Contents

- 1 Current Car Loan Interest Rates in India — June 2026

- 2 Best Car Loan Interest Rates in India 2026 — Lender by Lender Review

- 3 Car Loan EMI Calculator — Reference Table

- 4 How Your CIBIL Score Affects Your Car Loan Rate

- 5 New Car Loan vs Used Car Loan in India 2026

- 6 EV Car Loan — Special Rates for Electric Vehicles in 2026

- 7 Zero Percent EMI Car Deals — What You Need to Know

- 8 Prepayment Rules for Car Loans in India 2026

- 9 How to Get the Best Car Loan Rate in India 2026 — Step by Step

- 10 Conclusion — Compare the Best Car Loan Interest Rates in India 2026 Before You Sign

- 11 Frequently Asked Questions

- 11.1 Which bank offers the best car loan interest rate in India in 2026?

- 11.2 What CIBIL score is needed for the best car loan rate in India in 2026?

- 11.3 What is the EMI on a ₹8 lakh car loan over 5 years in India in 2026?

- 11.4 Can I get a car loan with a 0% interest rate in India?

- 11.5 Is it better to take a longer tenure (7 years) or shorter tenure (5 years) for a car loan?

- 11.6 Can I prepay my car loan early and how much does it cost?

Knowing the best car loan interest rates in India 2026 before you visit a showroom or speak to a bank could save you ₹20,000 to ₹80,000 in total interest on a typical car purchase. Car loan rates in India start as low as 7.35% per year at competitive public sector banks in June 2026 — but the same borrower might end up paying 10% to 11% simply by going with the first bank the car dealer suggests without comparing alternatives.

The car dealer’s preferred finance partner is almost never the best deal for you. Dealers earn a referral commission from the banks and NBFCs they send customers to — which means there is a direct financial incentive for them to route you toward partners with higher rates, not the ones with the best rates for your profile. A colleague bought a Hyundai Creta last year at the dealer’s suggested bank at 9.5% interest — completely unaware that his own salary account bank had a pre-approved car loan offer at 8.15% waiting in his mobile app. On his ₹7 lakh loan over 5 years, that difference meant paying approximately ₹26,000 more in total interest. Thirty minutes of comparison saved nothing because he did not look.

This complete guide on the best car loan interest rates in India 2026 covers current rates from all major lenders, a ready EMI reference table, the key factors that determine your rate, new vs used car loan differences, and exactly what to do to get the lowest possible rate on your car purchase this year.

Current Car Loan Interest Rates in India — June 2026

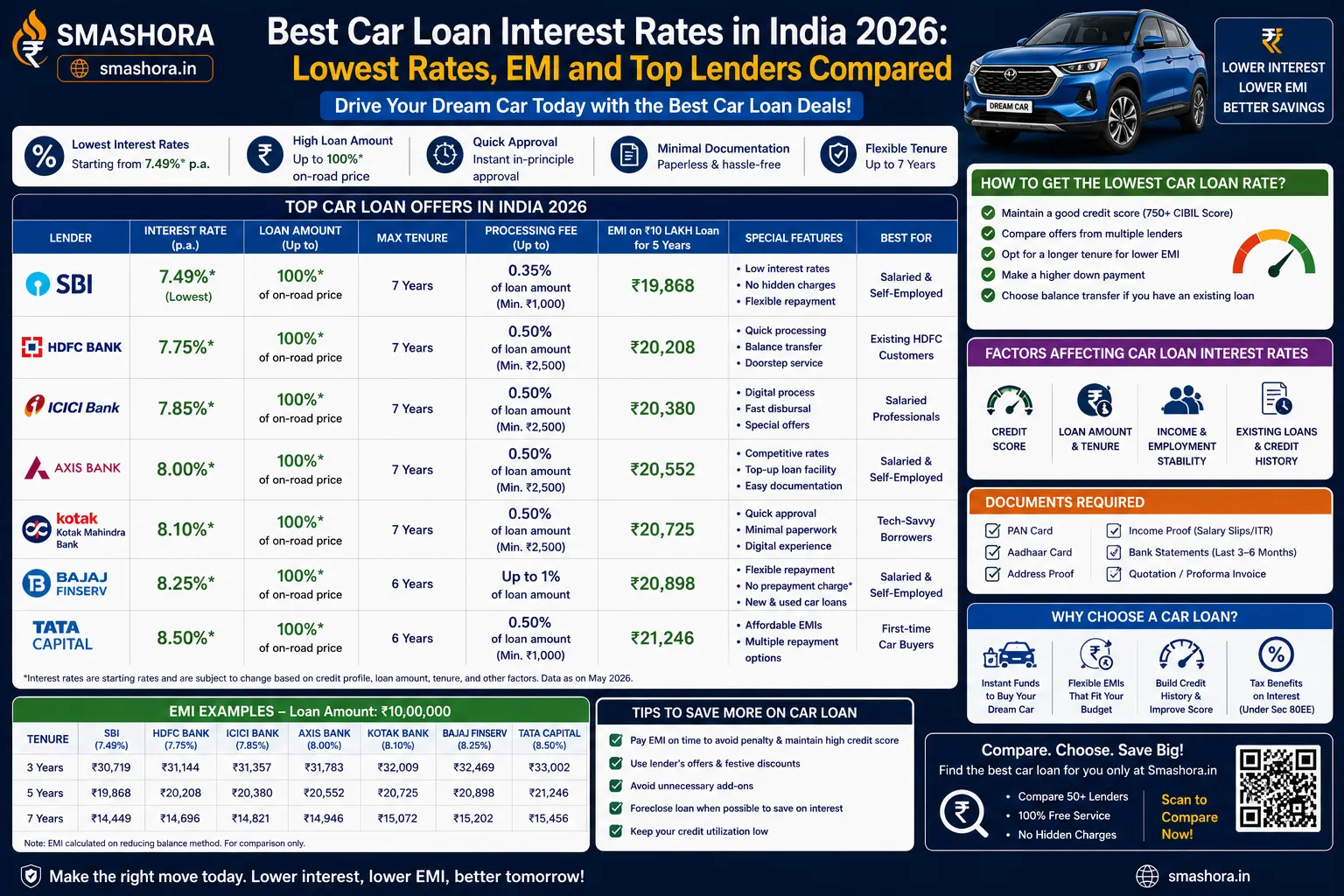

Here are the best car loan interest rates in India 2026 from all major lenders as of June 2026:

| Lender | Interest Rate (New Car) | Processing Fee | Max LTV | Max Tenure |

|---|---|---|---|---|

| UCO Bank | 7.40% to 9.25% per year | 0.50% | 100% on-road price | 7 years |

| Union Bank of India | 7.40% to 9.50% per year | 0.50% | 100% on-road price | 7 years |

| Canara Bank | 7.50% to 9.65% per year | 0.25% | 100% on-road price | 7 years |

| Punjab National Bank | 7.60% to 10.70% per year | 0.35% | 100% on-road price | 7 years |

| Bank of Maharashtra | 7.60% to 9.85% per year | 0.25% | 100% on-road price | 7 years |

| State Bank of India | 8.90% to 9.85% per year | Nil to 0.50% | 100% on-road price | 7 years |

| HDFC Bank | 8.15% to 17.35% per year | Up to ₹8,850 | 100% on-road price | 7 years |

| ICICI Bank | 8.35% to 13.00% per year | Up to ₹10,000 | 100% on-road price | 7 years |

| Axis Bank | 8.75% to 14.50% per year | Up to ₹5,500 | 100% on-road price | 7 years |

| Kotak Mahindra Bank | 7.99% to 16.00% per year | Up to ₹5,000 | 100% on-road price | 5 years |

The wide rate range at every bank reflects how much your CIBIL score and borrower profile affect the rate you personally receive. The best car loan interest rates in India 2026 at the starting end (7.40% to 7.60%) are reserved for borrowers with CIBIL scores above 750 and clean repayment histories. For official lending guidelines and monetary policy context, refer to the Reserve Bank of India website.

Best Car Loan Interest Rates in India 2026 — Lender by Lender Review

UCO Bank and Union Bank — Best for Absolute Lowest Rate

For borrowers whose only priority is the lowest possible car loan interest rate in India 2026, UCO Bank and Union Bank of India start at 7.40% per year — the most competitive starting rates in the market. Both are public sector banks with government ownership and a lower cost of funds that enables them to offer rates private banks cannot match.

- Rate: 7.40% to 9.25% per year (UCO Bank)

- Processing fee: 0.50% (reasonable)

- Tenure: Up to 7 years

- Prepayment: No charges on floating rate loans

- Special feature: UCO Bank offers 100% on-road price financing for eligible borrowers with no down payment requirement for CIBIL 750 plus profiles

Best for: Borrowers with CIBIL scores above 750 who want the lowest possible rate and are comfortable with the slightly slower processing that public sector banks typically have compared to private banks.

HDFC Bank — Best for Speed and Pre-Approved Offers

HDFC Bank is one of India’s most popular car loan providers and regularly appears among the best car loan interest rates in India 2026 for existing customers with pre-approved offers. HDFC offers instant car loans with same-day disbursal for pre-approved customers — a feature that is particularly useful when closing a deal at a showroom where the sale might fall through if funding is delayed.

- Rate: Starting from 8.15% per year (June 2026)

- Processing fee: Fixed charges up to ₹8,850 depending on loan amount

- Tenure: Up to 7 years

- Key feature: 10-second pre-approved car loan for eligible HDFC account holders via NetBanking or iMobile

- Prepayment charges: 6% of outstanding principal within 12 months, reducing to 3% after 24 months — significant charges worth noting

Best for: Existing HDFC Bank salary account holders with pre-approved offers. Always check your HDFC NetBanking or iMobile app for a pre-approved car loan rate before negotiating with the dealer’s finance representative.

ICICI Bank — Best for Flexible Car Loan Structures

ICICI Bank offers competitive rates on car loans in 2026 with a fully digital application process and multiple loan structure options including step-up EMI plans where your EMI increases gradually as your income grows — a useful feature for borrowers early in their careers who expect income growth over the loan tenure.

- Rate: Starting from 8.35% per year (June 2026)

- Processing fee: Up to ₹10,000

- Tenure: Up to 7 years

- Key feature: Balloon payment structure and step-up EMI options for income-growth borrowers

- Pre-approved offers: Available instantly for existing ICICI Bank customers via iMobile Pay

Best for: Young professionals with expected salary growth who want structured EMI flexibility, or existing ICICI Bank customers with pre-approved offers.

SBI Car Loan — Best for Government Employees

SBI’s car loan rates in June 2026 start at 8.90% — higher than UCO Bank or PNB. However, SBI offers special concession rates for government employees, central and state government workers, and defence personnel that can bring the effective rate significantly lower. SBI also charges zero prepayment penalty on all car loans — making it the best choice if you plan to repay the loan early from a bonus or windfall.

- Rate: 8.90% to 9.85% per year (general)

- Special rate for government employees: 0.25% to 0.50% concession

- Processing fee: Nil to 0.50% (frequently waived during festive offers)

- Tenure: Up to 7 years

- Prepayment: Zero charges — best policy among major lenders

Best for: Government employees, defence personnel, and PSU workers who get special rate concessions, and anyone who plans to prepay the loan early to save on total interest.

Car Loan EMI Calculator — Reference Table

Understanding your monthly EMI before committing is essential when evaluating the best car loan interest rates in India 2026. Here is a quick reference table for the most common car loan amounts:

| Loan Amount | 7.50% — 5 Years | 8.50% — 5 Years | 9.50% — 5 Years | 7.50% — 7 Years |

|---|---|---|---|---|

| ₹3 lakh | ₹6,006 | ₹6,141 | ₹6,279 | ₹4,576 |

| ₹5 lakh | ₹10,010 | ₹10,235 | ₹10,465 | ₹7,627 |

| ₹7 lakh | ₹14,014 | ₹14,329 | ₹14,651 | ₹10,677 |

| ₹10 lakh | ₹20,020 | ₹20,470 | ₹20,930 | ₹15,253 |

| ₹15 lakh | ₹30,030 | ₹30,705 | ₹31,395 | ₹22,879 |

On a ₹7 lakh car loan over 5 years, the EMI difference between 7.50% and 9.50% is ₹637 per month — which adds up to ₹38,220 in extra total interest over the loan period. This is why comparing the best car loan interest rates in India 2026 before committing is worth every minute of the effort.

How Your CIBIL Score Affects Your Car Loan Rate

Just like home loans and personal loans, your CIBIL score is the single most important factor determining which rate you receive among the best car loan interest rates in India 2026:

| CIBIL Score | Likely Rate Range (PSU Banks) | Likely Rate Range (Private Banks) | Impact on ₹8L Loan Over 5 Years |

|---|---|---|---|

| 800 and above | 7.40% to 7.75% | 8.15% to 8.50% | Lowest total interest |

| 750 to 799 | 7.75% to 8.50% | 8.50% to 9.25% | ₹15,000 to ₹25,000 more than 800 plus profile |

| 700 to 749 | 8.50% to 9.50% | 9.25% to 11.00% | ₹35,000 to ₹55,000 more than 800 plus profile |

| 650 to 699 | Difficult approval | 11.00% to 14.00% | ₹60,000 to ₹90,000 more — or rejection |

| Below 650 | Very likely rejected | NBFC only at 14% plus | Not advisable to borrow at these rates |

If your CIBIL score is currently below 750, spending 3 to 6 months improving it before applying for a car loan is genuinely worth the wait — the interest savings over a 5-year loan tenure often exceed ₹30,000 to ₹50,000. Read our complete guide on how to improve your CIBIL score for step-by-step actions that work within 3 to 6 months.

New Car Loan vs Used Car Loan in India 2026

The best car loan interest rates in India 2026 differ significantly between new and used (pre-owned) vehicles:

| Feature | New Car Loan | Used Car Loan |

|---|---|---|

| Interest Rate (starting) | 7.40% per year | 9.50% to 11.00% per year |

| Maximum LTV | Up to 100% on-road price | Up to 80% to 85% of car value |

| Maximum Tenure | 7 years | 5 years typically |

| Car Age Restriction | Not applicable | Car should not be older than 5 years at most banks |

| Loan Amount | Up to full on-road price | Limited by assessed market value of car |

Used car loans attract significantly higher interest rates than new car loans — typically 2% to 3% higher — because used cars depreciate faster and represent higher collateral risk for the lender. If you are deciding between a used car with lower upfront cost versus a new car with higher upfront cost, always factor in the higher interest rate on the used car loan when calculating the total cost of ownership.

EV Car Loan — Special Rates for Electric Vehicles in 2026

With India’s electric vehicle adoption accelerating in 2026, most major banks now offer special concessional rates on EV car loans as part of green lending initiatives encouraged by the RBI:

- SBI Green Car Loan: 0.20% concession below the standard new car loan rate for all electric vehicles

- Bank of Baroda: Special EV loan rates starting from 7.25% — among the best car loan interest rates in India 2026 specifically for EVs

- HDFC Bank: EV-specific loan products with longer tenures and competitive rates

- Canara Bank: EV loan starting from 7.40% with additional 0.25% concession for women borrowers

- Union Bank: Green vehicle loan at 7.15% — lowest available EV car loan rate among major banks in June 2026

If you are considering an EV purchase, always ask the bank specifically for their EV car loan rate — it may be 0.20% to 0.50% lower than the standard new car loan rate and can result in meaningful interest savings over a 5 to 7 year tenure.

Zero Percent EMI Car Deals — What You Need to Know

Many car manufacturers and dealers advertise 0% EMI car financing schemes. Before getting excited about these offers, here is what is actually happening behind the scenes:

- The manufacturer or dealer subsidises the interest by paying a subvention amount to the bank upfront — the interest is not actually zero, it is being paid for you

- The car’s effective price is often higher under 0% EMI schemes — the manufacturer bakes the interest cost into the car’s selling price by reducing or eliminating discounts that would otherwise be available

- Compare the on-road price under the 0% EMI offer vs the on-road price with full payment or a regular bank loan plus any negotiated discount. If the car is ₹30,000 to ₹50,000 cheaper with a regular bank loan, the bank loan at 8.50% may be cheaper in total cost than the 0% EMI deal

- Processing fees and other charges are often higher on 0% EMI schemes than on regular bank loans

Always do the total cost calculation before accepting a 0% EMI offer. Ask the dealer what cash discount or additional accessories they can include if you arrange your own bank financing instead. The answer often reveals the true economics of the 0% scheme.

Prepayment Rules for Car Loans in India 2026

Prepayment rules vary significantly across lenders and understanding them is important when choosing the best car loan interest rates in India 2026:

| Lender | Prepayment / Foreclosure Charges |

|---|---|

| SBI | Zero — no prepayment charges on any car loan |

| UCO Bank and Canara Bank | Zero on floating rate loans |

| HDFC Bank | 6% within 12 months, 5% between 13 to 24 months, 3% after 24 months |

| ICICI Bank | 3% to 5% depending on timing |

| Axis Bank | 5% for first 12 months, 3% thereafter |

If you receive a year-end bonus, a salary hike, or any windfall and want to prepay your car loan early, HDFC’s 6% foreclosure charge in the first year is a significant cost — approximately ₹36,000 to ₹48,000 on a ₹6 to ₹8 lakh outstanding balance. SBI and UCO Bank’s zero prepayment policy makes them significantly more attractive if early repayment is a possibility.

How to Get the Best Car Loan Rate in India 2026 — Step by Step

- Check your CIBIL score first: Before stepping into any showroom, know your score. A 750 plus score gets you the best advertised rates. If below 700, delay the purchase by 3 to 4 months and improve first.

- Check your existing bank app for pre-approved offers: Before comparing externally, check your salary account bank’s mobile app — HDFC, ICICI, SBI YONO, and Kotak all display pre-approved car loan offers with actual personalised rates.

- Get quotes from at least 3 lenders: Include at least one public sector bank (UCO, PNB, or Canara) where the best car loan interest rates in India 2026 tend to be lowest, plus your salary bank, plus one NBFC for comparison.

- Compare total cost, not just rate: Add processing fees, documentation charges, insurance requirements, and prepayment charges to the interest cost comparison. A 7.50% loan with ₹10,000 in processing fees may cost more than an 8.00% loan with zero processing fee on a smaller loan amount.

- Negotiate the processing fee: Most banks will waive or significantly reduce the processing fee — especially during festive offers or for existing customers. Always ask before signing.

- Avoid the showroom finance desk as your first stop: The showroom finance representative earns a commission from the bank or NBFC they recommend. Use them for information, but compare independently before deciding.

Once your car purchase is sorted, also make sure your overall financial foundation is strong. Our guide on how to build an emergency fund in India will help you ensure that an unexpected expense does not force you to miss a car loan EMI — which directly damages your CIBIL score and increases the cost of future loans. For a comparison of how car loan rates fit into the broader Indian credit landscape, see our articles on the best home loan interest rates in India 2026 and the best personal loan in India 2026.

Conclusion — Compare the Best Car Loan Interest Rates in India 2026 Before You Sign

The best car loan interest rates in India 2026 start at 7.40% at UCO Bank and Union Bank for high-credit-score borrowers — well below the 8.90% to 9.85% that SBI charges and the 8.15% to 14%+ that HDFC Bank offers across its range. For EV buyers, Union Bank’s green vehicle loan at 7.15% is among the most competitive rates available anywhere in the Indian car finance market in 2026.

The most important actions to take before financing a car in 2026: check your CIBIL score, look for pre-approved offers in your banking app, get quotes from at least 3 lenders including one public sector bank, understand the prepayment charges, and never accept the showroom’s first finance offer without comparing. The thirty minutes spent comparing rates could save you ₹25,000 to ₹80,000 in total interest over your loan tenure.

At Smashora, our mission is to help every Indian make every rupee count. If this guide on the best car loan interest rates in India 2026 helped you plan your vehicle purchase more intelligently, leave a comment below or share it with a friend or family member who is currently planning a car purchase.

Frequently Asked Questions

Which bank offers the best car loan interest rate in India in 2026?

Among all lenders, UCO Bank and Union Bank of India offer the best car loan interest rates in India 2026 with starting rates of 7.40% per year for eligible borrowers with CIBIL scores above 750. Among private sector banks, HDFC Bank starts from 8.15% and ICICI Bank from 8.35% in June 2026. For electric vehicles specifically, Union Bank’s green vehicle loan starts at 7.15% — the lowest EV car loan rate from a major bank. Always get personalised quotes from at least 3 lenders before committing, as the advertised starting rate is only available to the highest credit profile borrowers.

What CIBIL score is needed for the best car loan rate in India in 2026?

A CIBIL score of 750 and above qualifies you for the best advertised car loan rates in India 2026 at most major banks. A score of 800 and above may get you an additional rate concession of 0.10% to 0.25% at some lenders. Below 700, most PSU banks will either decline or offer rates of 9.50% to 10.70%, and private banks may charge 11% to 14% on the same loan. If your score is below 700, spending 3 to 6 months improving it before applying can save ₹30,000 to ₹60,000 in total interest on a typical car loan. Our guide on how to improve your CIBIL score covers the exact steps.

What is the EMI on a ₹8 lakh car loan over 5 years in India in 2026?

At an interest rate of 7.50% per year, the EMI on an ₹8 lakh car loan over 5 years is approximately ₹16,016 per month and the total interest paid is approximately ₹1.61 lakh. At 8.50%, the EMI rises to approximately ₹16,376 and total interest becomes approximately ₹1.83 lakh. At 9.50%, the EMI is approximately ₹16,744 and total interest approximately ₹2.05 lakh. The difference between the lowest and highest rate on this loan is approximately ₹44,000 in total extra interest over 5 years — well worth spending time on comparison shopping before committing.

Can I get a car loan with a 0% interest rate in India?

True zero-interest car loans do not exist. When a manufacturer or dealer advertises 0% EMI, the interest is being subsidised by the car manufacturer who pays the bank a subvention amount upfront. This cost is typically recovered by reducing or eliminating the cash discounts you would otherwise receive on the car’s selling price. Before accepting a 0% EMI deal, always ask the dealer what cash discount or additional accessories you would receive if you arranged your own bank financing. If the car is ₹30,000 to ₹50,000 cheaper without the 0% EMI scheme, a regular bank loan at 7.50% to 8.50% will cost you less in total.

Is it better to take a longer tenure (7 years) or shorter tenure (5 years) for a car loan?

A shorter tenure (5 years) is almost always better financially — you pay significantly less total interest even though the monthly EMI is higher. On a ₹7 lakh loan at 8.50%, the total interest over 5 years is approximately ₹1.60 lakh while the total interest over 7 years is approximately ₹2.25 lakh — a difference of ₹65,000. However, if the 5-year EMI is too high relative to your monthly income and other EMI obligations, a 7-year tenure keeps the EMI manageable and prevents missed payments — which would hurt your CIBIL score more than the extra interest costs.

Can I prepay my car loan early and how much does it cost?

Yes, you can prepay your car loan early at most banks. Prepayment charges vary significantly: SBI, UCO Bank, and Canara Bank charge zero prepayment penalty on floating rate car loans — making early repayment completely free. HDFC Bank charges 6% of the outstanding principal if you close within 12 months, reducing to 3% after 24 months. ICICI Bank charges 3% to 5% depending on timing. If you plan to use a year-end bonus or windfall to close your car loan early, choose SBI or UCO Bank specifically for their zero prepayment policy — you will save both the prepayment charge and all remaining future interest simultaneously.