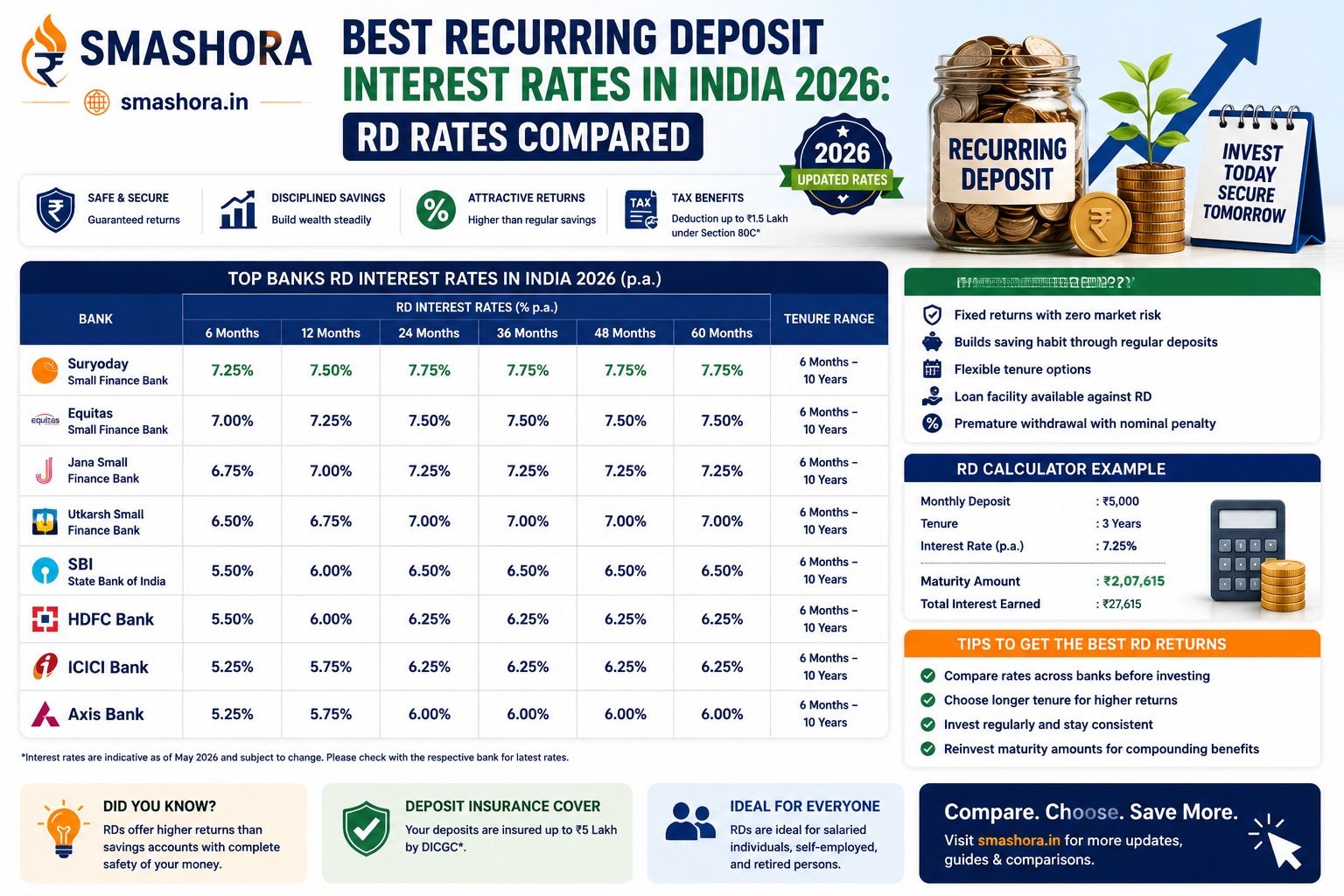

Contents

- 1 Government-Backed Savings Schemes for Women in India 2026

- 2 Women-Specific Loan Interest Rate Concessions in India 2026

- 3 Equity and Mutual Fund Investing — No Different by Gender, But Worth Starting Early

- 4 Insurance Considerations Specific to Women’s Financial Planning

- 5 Building a Practical Financial Plan — Best Investment Options for Women in India 2026 by Life Stage

- 6 Why Independent Financial Identity Matters

- 7 Conclusion — Build a Layered, Independent Financial Foundation

- 8 Frequently Asked Questions

- 8.1 What is the best investment option for women in India in 2026?

- 8.2 Is the Mahila Samman Savings Certificate still available in India in 2026?

- 8.3 What loan interest rate concessions are available specifically for women in India?

- 8.4 Should a woman invest separately even if her spouse manages household finances?

- 8.5 Does term insurance cost less for women in India?

- 8.6 How can a career break affect a woman’s long-term investment growth in India?

Identifying the best investment options for women in India 2026 is about more than just finding a high-interest scheme — it is about building genuine financial independence through a combination of dedicated savings instruments, meaningful loan rate concessions, and the right insurance protection, all designed around the specific financial journey many Indian women navigate. From career breaks for caregiving to outliving spouses on average, women’s financial planning benefits from a deliberate, layered approach rather than simply mirroring a generic investment checklist.

The encouraging reality in 2026 is that Indian banks, NBFCs, and government schemes increasingly recognise this and offer concrete, practical advantages specifically for women — from a guaranteed 0.05% lower home loan interest rate that compounds into meaningful savings over a 20-year tenure, to dedicated government savings instruments and insurance products with women-specific underwriting benefits. Knowing exactly which of these to use, and in what combination, is the foundation of smart financial planning for women in India 2026.

This complete guide on the best investment options for women in India 2026 covers government-backed savings schemes, women-specific loan concessions across home, business, and education loans, insurance considerations unique to women’s financial planning, and a practical framework for building wealth and security at every life stage.

Government-Backed Savings Schemes for Women in India 2026

Sukanya Samriddhi Yojana — Best for Daughters Below Age 10

For mothers and guardians of girl children below age 10, Sukanya Samriddhi Yojana remains the single best investment option among all government-backed schemes, currently offering 8.2% interest per annum, compounded annually, with complete EEE tax treatment — meaning the investment, the annual interest, and the maturity amount are all entirely tax-free. With a maximum annual investment of ₹1.5 lakh and a 21-year maturity period, SSY consistently outperforms every comparable government scheme in pure return terms while carrying the full sovereign guarantee of the Government of India.

For a complete breakdown of SSY including the maturity calculator, eligibility rules, and step-by-step account opening process, read our dedicated guide on Sukanya Samriddhi Yojana 2026.

An Important Note on the Mahila Samman Savings Certificate

Many women researching the best investment options for women in India 2026 still come across references to the Mahila Samman Savings Certificate (MSSC), a dedicated women-only scheme launched in the 2023-24 Union Budget that offered a fixed 7.5% interest rate, compounded quarterly, on deposits up to ₹2 lakh over a 2-year tenure. It is important to know that the scheme stopped accepting fresh deposits from April 1, 2025, and there has been no extension or relaunch announced in the 2026-27 Budget. If you already opened an MSSC account before the cutoff, it continues to earn the agreed 7.5% rate until its individual maturity date, but no new accounts can be opened under this scheme in 2026. For women looking for a comparable government-guaranteed instrument today, PPF, NSC, and bank fixed deposits remain the closest equivalent options currently open for fresh investment.

PPF and Other General Government Schemes — Equally Accessible to Women

Beyond SSY, women have full access to the same range of government savings schemes available to any Indian citizen — PPF at 7.1% with EEE tax treatment, NSC at 7.7% with Section 80C benefit, and the Senior Citizen Savings Scheme at 8.2% for women above 60. These instruments form a strong, risk-free foundation for any woman’s long-term savings, independent of marital or family financial structures. For a complete comparison of every government savings scheme with current rates, read our comprehensive guide on the best government savings schemes in India 2026.

Women-Specific Loan Interest Rate Concessions in India 2026

One of the most underutilised aspects of the best investment options for women in India 2026 is not a savings instrument at all — it is the meaningful interest rate concessions women receive across multiple loan categories, which directly reduce the cost of major life purchases and free up more capital for actual investment.

| Loan Type | Typical Women’s Concession | Impact on a Large Loan |

|---|---|---|

| Home Loan | 0.05% lower rate at most major banks | Meaningful cumulative saving over a 20-year tenure on a large loan amount |

| Business Loan (Bank of Baroda MSME Digital Loan) | 0.10% rate discount for women entrepreneurs | Reduces overall cost of business expansion capital |

| Education Loan (SBI and select banks) | 0.50% concession for female students | Significant cumulative saving on large education loans for studies abroad |

| Car Loan (SBI) | Concessional processing in select schemes | Lower upfront cost of vehicle financing |

Beyond the direct rate benefit, many states also offer reduced stamp duty rates for property registered in a woman’s name, which can mean a meaningful saving on a property purchase — always check your specific state’s current stamp duty schedule, since these vary and are revised periodically. For the complete current home loan landscape including all major lenders and their standard plus women-specific rates, read our detailed guide on the best home loan interest rates in India 2026.

Equity and Mutual Fund Investing — No Different by Gender, But Worth Starting Early

Equity mutual funds and index funds work identically for women as for any other investor — the same SIP discipline, the same long-term compounding principles, and the same fund selection criteria apply. The genuinely important consideration specific to many women’s financial journeys is the impact of career breaks, whether for childcare, caregiving for ageing parents, or other life transitions, on long-term retirement corpus building. Starting equity SIPs as early as possible, even at a modest amount, and treating any career-break period as a trigger to review and potentially increase contributions once income resumes, helps offset the compounding lost during any pause in active investing.

Insurance Considerations Specific to Women’s Financial Planning

Term Insurance — Often Underpurchased by Women

Many households default to purchasing term insurance only for the primary male earner, overlooking that a woman’s unpaid caregiving contribution, or her own income if employed, represents genuine economic value that would need to be replaced in her absence. Term insurance premiums for women are also typically lower than for men of the same age, given statistically longer average life expectancy, making adequate cover even more cost-effective. For a complete guide on choosing the right term insurance cover and understanding current premium benchmarks, read our article on the best term insurance plans in India 2026.

Health Insurance — Independent Cover Beyond Family Floater

While family floater health insurance policies are common and useful, many financial planners recommend women, particularly those who are homemakers or have variable income, maintain awareness of their specific coverage within any family floater, since a floater’s sum insured is shared across all members. For women planning major life events like childbirth, checking maternity coverage terms, waiting periods, and sum insured adequacy well in advance of need is an important and often overlooked part of comprehensive financial planning.

Building a Practical Financial Plan — Best Investment Options for Women in India 2026 by Life Stage

| Life Stage | Priority Investment Focus |

|---|---|

| Early Career (20s) | Start equity SIPs early, build PPF foundation, secure term and health insurance while premiums are lowest |

| Marriage and Family Building (late 20s to 30s) | Open SSY if you have a daughter, maintain independent investments alongside joint household finances, review insurance coverage adequacy |

| Career Break or Reduced Income Period | Continue minimum PPF and SIP contributions where possible to preserve compounding continuity, prioritise maintaining health insurance coverage |

| Mid-Career Re-Entry (30s to 40s) | Step up SIP contributions to offset any gap period, maximise 80C and 80CCD(1B) tax-saving investments, consider women-specific loan concessions for property purchase |

| Pre-Retirement and Retirement (50s plus) | Shift toward SCSS and senior citizen FDs for guaranteed income, ensure adequate health insurance given rising medical costs at this stage |

Why Independent Financial Identity Matters

Beyond the specific instruments and concessions covered above, one of the most valuable practices among the best investment options for women in India 2026 is maintaining at least some investments, bank accounts, and insurance policies independently, rather than exclusively through joint or spouse-managed arrangements. This independent financial footprint builds an individual CIBIL credit history, ensures direct access to funds in any emergency without requiring another person’s involvement, and provides genuine financial resilience regardless of changes in marital or family circumstances. Building and maintaining a strong personal credit score is a meaningful part of this independence, since it determines access to the favourable loan rates and concessions discussed earlier — our guide on how to improve your CIBIL score covers the specific steps for building this credit history from scratch or strengthening an existing one.

For the latest official information on government savings schemes available to women and girls, including current rates and eligibility notifications, refer to the National Savings Institute of India website.

Conclusion — Build a Layered, Independent Financial Foundation

The best investment options for women in India 2026 are not a single product but a deliberate combination — Sukanya Samriddhi Yojana for daughters, PPF and NSC for guaranteed long-term savings, equity SIPs started early and maintained through any career interruptions, term and health insurance recognising the real economic value of a woman’s contribution to the household, and active use of the loan rate concessions available across home, business, and education financing. Together, these build not just a larger corpus over time, but genuine financial independence and resilience.

The single most actionable step from this guide: if you have a daughter below age 10, open her SSY account today if you have not already, and if you are a woman applying for any major loan in 2026, always explicitly ask the lender about applicable women’s rate concessions, since these are not always volunteered automatically at the point of application.

At Smashora, our mission is to help every Indian make every rupee count, including the women building independent financial futures for themselves and their families. If this guide on the best investment options for women in India 2026 helped you plan more confidently, leave a comment below or share it with a woman in your life who is starting or strengthening her financial journey.

Frequently Asked Questions

What is the best investment option for women in India in 2026?

For mothers of daughters below age 10, Sukanya Samriddhi Yojana at 8.2% with complete EEE tax treatment is the single best dedicated government scheme available. For broader long-term savings, PPF at 7.1% tax-free remains an excellent risk-free foundation accessible to any woman regardless of family status. For long-term wealth building, equity mutual fund SIPs started early offer the highest growth potential. The right combination depends on your specific life stage, goals, and whether you have a daughter eligible for SSY.

Is the Mahila Samman Savings Certificate still available in India in 2026?

No. The Mahila Samman Savings Certificate stopped accepting new deposits from April 1, 2025, and there has been no extension or relaunch announced in the 2026-27 Union Budget. If you opened an account before this cutoff date, it continues to earn the originally agreed 7.5% interest rate until its individual two-year maturity date, but no fresh accounts can be opened under this scheme currently. Women looking for a comparable government-guaranteed savings instrument today should consider PPF, NSC, or bank and small finance bank fixed deposits, all of which remain open for fresh investment.

What loan interest rate concessions are available specifically for women in India?

Most major banks offer a 0.05% lower home loan interest rate for women borrowers, which compounds into a meaningful saving over a typical 20-year tenure. Select banks, including Bank of Baroda, offer a 0.10% rate discount for women entrepreneurs under specific MSME digital loan schemes. Education loans for female students at SBI and several other banks carry a 0.50% interest rate concession. Many states also offer reduced stamp duty for property registered in a woman’s name, providing an additional saving on real estate purchases. Always explicitly ask your lender about applicable women’s concessions, since these benefits are not always automatically highlighted during the application process.

Should a woman invest separately even if her spouse manages household finances?

Yes, most financial planners strongly recommend that women maintain at least some independent investments, bank accounts, and insurance policies, separate from joint or spouse-managed arrangements. This builds an individual CIBIL credit history necessary to access favourable loan rates and concessions independently, ensures direct access to funds during any emergency without requiring another person’s involvement, and provides genuine financial resilience regardless of how marital or family circumstances may change over time.

Does term insurance cost less for women in India?

Yes, generally. Term insurance premiums for women are typically lower than for men of the same age, primarily reflecting statistically longer average life expectancy used in insurer underwriting and pricing models. This makes adequate term insurance coverage even more cost-effective for women, yet many households still default to purchasing cover only for a primary male earner, overlooking the genuine economic value, whether through income or unpaid caregiving contribution, that a woman’s absence would require replacing in any household’s financial planning.

How can a career break affect a woman’s long-term investment growth in India?

A career break for childcare, caregiving, or other life transitions can meaningfully reduce the total compounding period for retirement-focused investments like equity SIPs and PPF, since contributions typically pause or reduce significantly during this time. The most effective mitigation is continuing at least minimal contributions during the break period wherever financially possible, to preserve continuity in the investment, and then deliberately stepping up SIP contributions once income resumes to help offset the growth gap created during the pause. Starting investments as early as possible in one’s career, before any anticipated break, also provides a larger compounding base that better absorbs the impact of a later interruption.